Time series decomposition

BUS 323 Forecasting and Risk Analysis

Time series components - additive decomposition

- If we assume an additive decomposition, we can write: \[ y_{t} = S_{t} + T_{t} + R_{t} \] where \(y_{t}\) represents a time series variable’s value at period \(t\); \(S\) represents the seasonal component of the series; \(T\) represents the trend-cycle component of the series; and \(R\) represents the remainder component of the series.

Time series components - additive decomposition

- If we assume an additive decomposition, we can write: \[ y_{t} = S_{t} + T_{t} + R_{t} \] where \(y_{t}\) represents a time series variable’s value at period \(t\); \(S\) represents the seasonal component of the series; \(T\) represents the trend-cycle component of the series; and \(R\) represents the remainder component of the series.

- Additive decomposition is appropriate if the magnitude of the seasonal fluctuations or the variation around the trend-cycle does not vary with \(t\).

Time series components - multiplicative decomposition

- A multiplicative decomposition would be written: \[ y_{t} = S_{t} \times T_{t} \times R_{t} \] where all objects are as defined above.

Time series components - multiplicative decomposition

- A multiplicative decomposition would be written: \[ y_{t} = S_{t} \times T_{t} \times R_{t} \] where all objects are as defined above.

- Multiplicative decompositionis appropriate when the variation in the seasonal patter or the variation around the trend-cycle appears proportional to \(t\).

Time series components - multiplicative decomposition

- Note that \(t_{t} = S_{t} \times T_{t} \times R_{t}\) is equivalent to \[ log(y_{t}) = log(S_{t}) + log(T_{t}) + log(R_{t}) \]

- So in the case of a multiplicative decomposition, it is standard to transform the series such that the variation appears stable over time, then apply an additive decomposition.

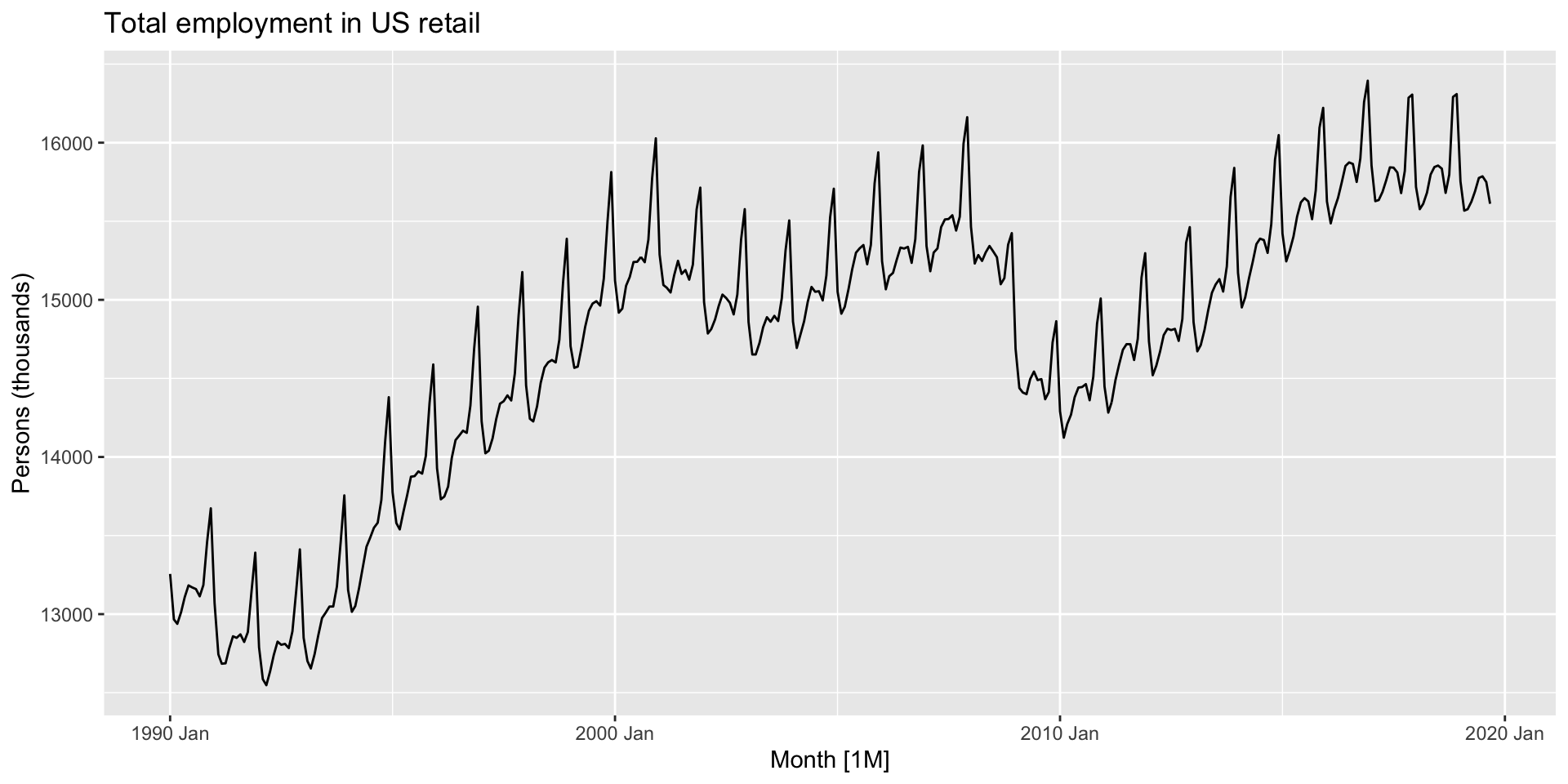

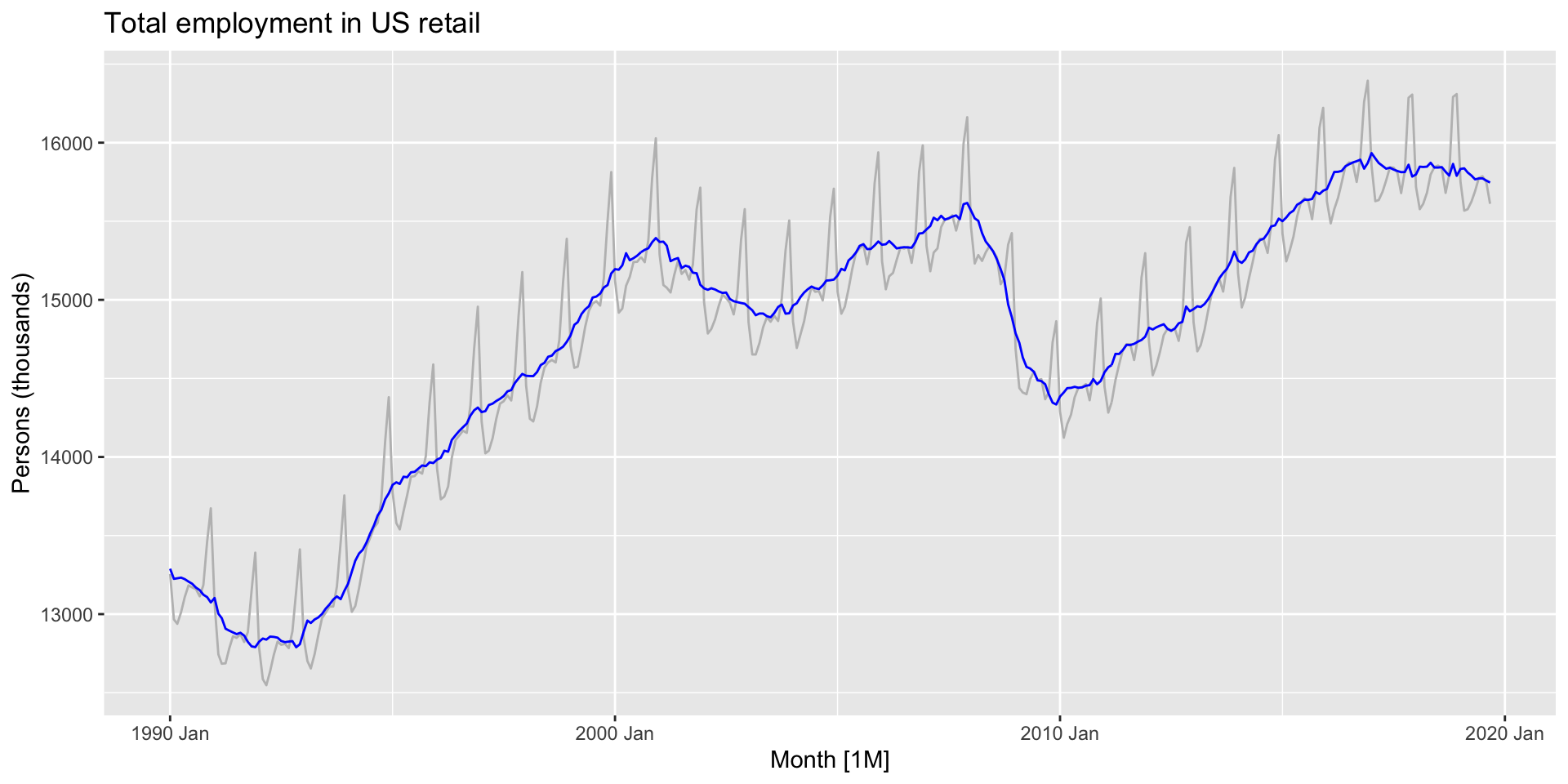

Example: US retail employment

- We’ll talk about decomposition methods soon, but let’s see the benefit first.

- Here’s a time plot of US retail employment we’ll decompose.

Example: US retail employment

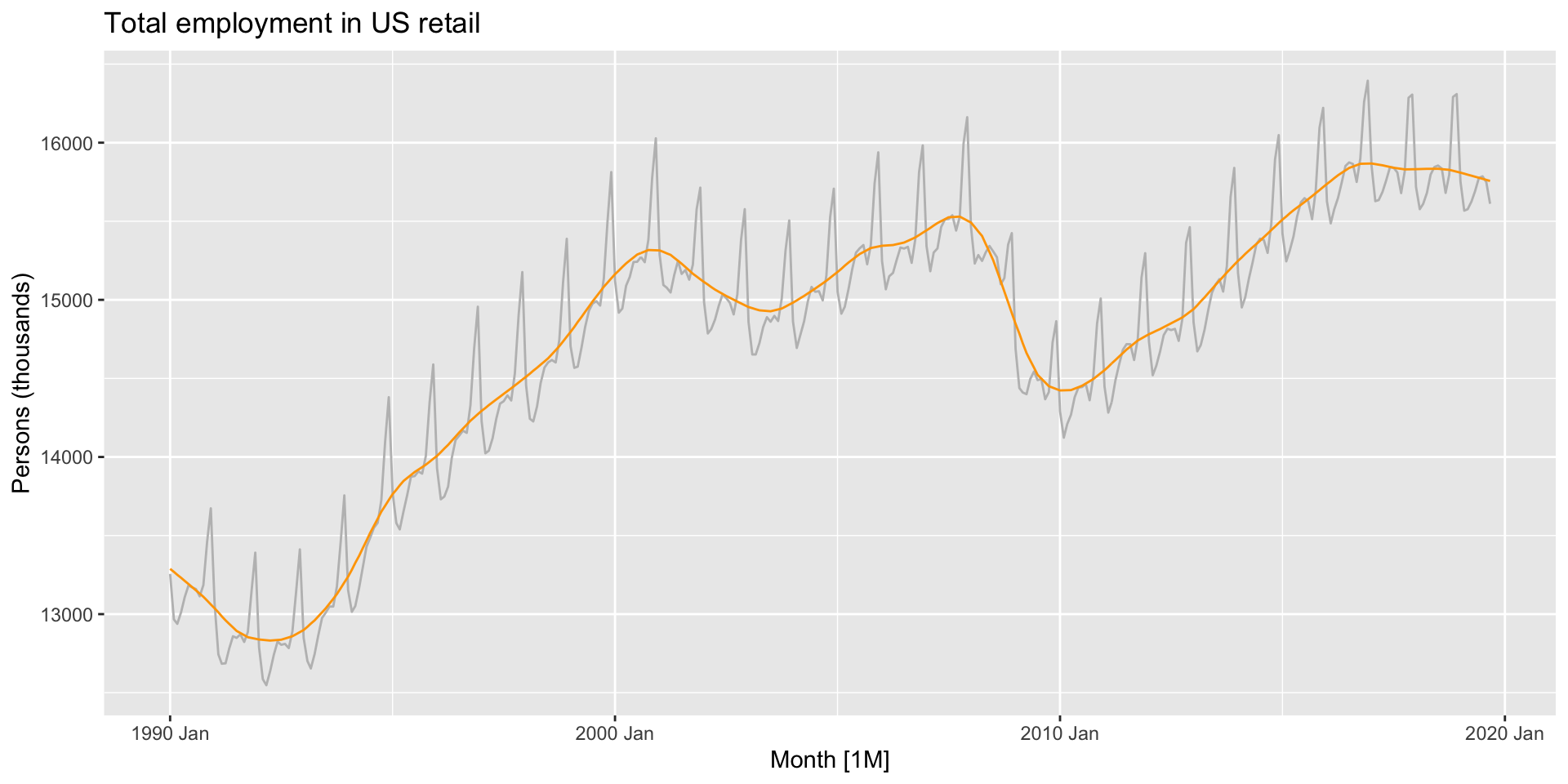

- Here’s the plot with just the trend-cycle component:

Example: US retail employment

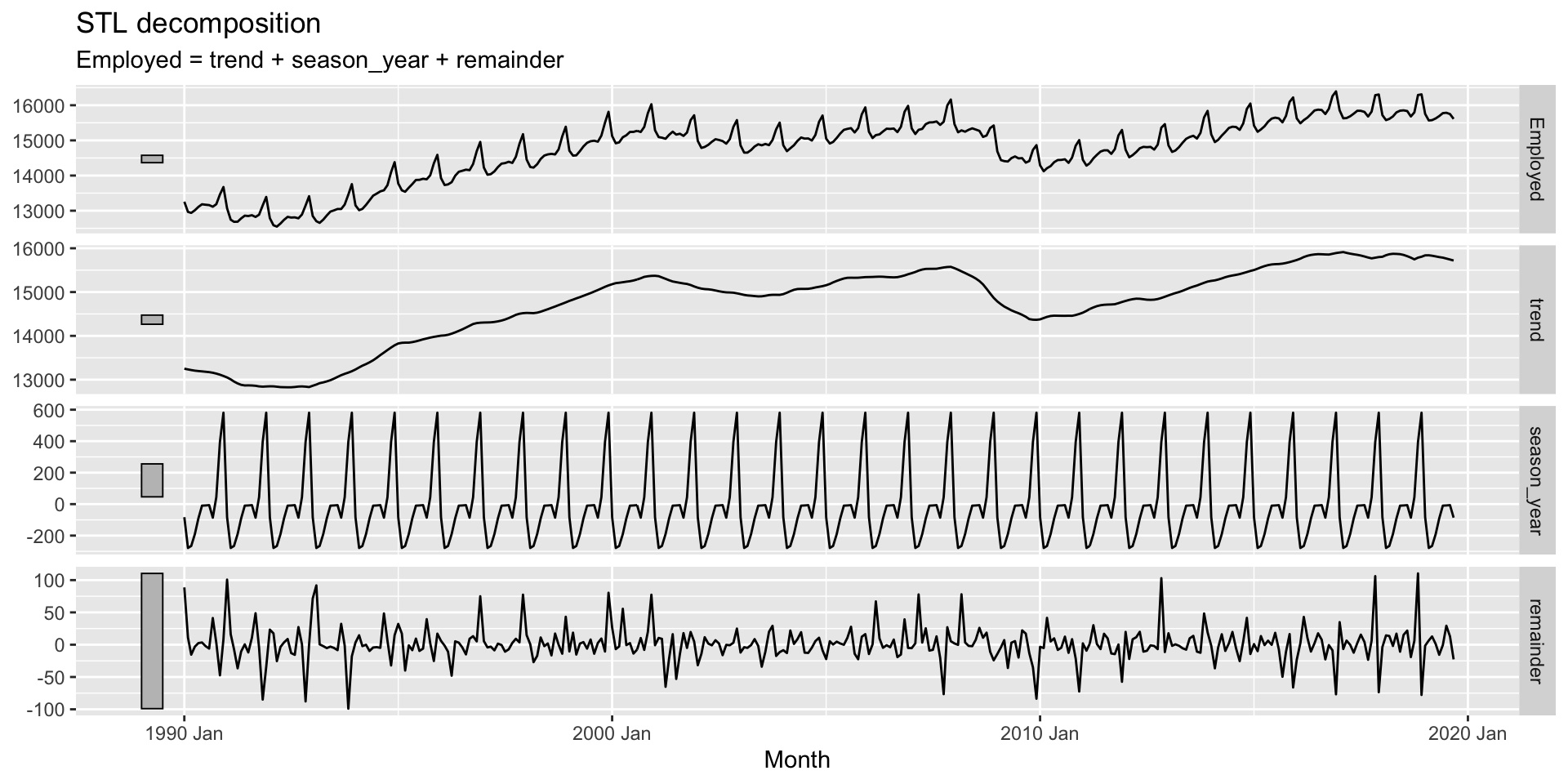

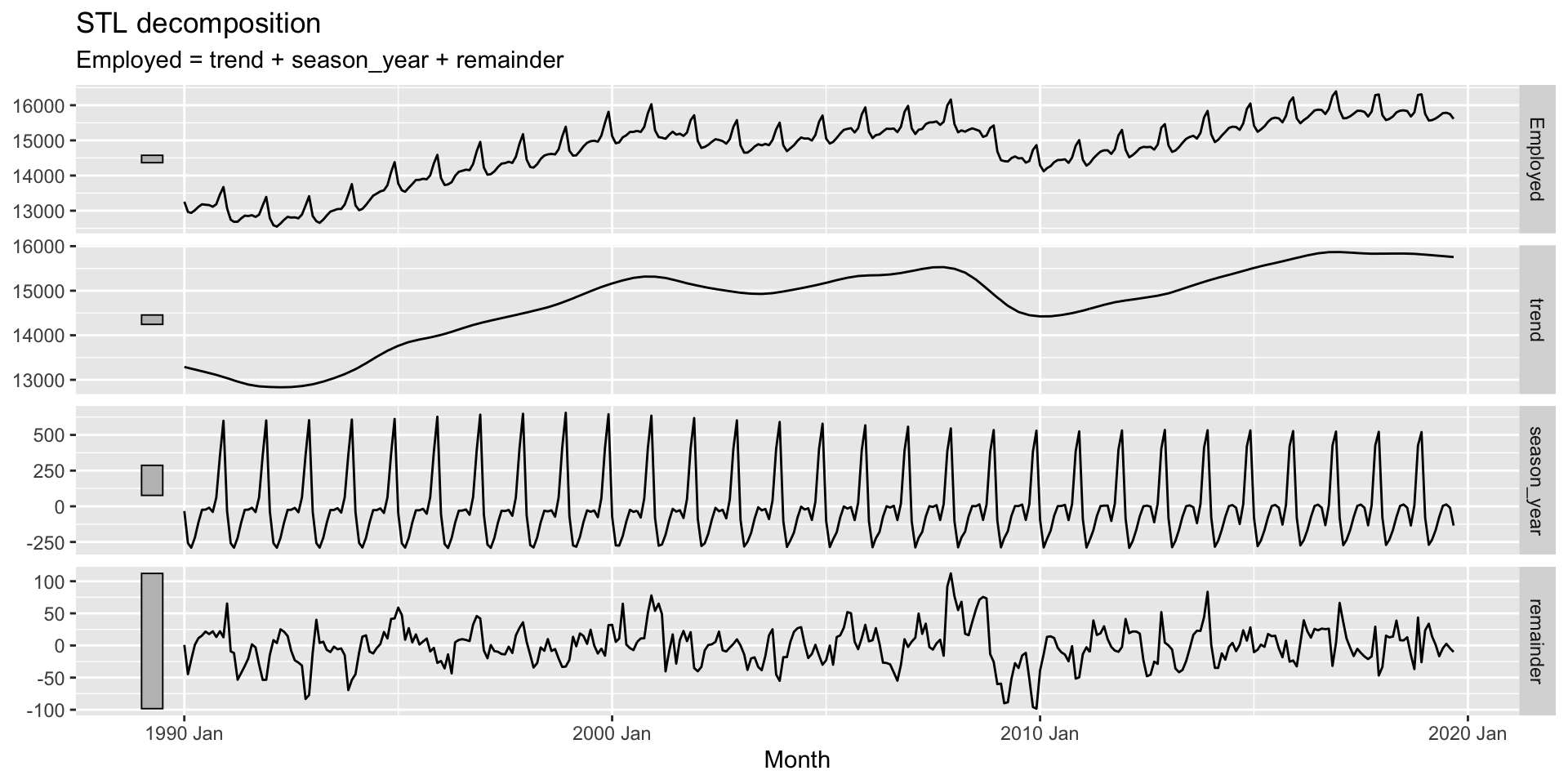

- Here’s a plot with all three decomposed components:

Example: US retail employment

- “Seasonally adjusted” data have the seasonal component of the series removed.

Example: US retail employment

- “Seasonally adjusted” data have the seasonal component of the series removed.

- For additive decomposition: \(y_{t} - S_{t}\)

Example: US retail employment

- “Seasonally adjusted” data have the seasonal component of the series removed.

- For additive decomposition: \(y_{t} - S_{t}\)

- For multiplicative decomposition: \(\frac{y_{t}}{S_{t}}\)

Example: US retail employment

- “Seasonally adjusted” data have the seasonal component of the series removed.

- For additive decomposition: \(y_{t} - S_{t}\)

- For multiplicative decomposition: \(\frac{y_{t}}{S_{t}}\)

- Here’s a seasonally adjusted retail employment time plot:

Example: US retail employment

Moving average models

- MA models are used for decomposing the trend-cycle component of a series.

Moving average models

- MA models are used for decomposing the trend-cycle component of a series.

- A moving average of order \(m\) can be written: \[ \hat{T}_{t} = \frac{1}{m} \sum_{j = -k}^{k} y_{t+j} \] where \(m=2k+1\).

Moving average models

- MA models are used for decomposing the trend-cycle component of a series.

- A moving average of order \(m\) can be written: \[ \hat{T}_{t} = \frac{1}{m} \sum_{j = -k}^{k} y_{t+j} \] where \(m=2k+1\).

- Suppose \(k=1\). Expand the above expression out to gain some intuition about it.

Moving average models

- MA models are used for decomposing the trend-cycle component of a series.

- A moving average of order \(m\) can be written: \[ \hat{T_{t}} = \frac{1}{m} \sum_{j = -k}^{k} y_{t+j} \] where \(m=2k+1\).

- Suppose \(k=1\). Expand this expression out to gain some intuition about it.

Moving averages

\[ \hat{T_{t}} = \frac{y_{t-1} + y_{t} + y_{t+1}}{2} \] The above is a MA(2) model, or a 2-MA model.

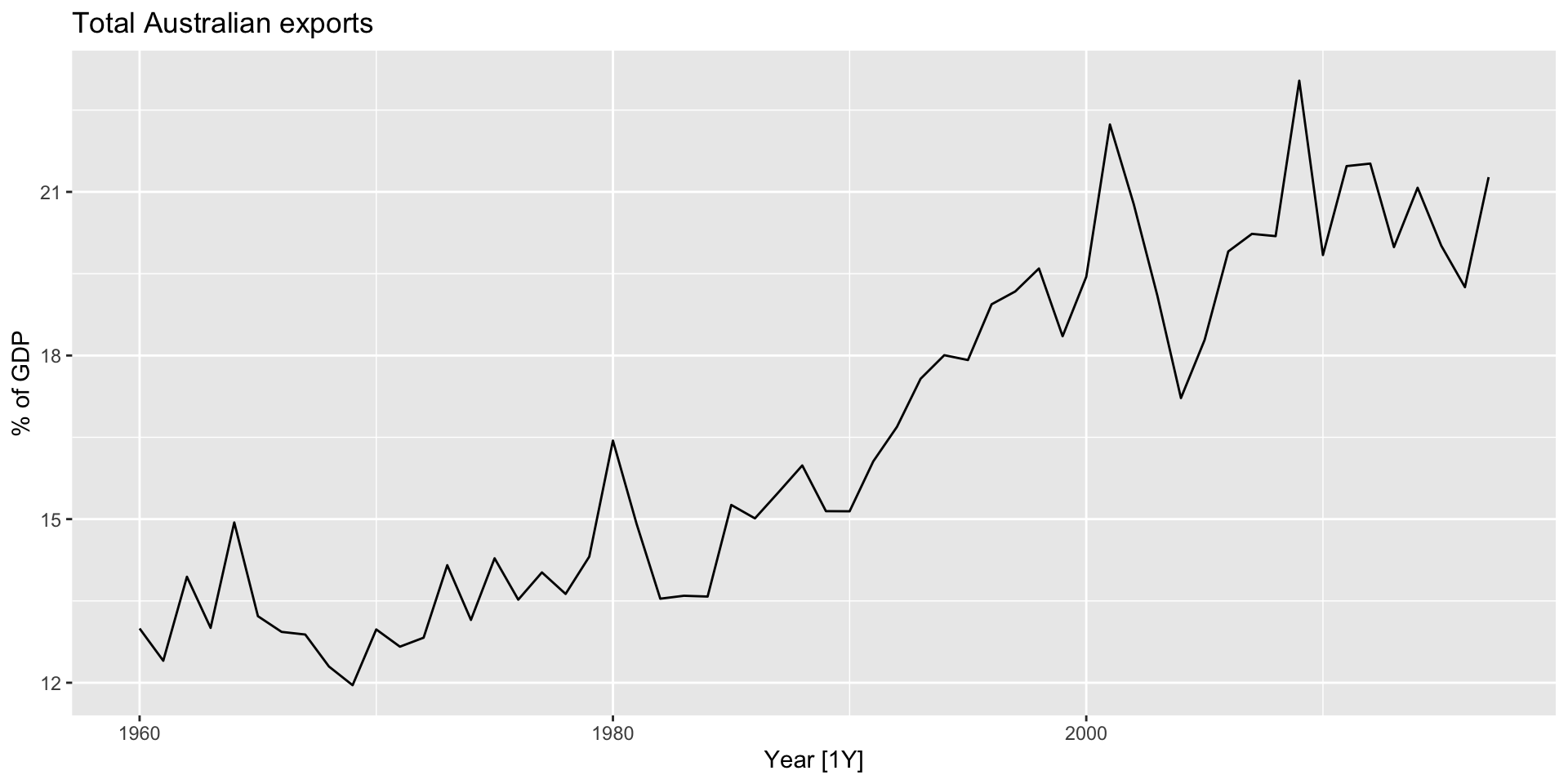

Moving averages: application

- Make an autoplot of Australian exports from the

global_economydataset:

Moving averages: application

- We can execute a 5-MA transformation manually with an iterative loop. First, we’ll define the parameters:

Moving averages: application

- Next, make a vector we’ll put the 5-MA transformation in:

Moving averages: application

- Finally, we can make a loop to feed the 5-period average of

Exportsinto each observation inma_5:

for (i in (k + 1):(length(aus_economy$Exports) - k)) {

aus_economy$ma_5[i] <- mean(aus_economy$Exports[(i - k):(i + k)])

}

aus_economy |>

select(Exports, ma_5) |>

head()# A tsibble: 6 x 3 [1Y]

Exports ma_5 Year

<dbl> <dbl> <dbl>

1 13.0 NA 1960

2 12.4 NA 1961

3 13.9 13.5 1962

4 13.0 13.5 1963

5 14.9 13.6 1964

6 13.2 13.4 1965Moving averages: application

- We can also do this automatically using

slide_dbl()from thesliderpackage.- The function applies a given function (for us, it will be

mean) to “sliding” time windows.

- The function applies a given function (for us, it will be

Moving averages: application

We can also do this automatically using

slide_dbl()from thesliderpackage.- The function applies a given function (for us, it will be

mean) to “sliding” time windows.

- The function applies a given function (for us, it will be

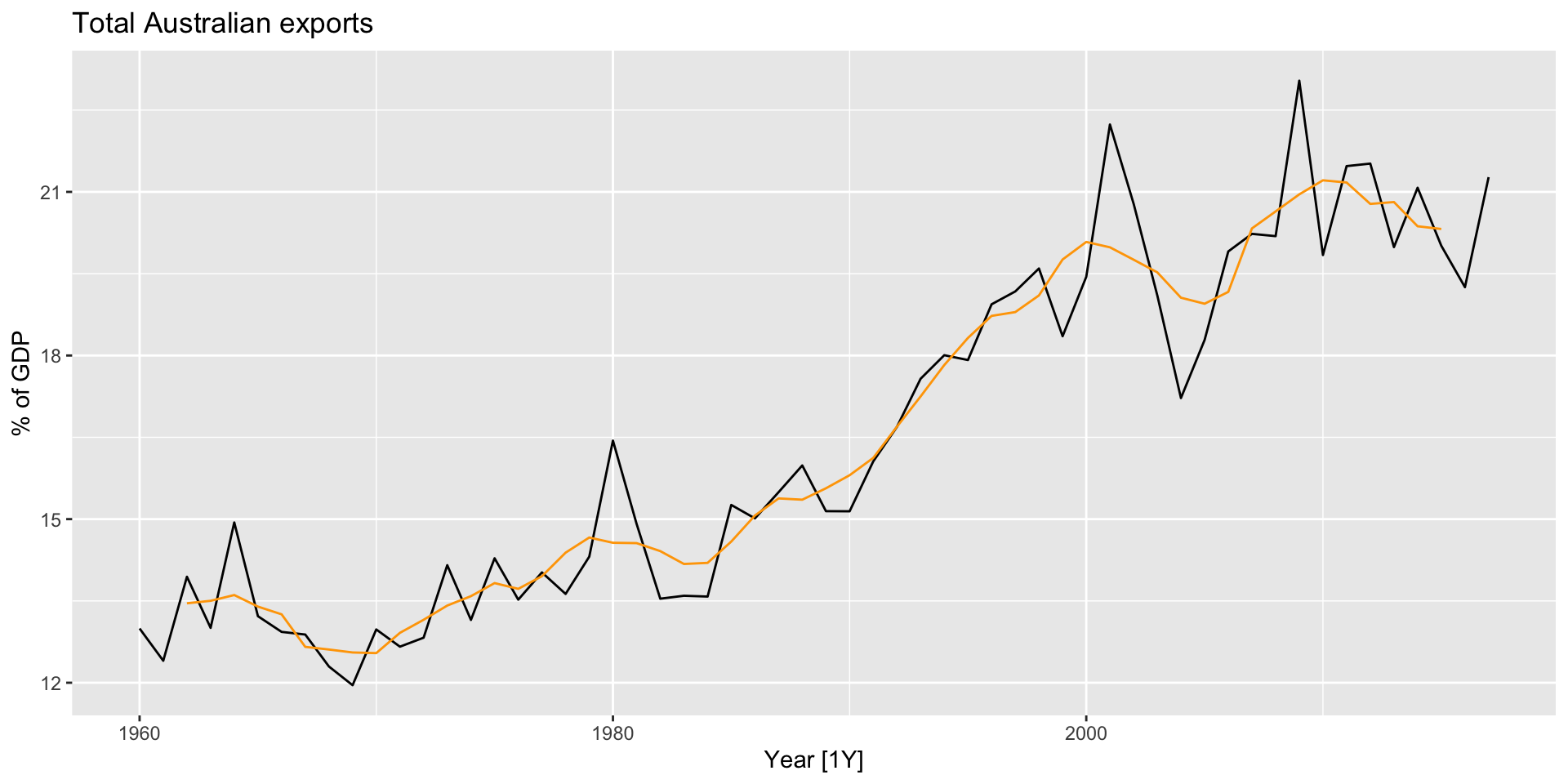

Moving averages: application

- Let’s plot the trend-cycle component estimates from our 5-MA object along with the time plot of exports:

Moving averages of moving averages

- If you use an even-order MA, you can take another even-order MA of the MA to make the whole process symmetric.

Moving averages of moving averages

- If you use an even-order MA, you can take another even-order MA of the MA to make the whole process symmetric.

- Consider a 4-MA followed by a 2-MA: \[ \hat{T_{t}} = \frac{1}{2} [\frac{1}{4} (y_{t-1} + y_{t} + y_{t+1} + y_{t+2}) + \frac{1}{4} (y_{t-2} + y_{t-1} + y_{t} + y_{t+1})] \\ = \frac{1}{8} y_{t-2} + \frac{1}{4} y_{t-1} + \frac{1}{4} y_{t} + \frac{1}{4} y_{t+1} + \frac{1}{8} y_{t+2} \] ## Moving averages of moving averages

- If you use an even-order MA, you can take another even-order MA of the MA to make the whole process symmetric.

- Consider a 4-MA followed by a 2-MA: \[ \hat{T_{t}} = \frac{1}{2} [\frac{1}{4} (y_{t-1} + y_{t} + y_{t+1} + y_{t+2}) + \frac{1}{4} (y_{t-2} + y_{t-1} + y_{t} + y_{t+1})] \\ = \frac{1}{8} y_{t-2} + \frac{1}{4} y_{t-1} + \frac{1}{4} y_{t} + \frac{1}{4} y_{t+1} + \frac{1}{8} y_{t+2} \]

- Why might this be useful?

Estimating the trend-cycle with seasonal data

- When applying the 2x4-MA to quarterly data, each quarter is given equal weight. As a result the seasonal variation will be averaged out.

Estimating the trend-cycle with seasonal data

- When applying the 2x4-MA to quarterly data, each quarter is given equal weight. As a result the seasonal variation will be averaged out.

- You can use a 2x12-MA to estimate the trend-cycle of monthly data with annual seasonality.

Estimating the trend-cycle with seasonal data

- When applying the 2x4-MA to quarterly data, each quarter is given equal weight. As a result the seasonal variation will be averaged out.

- You can use a 2x12-MA to estimate the trend-cycle of monthly data with annual seasonality.

- A 7-MA to estimate the trend-cycle of daily data with weekly seasonality.

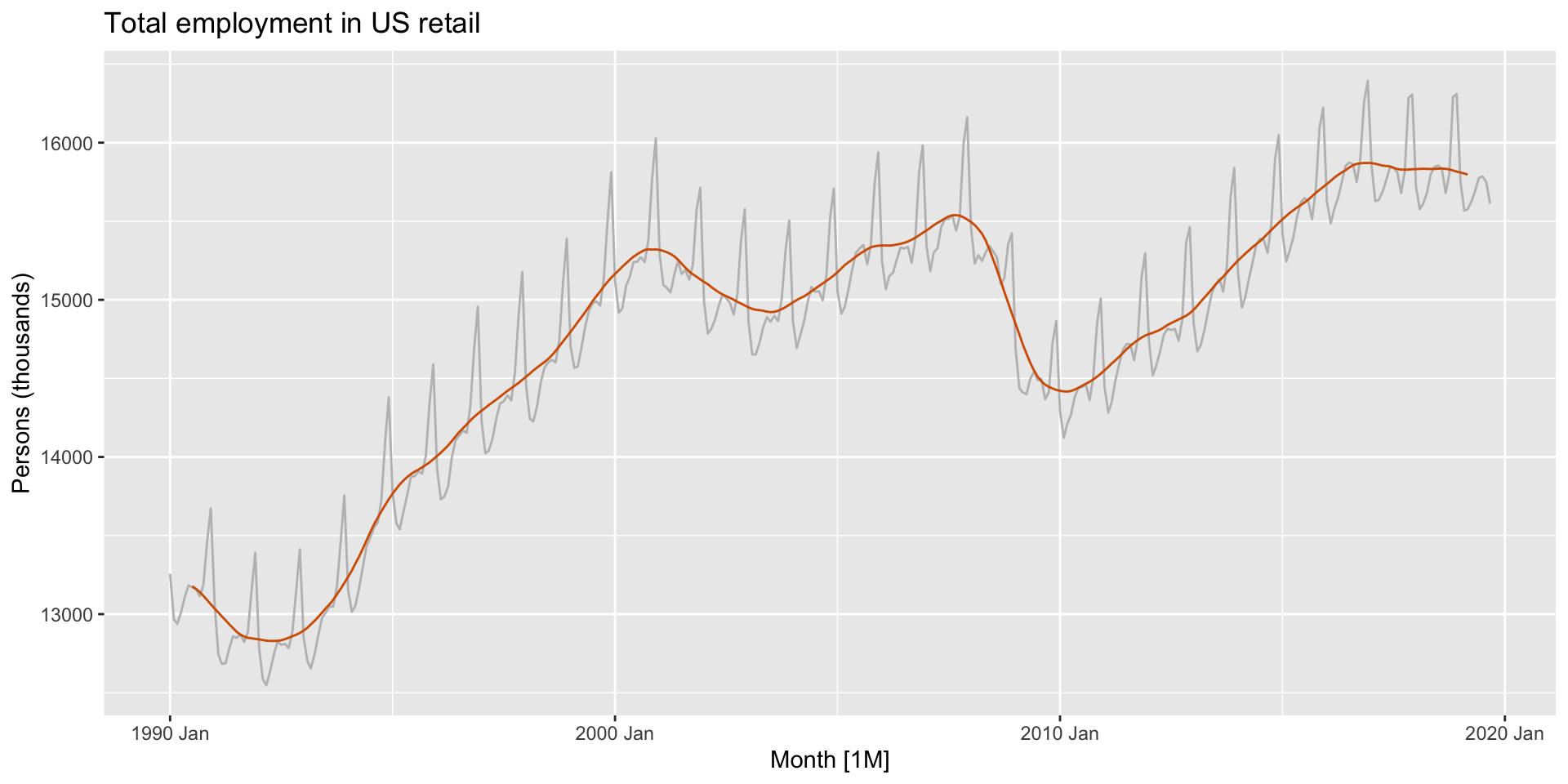

Example: US retail employment

us_retail_employment_ma <- us_retail_employment |>

mutate(

`12-MA` = slider::slide_dbl(Employed, mean,

.before = 5, .after = 6, .complete = TRUE),

`2x12-MA` = slider::slide_dbl(`12-MA`, mean,

.before = 1, .after = 0, .complete = TRUE)

)

us_retail_employment_ma |>

autoplot(Employed, colour = "gray") +

geom_line(aes(y = `2x12-MA`), colour = "#D55E00") +

labs(y = "Persons (thousands)",

title = "Total employment in US retail")Example: US retail employment

Classical decomposition

- Assume seasonal period \(m\).

- Assume constant seasonal component across time.

Classical decomposition

- Assume seasonal period \(m\).

- Assume constant seasonal component across time.

- If \(m\) is even, compute \(\hat{T_{t}}\) using a \(2 \times m\)-MA. If \(m\) is odd, compute \(\hat{T_{t}}\) using a \(m\)-MA.

Classical decomposition

- Assume seasonal period \(m\).

- Assume constant seasonal component across time.

- If \(m\) is even, compute \(\hat{T_{t}}\) using a \(2 \times m\)-MA. If \(m\) is odd, compute \(\hat{T_{t}}\) using a \(m\)-MA.

- Calculate the detrended series \(y_{t} - \hat{T_{t}}\).

Classical decomposition

- Assume seasonal period \(m\).

- Assume constant seasonal component across time.

- If \(m\) is even, compute \(\hat{T_{t}}\) using a \(2 \times m\)-MA. If \(m\) is odd, compute \(\hat{T_{t}}\) using a \(m\)-MA.

- Calculate the detrended series \(y_{t} - \hat{T_{t}}\).

- Average the within-season detrended values to obtain \(\hat{S_{t}}\).

Classical decomposition

- Assume seasonal period \(m\).

- Assume constant seasonal component across time.

- If \(m\) is even, compute \(\hat{T_{t}}\) using a \(2 \times m\)-MA. If \(m\) is odd, compute \(\hat{T_{t}}\) using a \(m\)-MA.

- Calculate the detrended series \(y_{t} - \hat{T_{t}}\).

- Average the within-season detrended values to obtain \(\hat{S_{t}}\).

- Calculate the remainder component \(\hat{R_{t}} = y_{t} - \hat{T_{t}} - \hat{S_{t}}\).

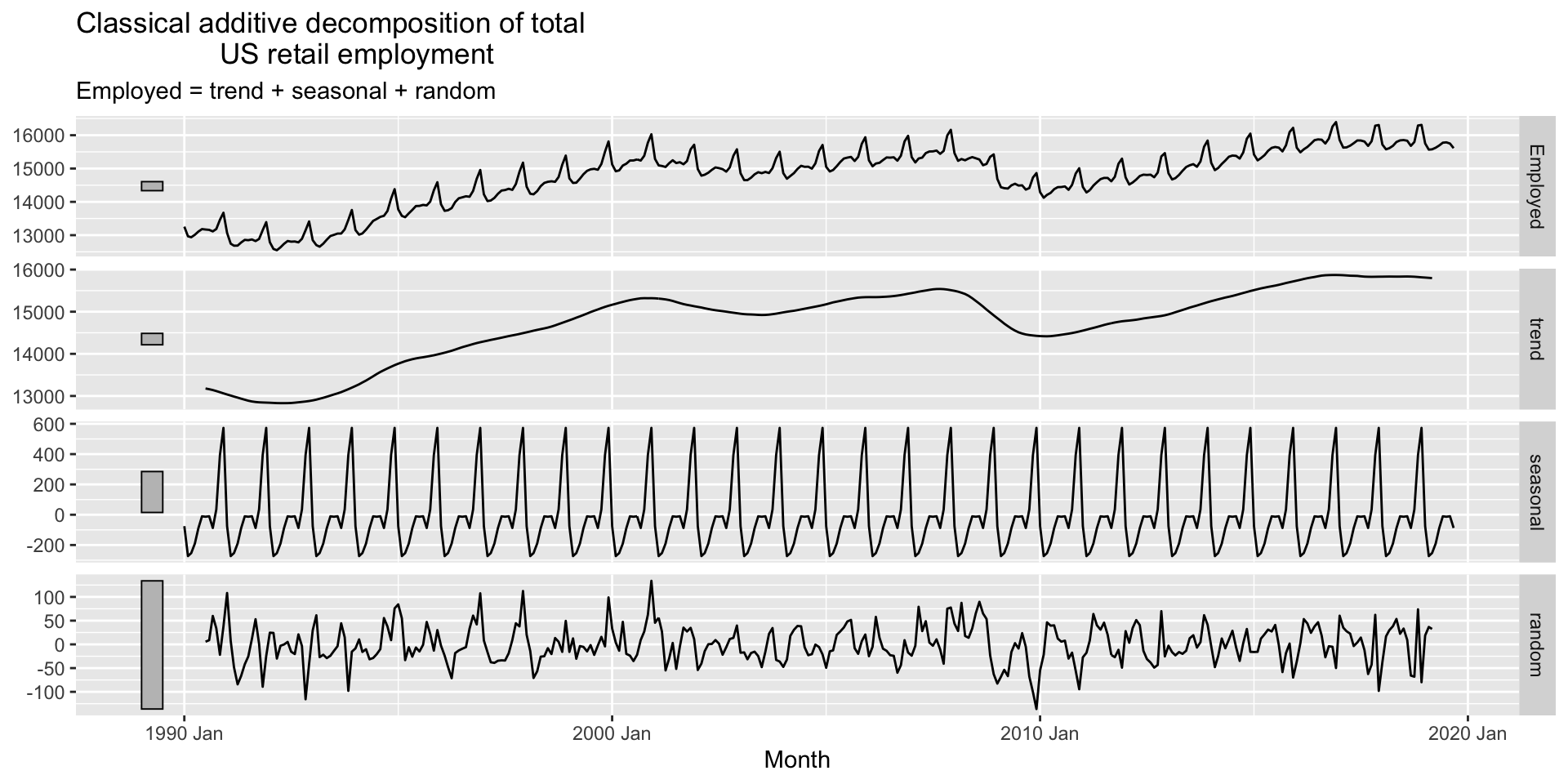

Classical decomposition example

- Luckily there is an R function that does all this for us:

classical_decomposition():

Classical decomposition example

- Luckily there is an R function that does all this for us:

classical_decomposition():

Classical decomposition limitations

- Can’t estimate the trend-cycle for the first few and last few observations.

Classical decomposition limitations

- Can’t estimate the trend-cycle for the first few and last few observations.

- The trend-cycle estimate tends to over-smooth rapid rises and falls.

Classical decomposition limitations

- Can’t estimate the trend-cycle for the first few and last few observations.

- The trend-cycle estimate tends to over-smooth rapid rises and falls.

- The assumption that the seasonal component remans constant over time is often unrealistic.

Classical decomposition limitations

- Can’t estimate the trend-cycle for the first few and last few observations.

- The trend-cycle estimate tends to over-smooth rapid rises and falls.

- The assumption that the seasonal component remans constant over time is often unrealistic.

- Not robust to outliers.

STL decomposition

- STL: “Seasonal and Trend decomposition using Loess”

STL decomposition

- STL: “Seasonal and Trend decomposition using Loess”

- loess: a non-parametric local linear regression method for estimating nonlinear relationships

STL decomposition

- STL: “Seasonal and Trend decomposition using Loess”

- loess: a non-parametric local linear regression method for estimating nonlinear relationships

- Note that STL only works for aditive decompositions

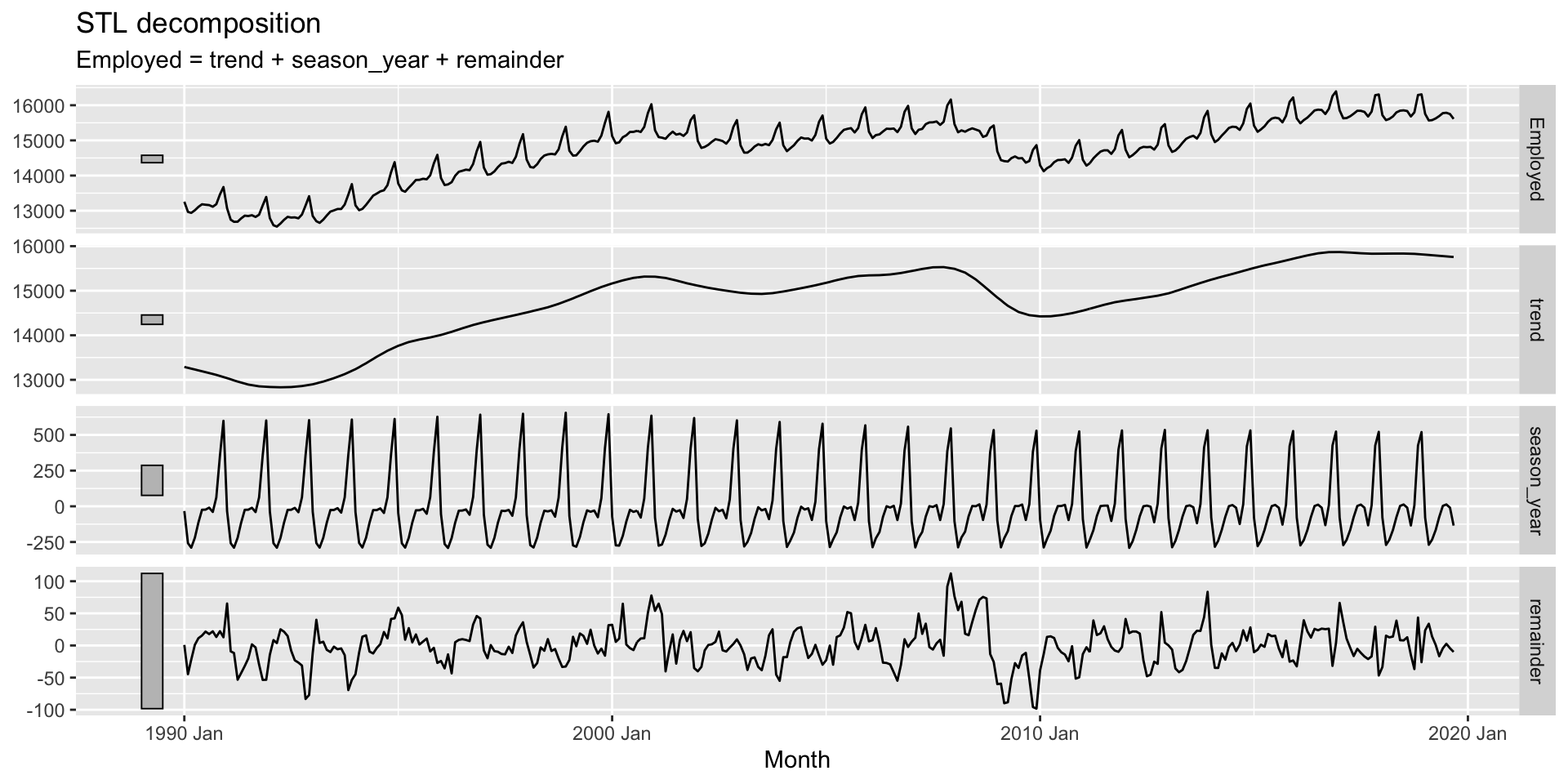

STL decomposition: example

- Try out the following:

STL decomposition: example

STL decomposition: parameters

- Trend-cycle window:

trend(window = x)

STL decomposition: parameters

- Trend-cycle window:

trend(window = x)- The number of consecutive observations to use when estimating the trend-cycle component

STL decomposition: parameters

- Trend-cycle window:

trend(window = x)- The number of consecutive observations to use when estimating the trend-cycle component

- Seasonal window:

season(window = x)

STL decomposition: parameters

- Trend-cycle window:

trend(window = x)- The number of consecutive observations to use when estimating the trend-cycle component

- Seasonal window:

season(window = x)- The number of consecutive years to use in estimating each value in the seasonal component.

STL decomposition: parameters

- Trend-cycle window:

trend(window = x)- The number of consecutive observations to use when estimating the trend-cycle component

- Seasonal window:

season(window = x)- The number of consecutive years to use in estimating each value in the seasonal component.

season(window = 'periodic')forces the component to be identical across years.

STL decomposition: parameters

- Trend-cycle window:

trend(window = x)- The number of consecutive observations to use when estimating the trend-cycle component

- Seasonal window:

season(window = x)- The number of consecutive years to use in estimating each value in the seasonal component.

season(window = 'periodic')forces the component to be identical across years.

- Robustness:

robust = TRUE- Reduces the influence of outliers by using robust loess.

STL decomposition: example, again

- Try the following:

STL decomposition: example, again