Distributional forecasts and prediction intervals

BUS 323 Forecasting and Risk Analysis

Forecast distributions

- Forecasts have associated probability distribution

- Typically Normal

- Mean: point forecast

Prediction intervals

- 95% interval for a Normally distributed \(h\)-step forecast:

\[ \widehat{y}_{T+h|T} \pm 1.96 \widehat{\sigma}_{h} \]

where \(\widehat{\sigma}_{h}\) is the standard error of the \(h\)-step forecast.

Forecast standard error

- Where do we get \(\widehat{\sigma}_{h}\) from?

- Need residual standard error first

- Next, we can find the distribution standard error.

Forecast standard error: demonstration

- e.g. for a mean forecast:

\[ \widehat{y}_{T+h|T} = \bar{y} \]

The residual is \(e_{T+h} = y_{T+h} - \bar{y}\).

- \(y_{T+h} \sim N(0,\sigma)\).

- \(\bar{y} \sim N(0,\sqrt{\frac{\sigma^{2}}{T}})\).

- Thus \(e_{T+H} \sim N(0, \sqrt{\sigma^{2} + \frac{\sigma^{2}}{T}})\).

Forecast standard error: demonstration

- Constant forecast with this method

\(\rightarrow\) Constant forecast standard error of \(\sigma \sqrt{1 + \frac{1}{t}}\).

Forecast standard errors: other methods

- Mean: \(\widehat{\sigma}_{h} = \widehat{\sigma} \sqrt{1 + \frac{1}{T}}\)

- Naive: \(\widehat{\sigma}_{h} = \widehat{\sigma} \sqrt{h}\)

- Seasonal naive: \(\widehat{\sigma}_{h} = \widehat{\sigma} \sqrt{k+1}\)

- where \(k\) represents \(\frac{h-1}{m}\) and \(m\) represents the seasonal period

- Drift: \(\widehat{\sigma}_{h} = \widehat{\sigma} \sqrt{h(1 + \frac{h}{T-1})}\)

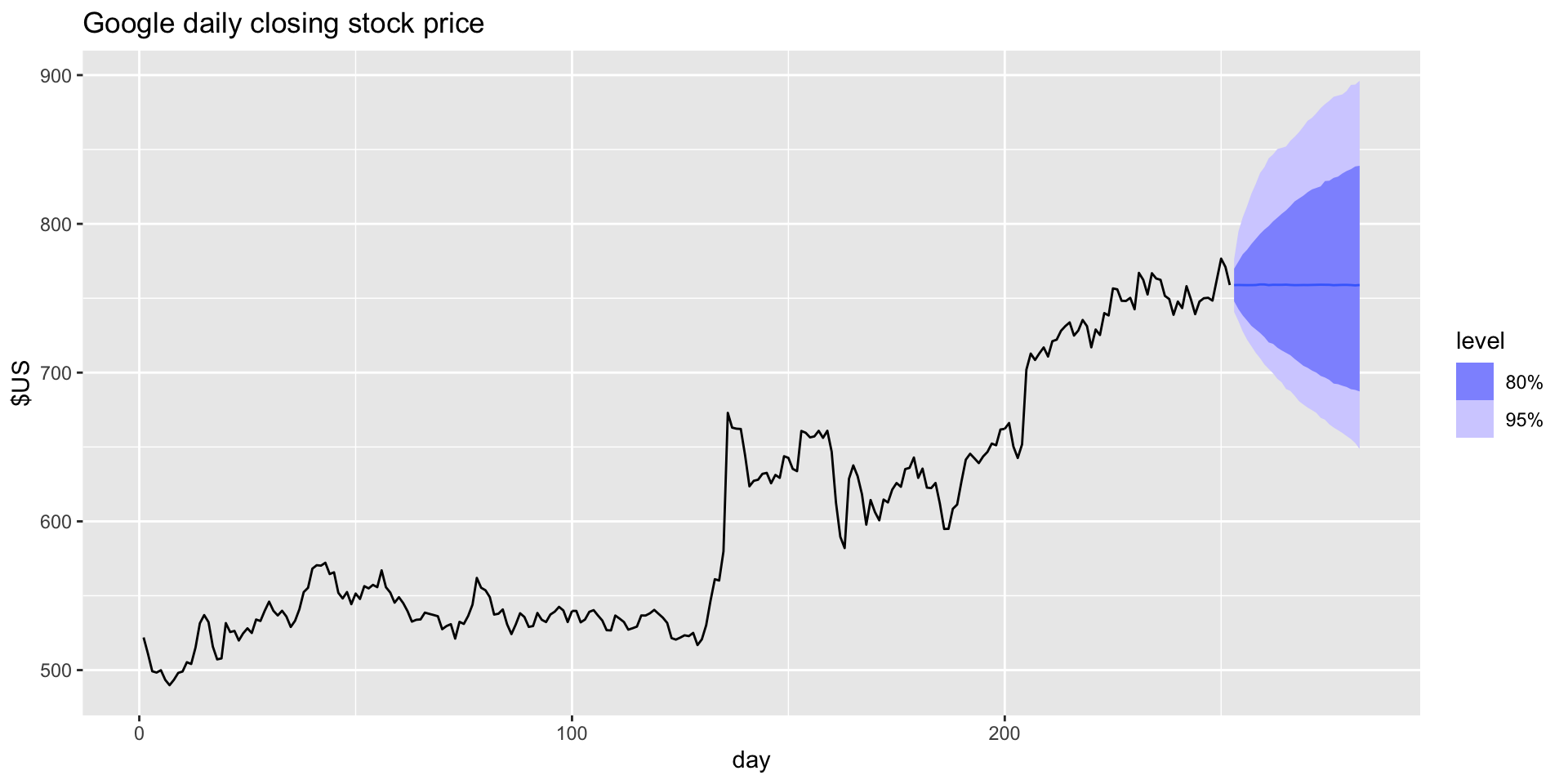

Computing prediction intervals with R

- Using the pakcage

fable(withinfpp3) and functionhilo():

| Symbol | .model | day | Close | .mean | 80% | 95% |

|---|---|---|---|---|---|---|

| GOOG | NAIVE(Close) | 253 | N(759, 125) | 758.88 | [744.5400, 773.2200]80 | [736.9488, 780.8112]95 |

| GOOG | NAIVE(Close) | 254 | N(759, 250) | 758.88 | [738.6001, 779.1599]80 | [727.8646, 789.8954]95 |

| GOOG | NAIVE(Close) | 255 | N(759, 376) | 758.88 | [734.0423, 783.7177]80 | [720.8941, 796.8659]95 |

| GOOG | NAIVE(Close) | 256 | N(759, 501) | 758.88 | [730.1999, 787.5601]80 | [715.0176, 802.7424]95 |

| GOOG | NAIVE(Close) | 257 | N(759, 626) | 758.88 | [726.8147, 790.9453]80 | [709.8404, 807.9196]95 |

| GOOG | NAIVE(Close) | 258 | N(759, 751) | 758.88 | [723.7543, 794.0058]80 | [705.1598, 812.6002]95 |

| GOOG | NAIVE(Close) | 259 | N(759, 876) | 758.88 | [720.9399, 796.8202]80 | [700.8556, 816.9045]95 |

| GOOG | NAIVE(Close) | 260 | N(759, 1002) | 758.88 | [718.3203, 799.4397]80 | [696.8493, 820.9108]95 |

| GOOG | NAIVE(Close) | 261 | N(759, 1127) | 758.88 | [715.8599, 801.9001]80 | [693.0865, 824.6735]95 |

| GOOG | NAIVE(Close) | 262 | N(759, 1252) | 758.88 | [713.5329, 804.2272]80 | [689.5275, 828.2325]95 |

Computing prediction intervals with R

- Use the

leveloption for different levels of confidence.

Prediction intervals from bootstrapped residuals

- Normal distribution not always a reasonable assumption.

- Bootstrapping: non-parametric method of generating prediction intervals

- Suppose a naive forecast: \(y_{t} = y_{t-1} + e_{t}\).

- Bootstrapping assumes future residuals will be similar to past residuals.

- For \(t>T\), use \(e_{t|t \leq T}\) to model \(e_{t}\).

prediction intervals from bootstrapped residuals

- Thus we can simulate: \(y_{T+1}^{*} = y_{T} + e_{T+1}^{*}\).

- Where \(e_{T+1}^{*}\) is a randomly sampled observed residual. \(y_{T+1}^{*}\) is the forecast under that particular residual value.

- Repeat: \(y_{T+2}^{*} = y_{T+1}^{*} + e_{T+2}^{*}\).

- We can obtain many possible futures by repeating this process.

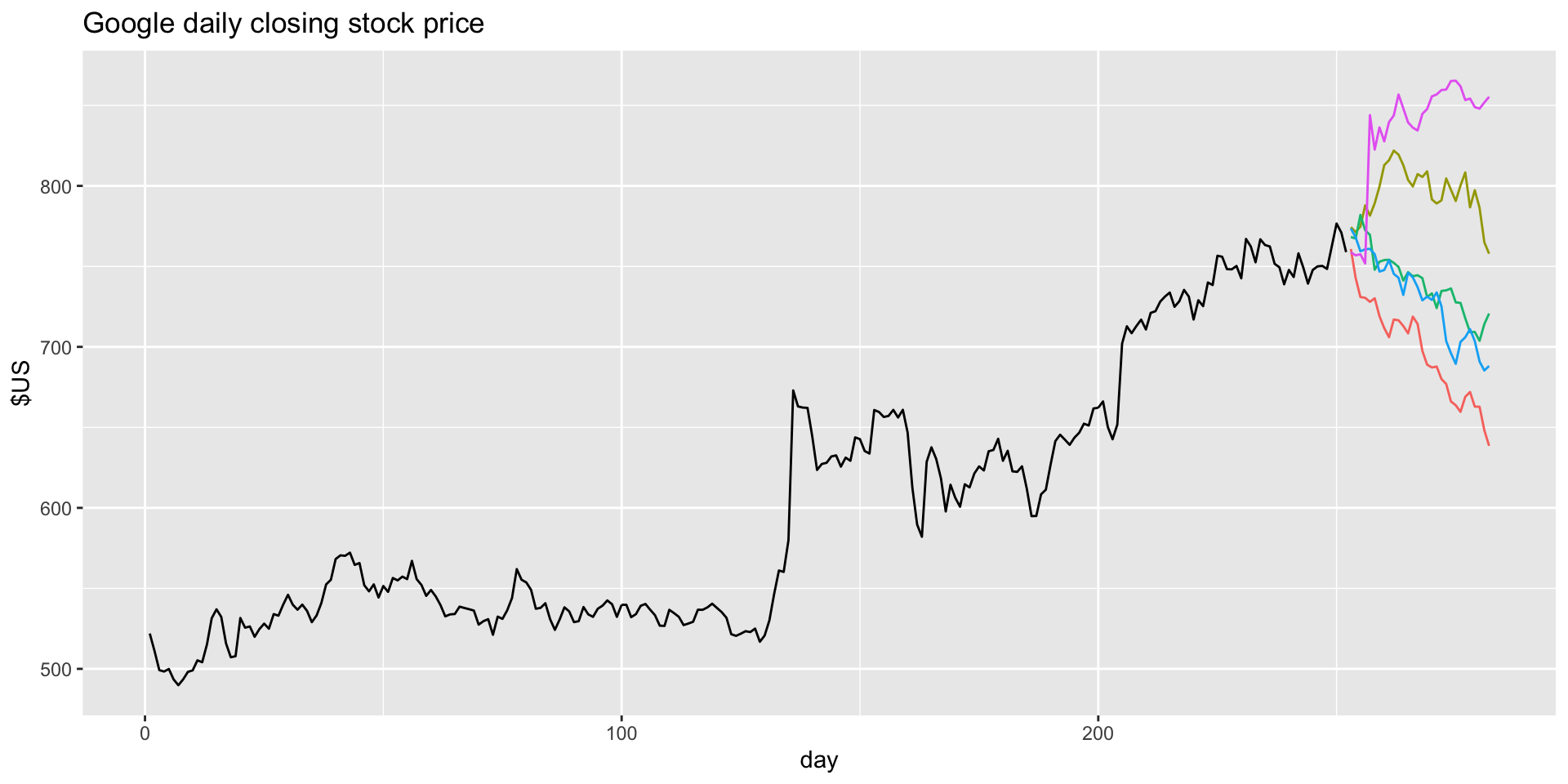

Bootstrap prediction intervals demonstration

- To see how this works, use the

generate()function:

fit <- google_2015 |>

model(NAIVE(Close))

sim <- fit |> generate(h = 30, times = 5, bootstrap = TRUE)

sim# A tsibble: 150 x 5 [1]

# Key: Symbol, .model, .rep [5]

Symbol .model day .rep .sim

<chr> <chr> <dbl> <chr> <dbl>

1 GOOG NAIVE(Close) 253 1 761.

2 GOOG NAIVE(Close) 254 1 743.

3 GOOG NAIVE(Close) 255 1 731.

4 GOOG NAIVE(Close) 256 1 730.

5 GOOG NAIVE(Close) 257 1 728.

6 GOOG NAIVE(Close) 258 1 730.

7 GOOG NAIVE(Close) 259 1 719.

8 GOOG NAIVE(Close) 260 1 712.

9 GOOG NAIVE(Close) 261 1 706.

10 GOOG NAIVE(Close) 262 1 717.

# ℹ 140 more rowsBootstrap prediction intervals demonstration

- Here are our five simulated futures plotted:

Bootstrap prediction intervals demonstration

- Here are our five simulated futures plotted:

Bootstrap prediction intervals: bootstrapped distribution

- With these we can manufacture a “probability distribution”.

- Luckily there is a

bootstrapoption built intoforecast():

# A fable: 30 x 5 [1]

# Key: Symbol, .model [1]

Symbol .model day Close .mean

<chr> <chr> <dbl> <dist> <dbl>

1 GOOG NAIVE(Close) 253 sample[5000] 759.

2 GOOG NAIVE(Close) 254 sample[5000] 759.

3 GOOG NAIVE(Close) 255 sample[5000] 759.

4 GOOG NAIVE(Close) 256 sample[5000] 759.

5 GOOG NAIVE(Close) 257 sample[5000] 759.

6 GOOG NAIVE(Close) 258 sample[5000] 759.

7 GOOG NAIVE(Close) 259 sample[5000] 759.

8 GOOG NAIVE(Close) 260 sample[5000] 759.

9 GOOG NAIVE(Close) 261 sample[5000] 759.

10 GOOG NAIVE(Close) 262 sample[5000] 759.

# ℹ 20 more rowsBootstrap prediction intervals: bootstrapped distribution

- Note that the

.meancolumn is the mean of the bootstraps.

Bootstrapping in R

- Number of samples is controlled with the

timesoption:

bootstraps <- google_2015 |>

model(NAIVE(Close)) |>

forecast(h = 10, bootstrap = TRUE, times = 1000) |>

hilo()

kable(bootstraps)| Symbol | .model | day | Close | .mean | 80% | 95% |

|---|---|---|---|---|---|---|

| GOOG | NAIVE(Close) | 253 | sample[1000] | 759.1838 | [747.9560, 771.8960]80 | [743.7060, 781.6654]95 |

| GOOG | NAIVE(Close) | 254 | sample[1000] | 759.2800 | [742.6378, 775.2679]80 | [733.9835, 796.0598]95 |

| GOOG | NAIVE(Close) | 255 | sample[1000] | 759.3544 | [739.1602, 780.3466]80 | [730.2132, 804.6933]95 |

| GOOG | NAIVE(Close) | 256 | sample[1000] | 759.5816 | [735.9287, 783.4072]80 | [725.6406, 818.4894]95 |

| GOOG | NAIVE(Close) | 257 | sample[1000] | 759.9708 | [733.4634, 786.7182]80 | [721.3592, 829.4516]95 |

| GOOG | NAIVE(Close) | 258 | sample[1000] | 759.1356 | [729.9575, 789.9693]80 | [715.2863, 833.4845]95 |

| GOOG | NAIVE(Close) | 259 | sample[1000] | 758.8663 | [728.2751, 793.5958]80 | [711.3703, 835.3340]95 |

| GOOG | NAIVE(Close) | 260 | sample[1000] | 759.1014 | [725.5190, 797.5592]80 | [707.3571, 837.5594]95 |

| GOOG | NAIVE(Close) | 261 | sample[1000] | 759.0371 | [722.4588, 799.1424]80 | [704.7527, 841.6002]95 |

| GOOG | NAIVE(Close) | 262 | sample[1000] | 758.8098 | [720.8937, 798.4185]80 | [703.2162, 843.4535]95 |

Exercise

- Create a 90% and 99% prediction interval for the forecast you produced last time.

- Create a bootstrapped forecast for the forecast you produced last time (try a bunch of different number of bootstraps)