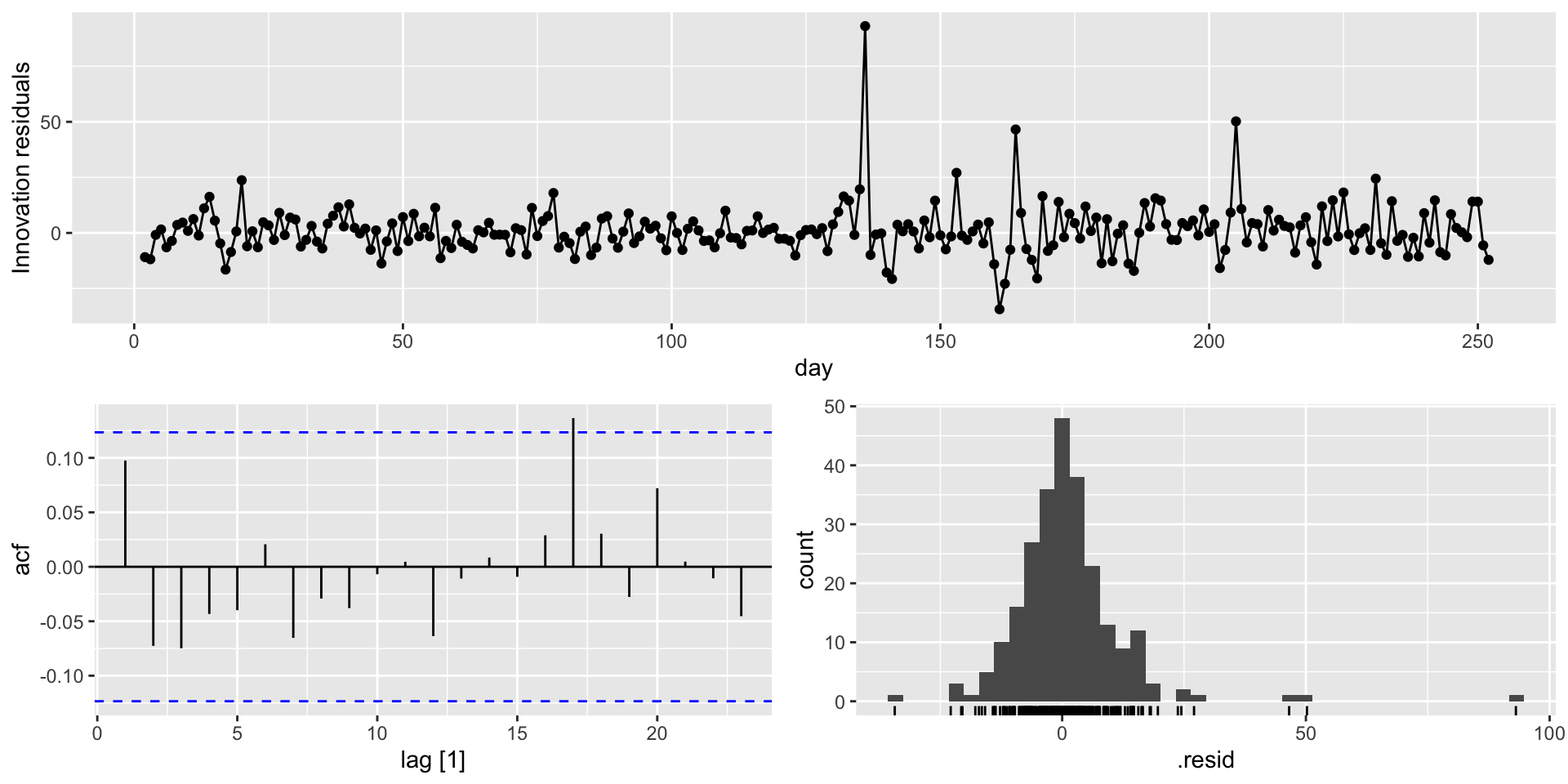

Forecasting diagnostics

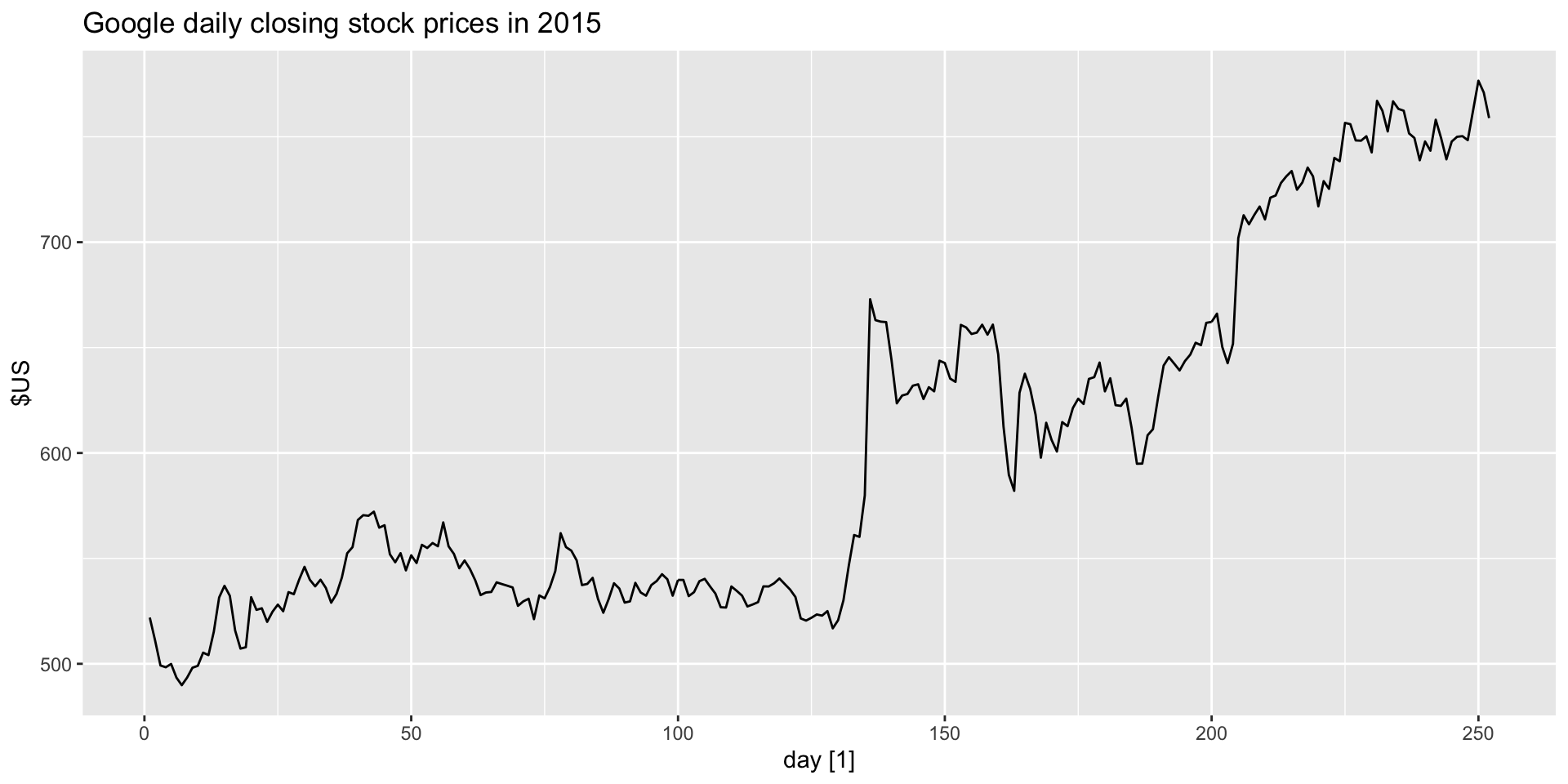

Example: Google closing stock prices

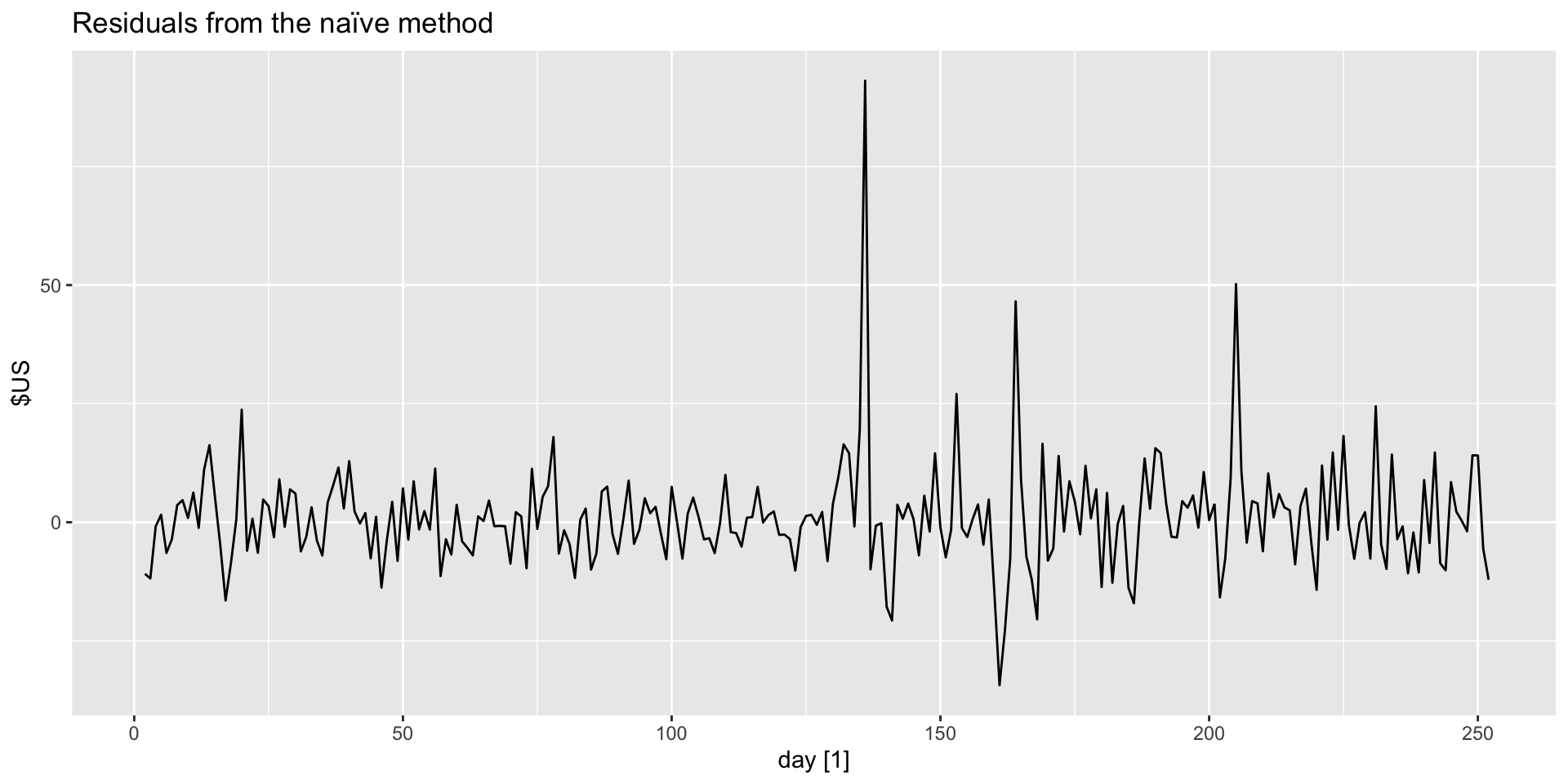

- Innovation residual for a naive forecast?

- \(e_{t} = y_{t} - \hat{y}_{t} = y_{t} - y_{t-1}\).

- And make an autoplot:

Example: Google closing stock prices residual autoplot

- Autoplot the innovation residuals:

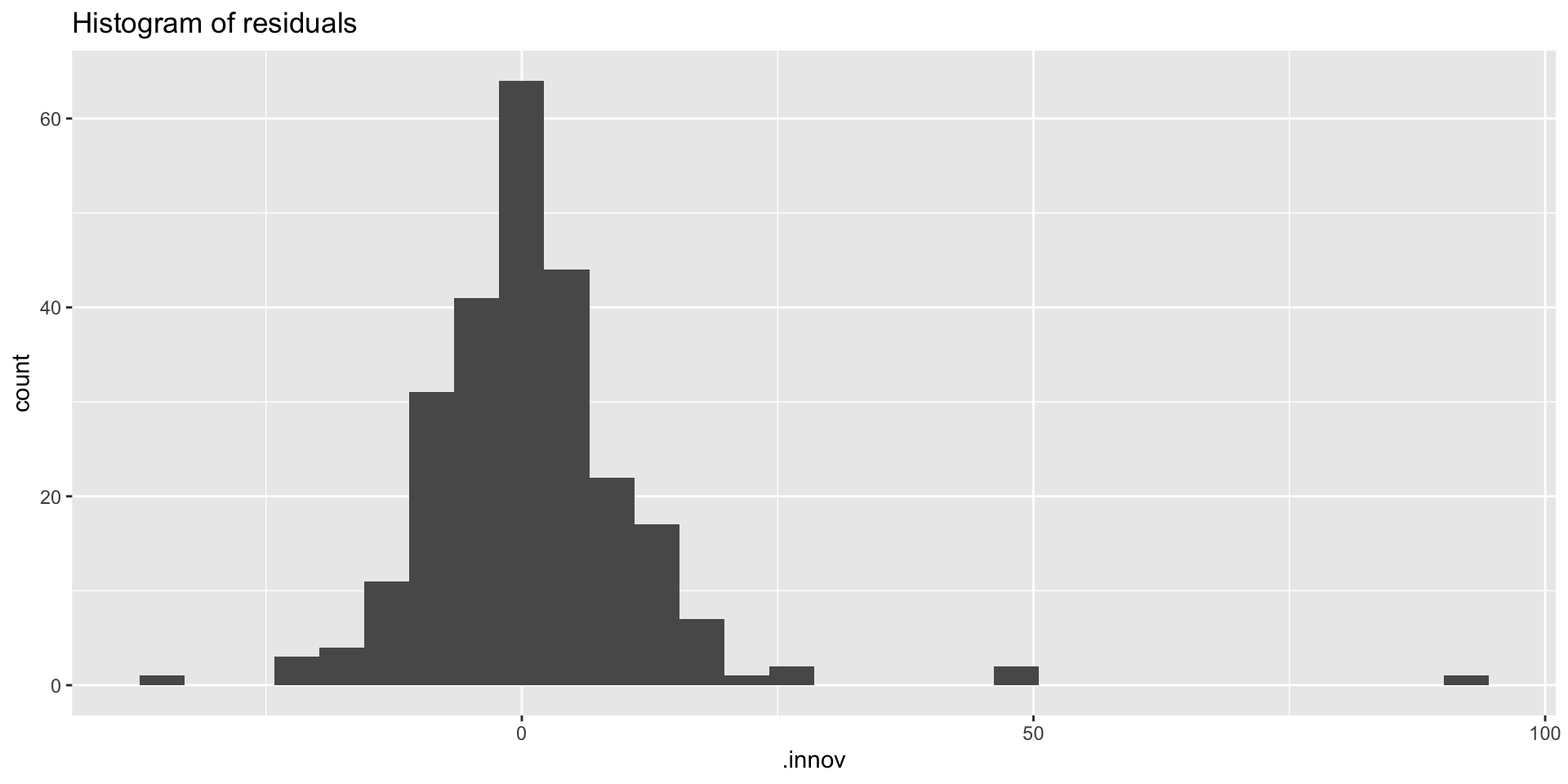

Example: Google closing stock prices residual histogram

-Produce a histogram of the innovation residuals:

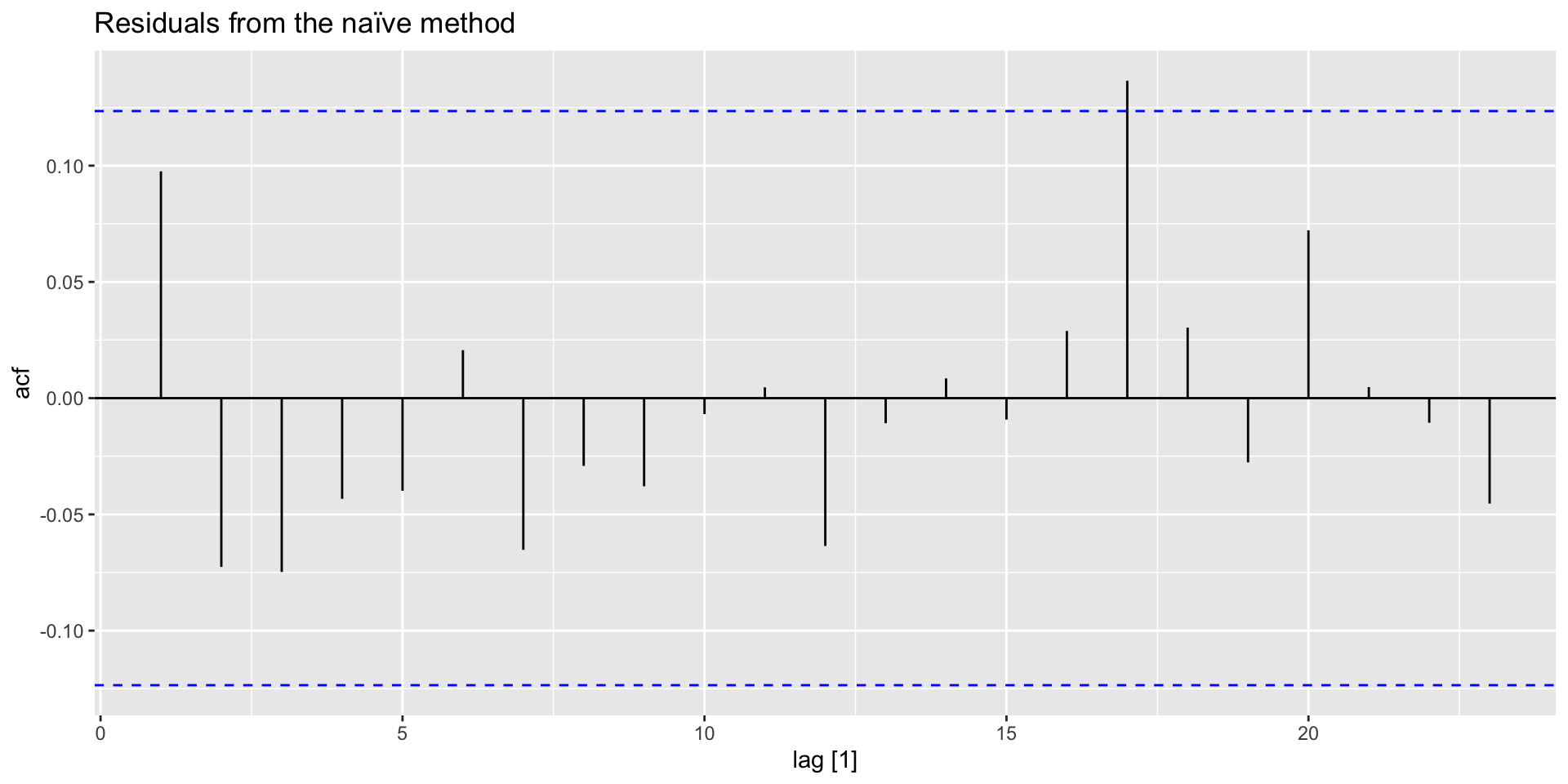

Example: Google closing stock prices ACF plot

- Produce an ACF plot:

Example: Google closing stock prices tsresiduals()

- You can use

tsresiduals()to produce all of these: