Forecasting tools

BUS 323 Forecasting and Risk Analysis

Forecasting workflow

- Tidy

- Model-building

- Visualize

- Specify model

- Estimate model

- Evaluate model

- Repeat as necessary

- Forecast

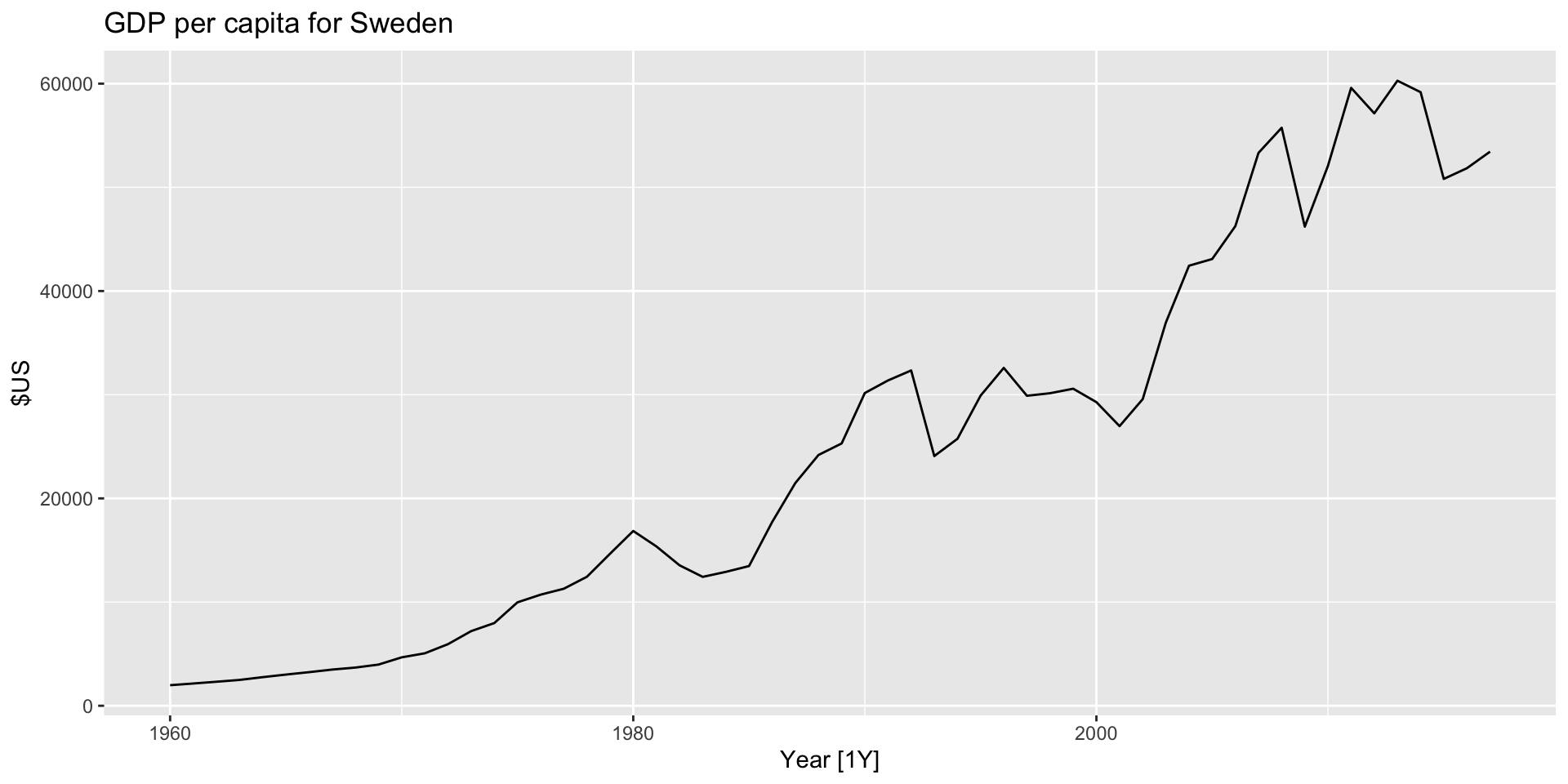

Visualize

- Let’s plot Swedish GDP per capita from the

global_economydataset.

Visualize

- Let’s plot Swedish GDP per capita from the

global_economydataset.

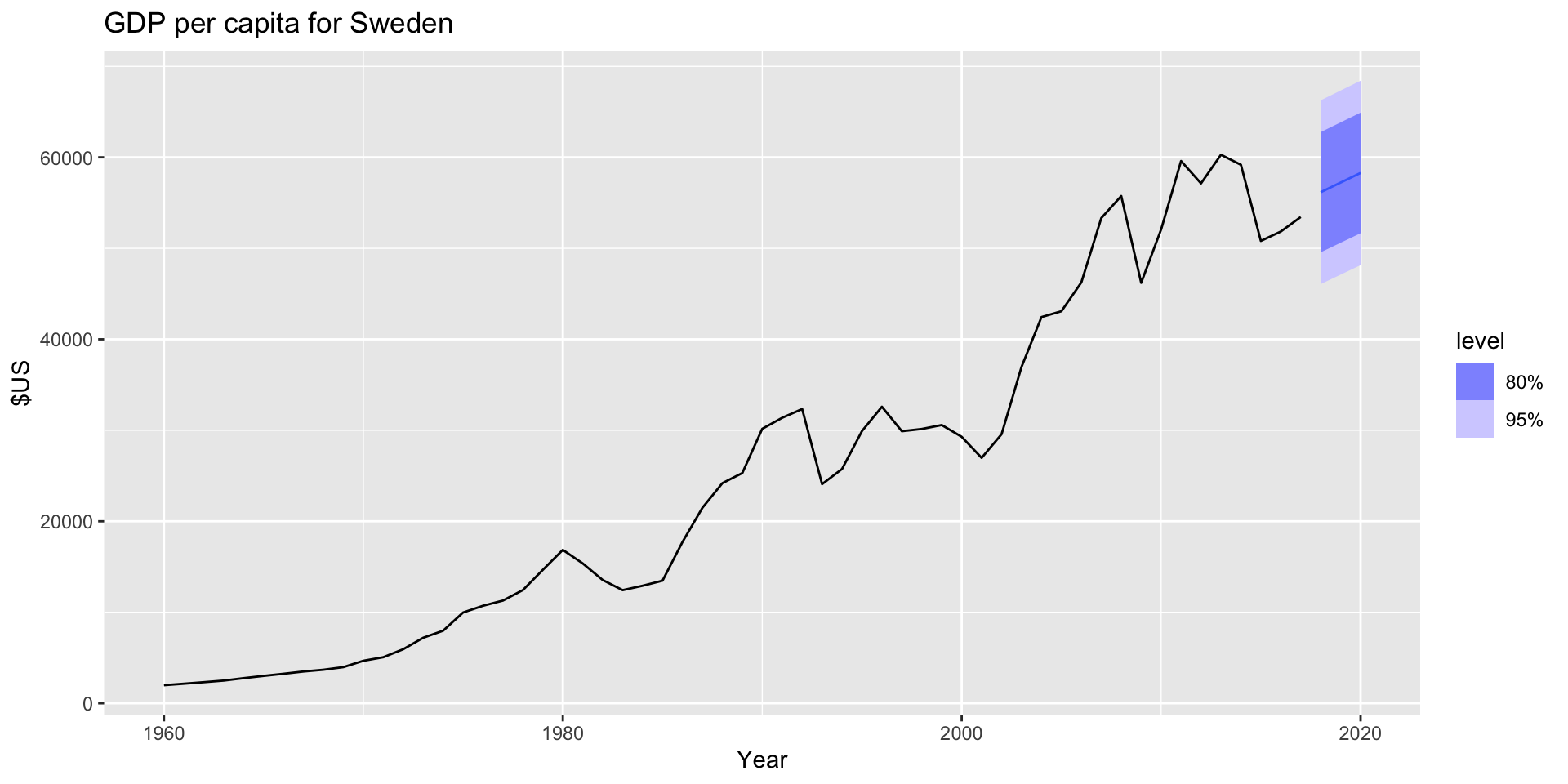

Specify a model

- Linear trend:

Estimate the model

- To estimate the model, just specify the data you want to use:

Estimate the model

Evaluate the model

- Important to check how well your model has performed. More in a bit.

Forecast

- Use

forecast()! - To specify a timeframe for your forecast, use the

hoption:

# A fable: 789 x 5 [1Y]

# Key: Country, .model [263]

Country .model Year

<fct> <chr> <dbl>

1 Afghanistan trend_model 2018

2 Afghanistan trend_model 2019

3 Afghanistan trend_model 2020

4 Albania trend_model 2018

5 Albania trend_model 2019

6 Albania trend_model 2020

7 Algeria trend_model 2018

8 Algeria trend_model 2019

9 Algeria trend_model 2020

10 American Samoa trend_model 2018

# ℹ 779 more rows

# ℹ 2 more variables: GDP_per_capita <dist>, .mean <dbl>Forecast

- The result is a “fable”, a forecast table. Each row corresponds to one forecast period. The

.meancolumn gives the average of the forecast distribution. - Plotting Sweden’s forecast:

Forecast

- The result is a “fable”, a forecast table. Each row corresponds to one forecast period. The

.meancolumn gives the average of the forecast distribution. - Plotting Sweden’s forecast:

More forecasting methods

- So far we have only talked about using regression to produce forecasts.

- Next we’ll dicsuss a few more simple forecasting methods.

Example dataset

- Use Australian clay brick production between 1970 and 2004 as example:

# A tsibble: 218 x 7 [1Q]

Quarter Beer Tobacco Bricks Cement Electricity Gas

<qtr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1956 Q1 284 5225 189 465 3923 5

2 1956 Q2 213 5178 204 532 4436 6

3 1956 Q3 227 5297 208 561 4806 7

4 1956 Q4 308 5681 197 570 4418 6

5 1957 Q1 262 5577 187 529 4339 5

6 1957 Q2 228 5651 214 604 4811 7

7 1957 Q3 236 5317 227 603 5259 7

8 1957 Q4 320 6152 222 582 4735 6

9 1958 Q1 272 5758 199 554 4608 5

10 1958 Q2 233 5641 229 620 5196 7

# ℹ 208 more rowsExample dataset

- Use

filter_index()to specify a range of the index to filter by:

# A tsibble: 140 x 7 [1Q]

Quarter Beer Tobacco Bricks Cement Electricity Gas

<qtr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1970 Q1 387 6807 386 1049 12328 12

2 1970 Q2 357 7612 428 1134 14493 18

3 1970 Q3 374 7862 434 1229 15664 23

4 1970 Q4 466 7126 417 1188 13781 20

5 1971 Q1 410 7255 385 1058 13299 19

6 1971 Q2 370 8076 433 1209 15230 23

7 1971 Q3 379 8405 453 1199 16667 28

8 1971 Q4 487 7974 436 1253 14484 24

9 1972 Q1 419 6500 399 1070 13838 24

10 1972 Q2 378 7119 461 1282 15919 34

# ℹ 130 more rowsExample dataset

- Use

select()to restrict attention only toBricks:

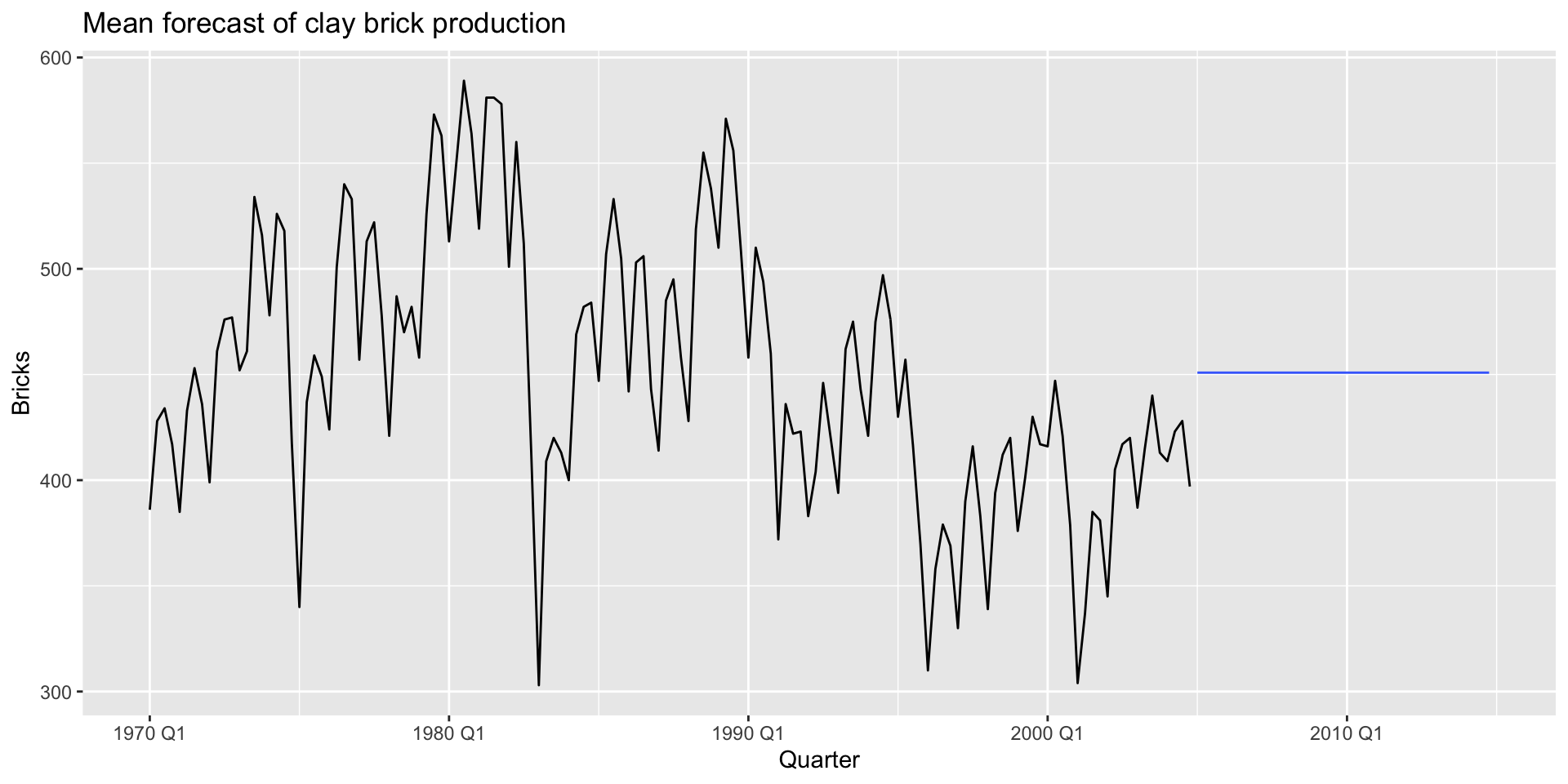

Mean method

- Use the mean of the historical data to forecast forward.

- The forecast estimate for a time series \(y\) \(h\) periods beyond the final observed period \(T\): \[ \hat{y}_{T+h|T} = \bar{y} = \frac{(y_{1} + ... + y_{t})}{T} \]

Mean method

- The function

model(MEAN())allows us to implement the mean method easily:

Mean method: forecasting

- The function

model(MEAN())allows us to implement the mean method easily:

Mean method: plotting

Mean method: plotting

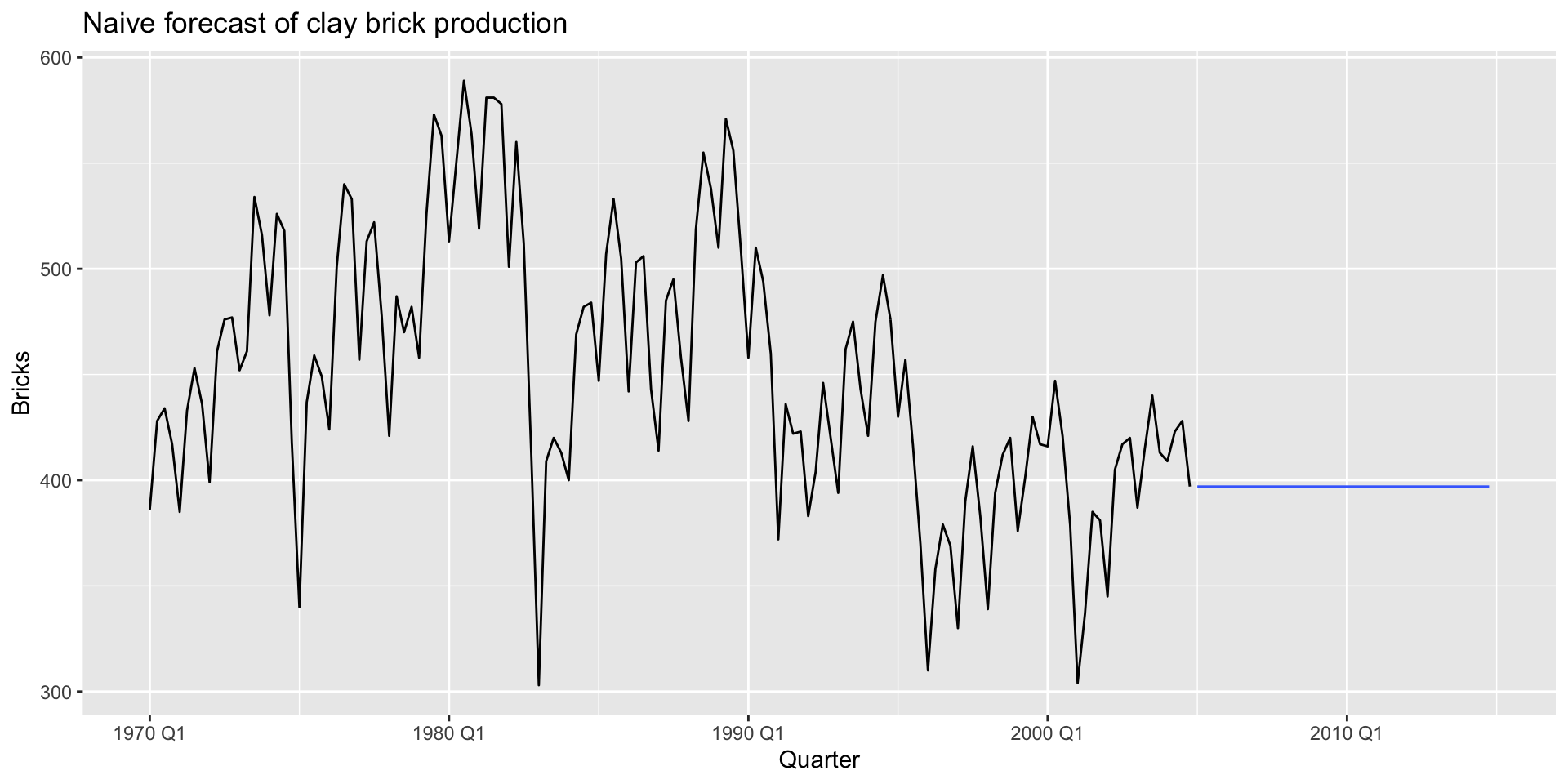

Naïve method

- Use value of last observation: \[ \hat{y}_{T+h | T} = y_{T} \]

Naïve method

- Use value of last observation: \[ \hat{y}_{T+h | T} = y_{T} \]

- AKA random walk forecasts.

Naïve implementation

- Implement with

model(NAIVE()):

Naïve forecast

- Implement with

model(NAIVE()):

Naïve plotting

- Implement with

model(NAIVE()):

Naïve plotting

- Implement with

model(NAIVE()):

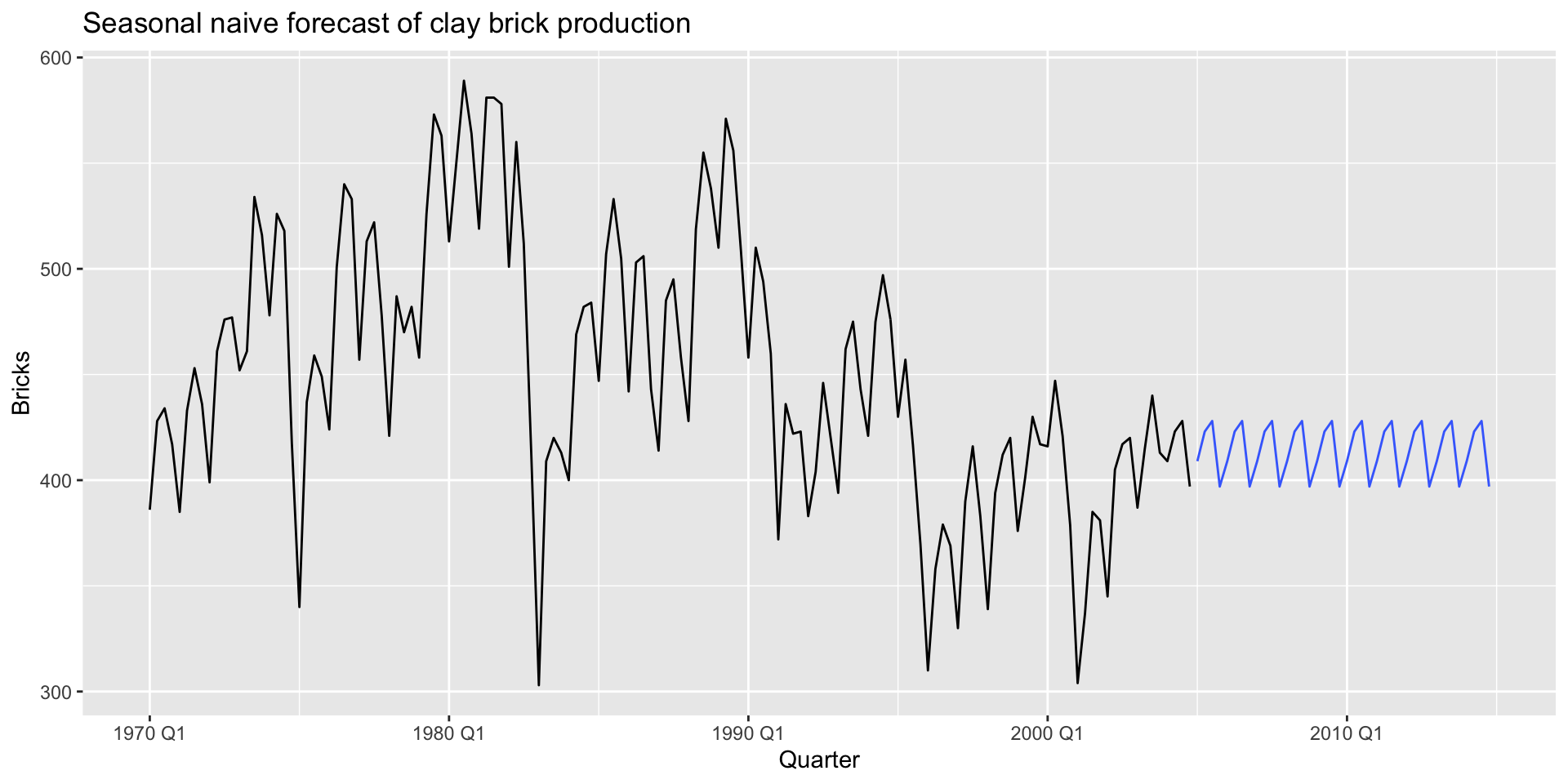

Seasonal naïve method

- Use value of last within-season observation: \[

\hat{y}_{T+h | T} = y_{T+h-m(k+1)}

\]

- \(m\): seasonal period

- \(k\): number of years in forecast prior to \(T+h\)

Seasonal naïve implementation

- Implement with

model(SNAIVE()):

Seasonal naïve forecast

# A fable: 40 x 4 [1Q]

# Key: .model [1]

.model Quarter

<chr> <qtr>

1 "SNAIVE(Bricks ~ lag(\"year\"))" 2005 Q1

2 "SNAIVE(Bricks ~ lag(\"year\"))" 2005 Q2

3 "SNAIVE(Bricks ~ lag(\"year\"))" 2005 Q3

4 "SNAIVE(Bricks ~ lag(\"year\"))" 2005 Q4

5 "SNAIVE(Bricks ~ lag(\"year\"))" 2006 Q1

6 "SNAIVE(Bricks ~ lag(\"year\"))" 2006 Q2

7 "SNAIVE(Bricks ~ lag(\"year\"))" 2006 Q3

8 "SNAIVE(Bricks ~ lag(\"year\"))" 2006 Q4

9 "SNAIVE(Bricks ~ lag(\"year\"))" 2007 Q1

10 "SNAIVE(Bricks ~ lag(\"year\"))" 2007 Q2

# ℹ 30 more rows

# ℹ 2 more variables: Bricks <dist>, .mean <dbl>Seasonal naïve plotting

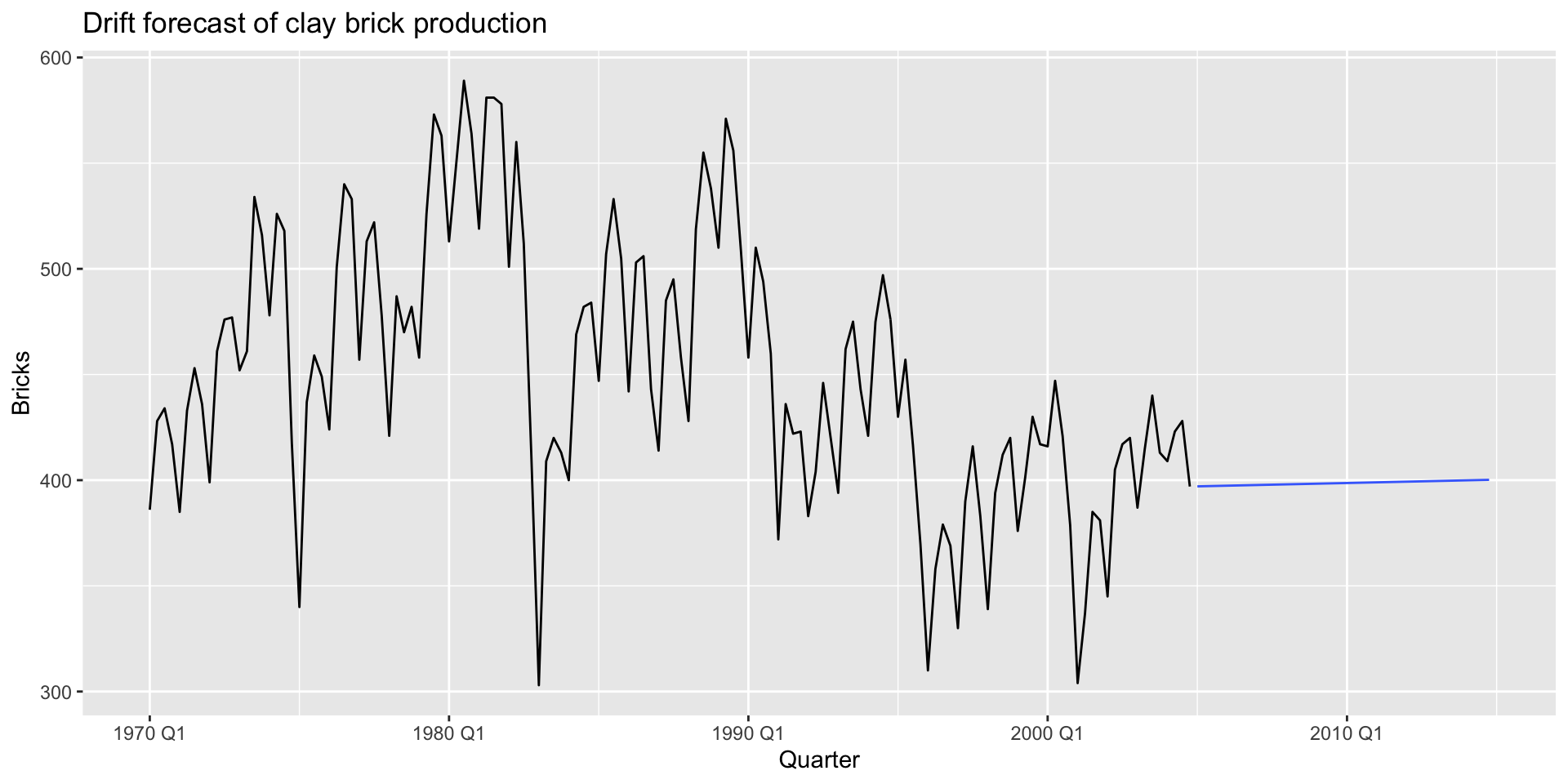

Drift method

- Naïve method allowing for “drift”

Drift method

- Naïve method allowing for “drift”

- Increase/decrease in forecast over time

Drift method

- Naïve method allowing for “drift”

- Increase/decrease in forecast over time

- Drift set to average observed change

Drift method

- Naïve method allowing for “drift”

- Increase/decrease in forecast over time

- Drift set to average observed change

- Forecast for \(T+h\): \[ \hat{y}_{T+h | T} = y_{T} + h\frac{\sum_{t=2}^{T} (y_{t} - y_{t-1})}{T-2} = y_{T} + h(\frac{y_{T}-y_{1}}{T-1}) \]

Drift implementation

- Use

model(RW()):

Drift forecast

# A fable: 40 x 4 [1Q]

# Key: .model [1]

.model Quarter

<chr> <qtr>

1 RW(Bricks ~ drift()) 2005 Q1

2 RW(Bricks ~ drift()) 2005 Q2

3 RW(Bricks ~ drift()) 2005 Q3

4 RW(Bricks ~ drift()) 2005 Q4

5 RW(Bricks ~ drift()) 2006 Q1

6 RW(Bricks ~ drift()) 2006 Q2

7 RW(Bricks ~ drift()) 2006 Q3

8 RW(Bricks ~ drift()) 2006 Q4

9 RW(Bricks ~ drift()) 2007 Q1

10 RW(Bricks ~ drift()) 2007 Q2

# ℹ 30 more rows

# ℹ 2 more variables: Bricks <dist>, .mean <dbl>Drift plotting

Drift plotting