# A tsibble: 6 x 6 [1Q]

Quarter Consumption Income Production Savings Unemployment

<qtr> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1970 Q1 0.619 1.04 -2.45 5.30 0.9

2 1970 Q2 0.452 1.23 -0.551 7.79 0.5

3 1970 Q3 0.873 1.59 -0.359 7.40 0.5

4 1970 Q4 -0.272 -0.240 -2.19 1.17 0.700

5 1971 Q1 1.90 1.98 1.91 3.54 -0.100

6 1971 Q2 0.915 1.45 0.902 5.87 -0.100Time series regression in R

BUS 323 Forecasting and Risk Analysis

Getting set up

- We’ll work with the

us_changedataset today.

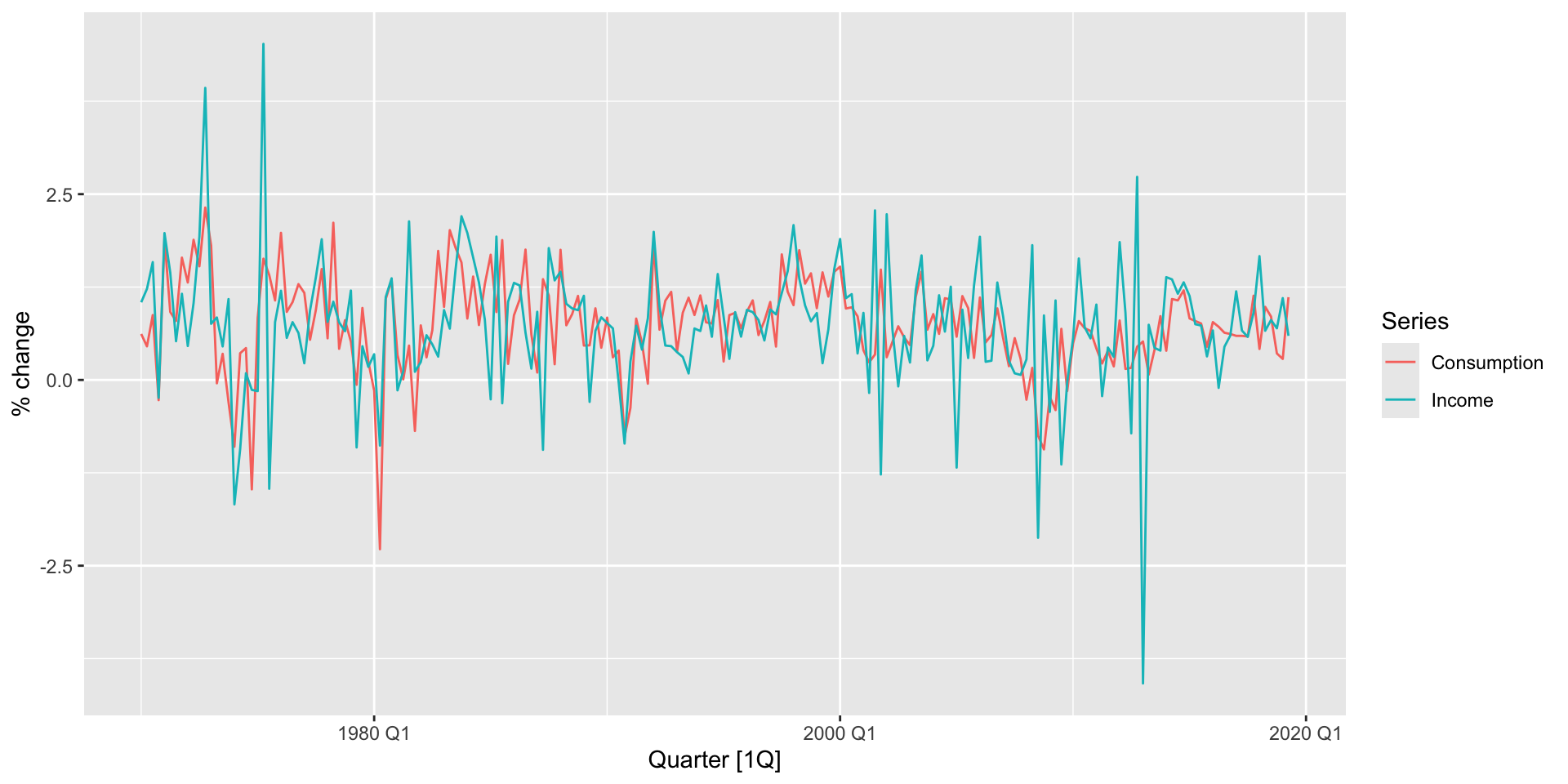

head(us_change)Plotting multiple series on a time plot

autoplotplots a single series across time.- We want to plot consumption and income change on one plot.

- To plot two, we’ll have to transform the data such that both series correspond to one variable. We can use

pivot_longer()to do so.

us_change |>

pivot_longer(c(Consumption, Income), names_to="Series")Plotting multiple series on a time plot

- Great, now we can autoplot

value

us_change |>

pivot_longer(c(Consumption, Income), names_to="Series") |>

autoplot(value) +

labs(y = "% change")

Plotting a line of best fit

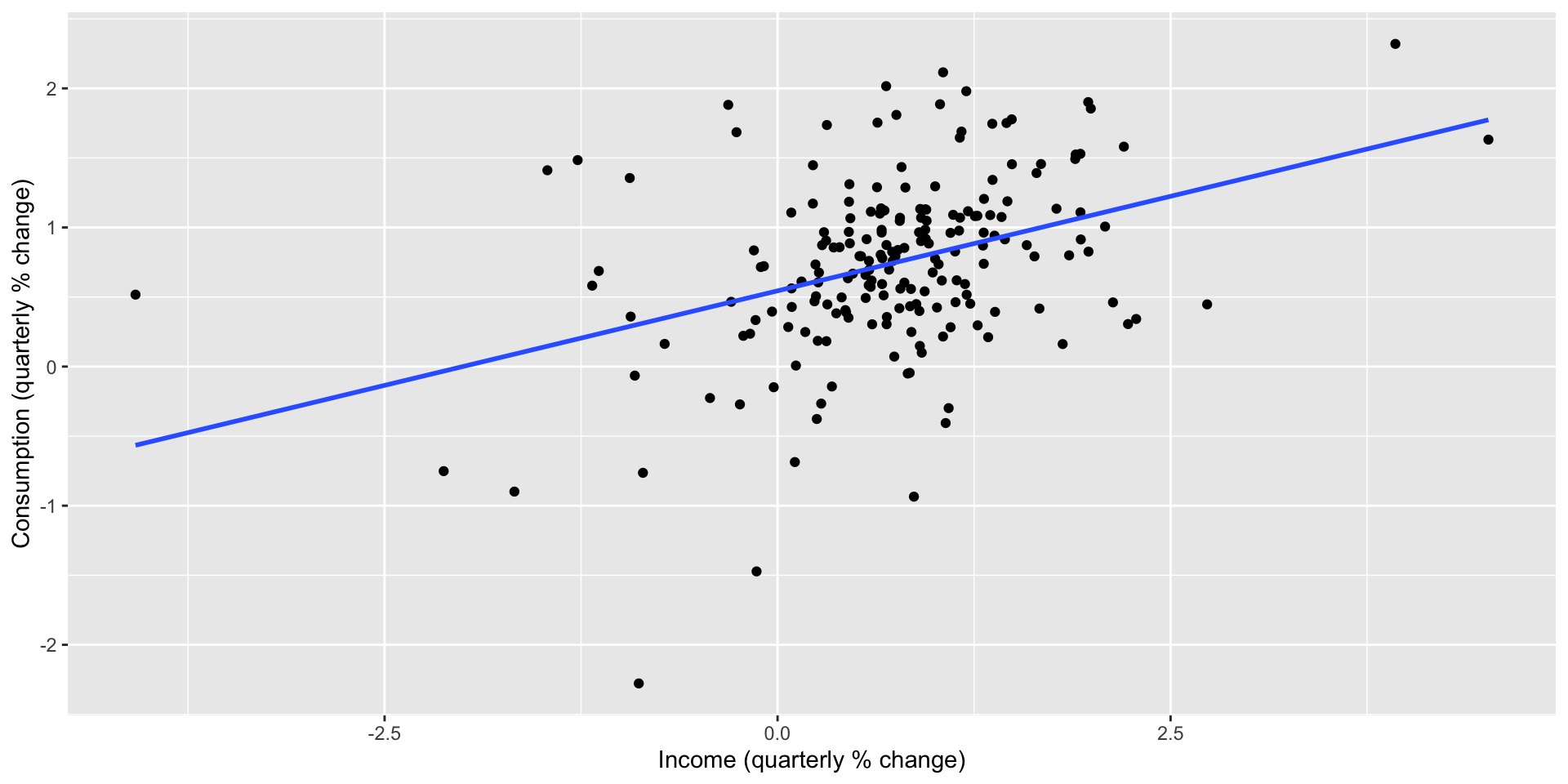

- Adding a regression line to a scatterplot is simple with

geom_smoothand themethod = "lm"option:

us_change |>

ggplot(aes(x = Income, y = Consumption)) +

labs(y = "Consumption (quarterly % change)",

x = "Income (quarterly % change)") +

geom_point() +

geom_smooth(method = "lm", se = FALSE)Plotting a line of best fit

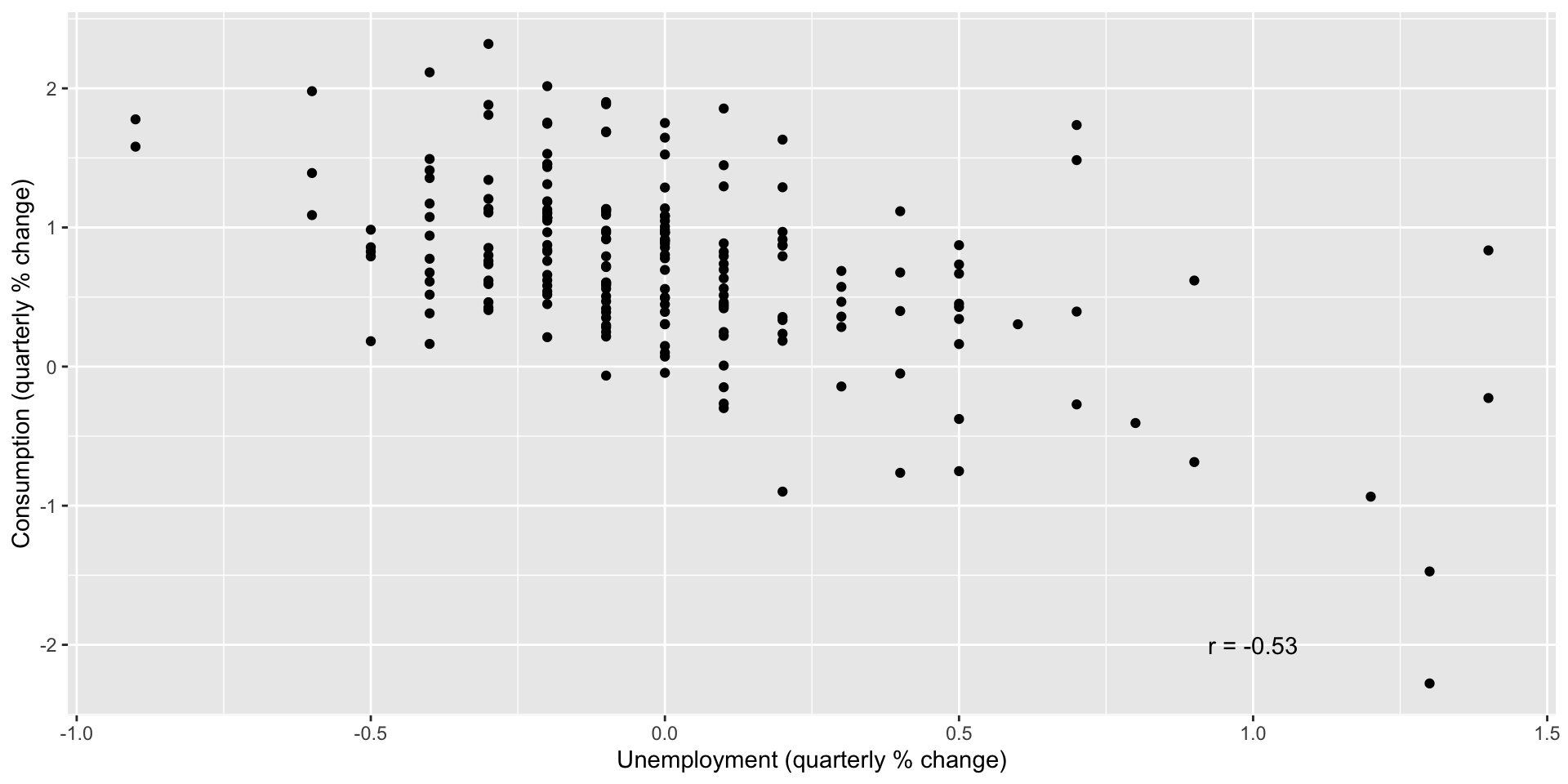

Estimating a regression function

- Suppose we want to estimate the following regression fucntion: \(y_{t} = \beta_{0} + \beta_{1} x_{t} + \epsilon_{t}\).

- Use

TSLM()to do so:

us_change |>

model(TSLM(Consumption ~ Income)) |>

report()- Use

TSLM()instead oflm()because it has time series-friendly options built in.

Regression results

Series: Consumption

Model: TSLM

Residuals:

Min 1Q Median 3Q Max

-2.58236 -0.27777 0.01862 0.32330 1.42229

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.54454 0.05403 10.079 < 2e-16 ***

Income 0.27183 0.04673 5.817 2.4e-08 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.5905 on 196 degrees of freedom

Multiple R-squared: 0.1472, Adjusted R-squared: 0.1429

F-statistic: 33.84 on 1 and 196 DF, p-value: 2.4022e-08Multiple linear regression

- Regression with more than one regressor is called multiple regression: \(y_{t} = \beta_{0} + \beta_{1} x_{1,t} + \beta_{2} x_{2,t} + ... + \beta_{k} x_{k,t} + \epsilon_{t}\)

- Coefficients reflect conditional marginal effects

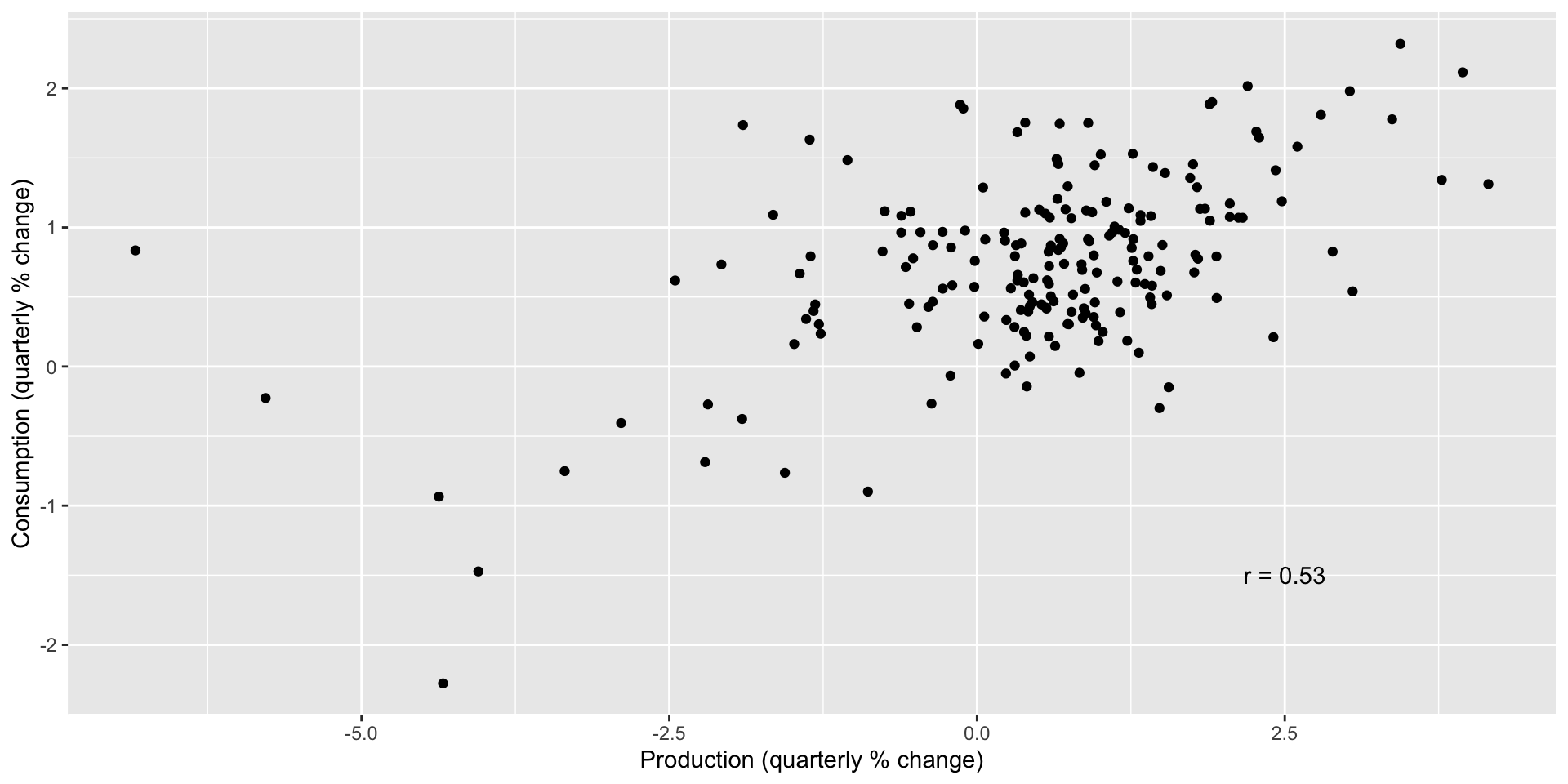

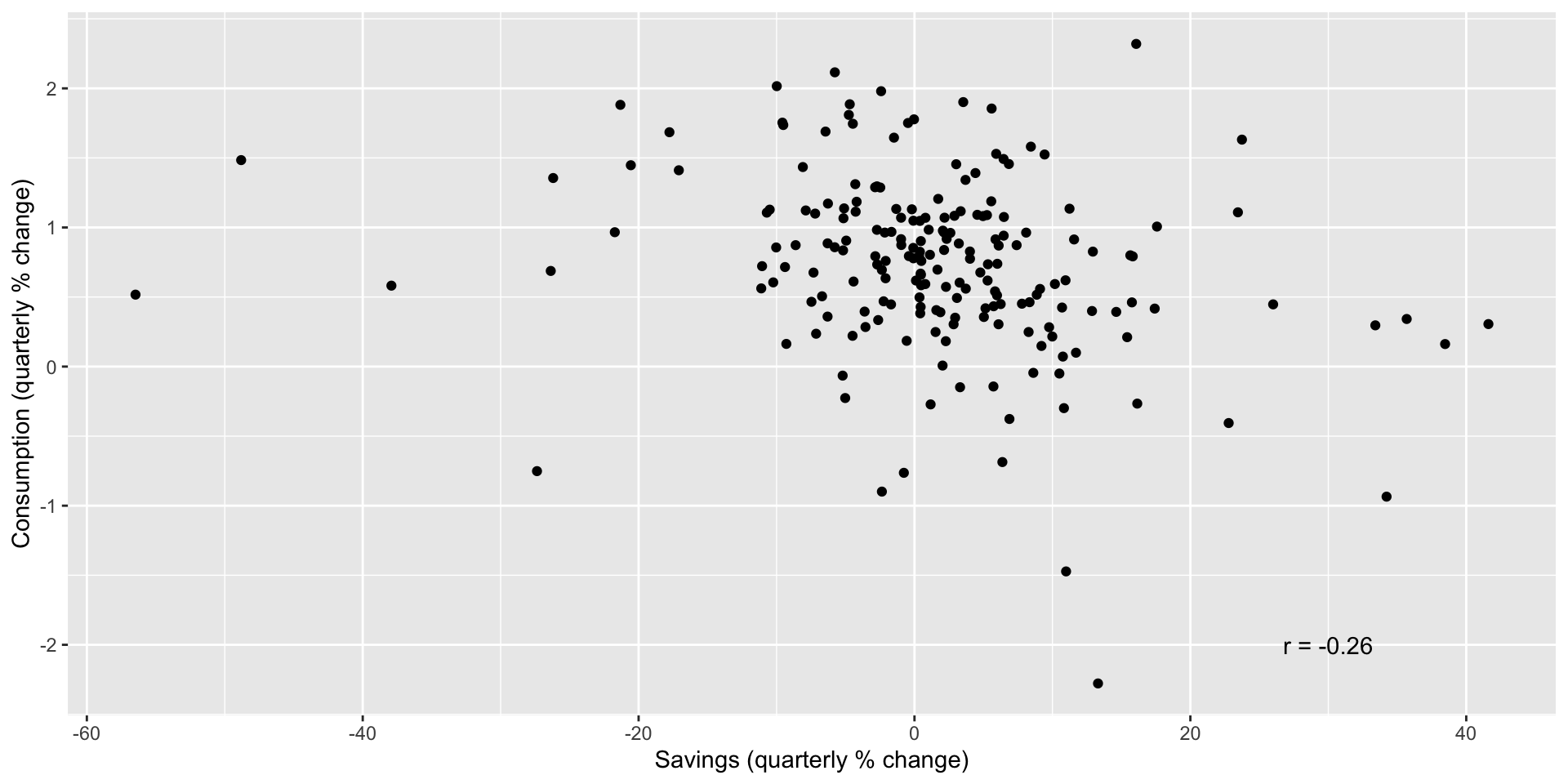

Multiple regression

- Pick a few variables in

us_changeto include in a multiple regression againstConsumption.

Consumption/production

Consumption/savings

Consumption/unemployment

Multiple regression model

mr_c <- us_change |>

model(TSLM(Consumption ~ Income + Production + Unemployment))

report(mr_c)Multiple regression results

Series: Consumption

Model: TSLM

Residuals:

Min 1Q Median 3Q Max

-1.5973206 -0.3317848 -0.0004972 0.2948522 1.6881414

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.55973 0.04915 11.389 < 2e-16 ***

Income 0.18044 0.04175 4.322 2.47e-05 ***

Production 0.10227 0.03756 2.722 0.00707 **

Unemployment -0.49026 0.15376 -3.188 0.00167 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.508 on 194 degrees of freedom

Multiple R-squared: 0.3755, Adjusted R-squared: 0.3658

F-statistic: 38.88 on 3 and 194 DF, p-value: < 2.22e-16Fitted values

- Estimating the regression allows us to obtain fitted (predicted) values for \(y\): \(\hat{y}_{t} = \hat{\beta}_{0} + \hat{\beta}_{1} x_{1,t} + \hat{\beta}_{2} x_{2,t} + ... + \hat{\beta}_{k} x_{k,t} + \epsilon_{t}\)

- Note these are predictions for the actual observed values, not forecasts.

Accessing fitted values

- With a

tslmobject, useaugment()to access fitted values:

augment(mr_c)# A tsibble: 198 x 6 [1Q]

# Key: .model [1]

.model Quarter Consumption .fitted .resid .innov

<chr> <qtr> <dbl> <dbl> <dbl> <dbl>

1 TSLM(Consumption ~ Income + Prod… 1970 Q1 0.619 0.0562 0.562 0.562

2 TSLM(Consumption ~ Income + Prod… 1970 Q2 0.452 0.479 -0.0274 -0.0274

3 TSLM(Consumption ~ Income + Prod… 1970 Q3 0.873 0.564 0.309 0.309

4 TSLM(Consumption ~ Income + Prod… 1970 Q4 -0.272 -0.0502 -0.222 -0.222

5 TSLM(Consumption ~ Income + Prod… 1971 Q1 1.90 1.16 0.741 0.741

6 TSLM(Consumption ~ Income + Prod… 1971 Q2 0.915 0.962 -0.0470 -0.0470

7 TSLM(Consumption ~ Income + Prod… 1971 Q3 0.794 0.636 0.158 0.158

8 TSLM(Consumption ~ Income + Prod… 1971 Q4 1.65 1.00 0.642 0.642

9 TSLM(Consumption ~ Income + Prod… 1972 Q1 1.31 1.17 0.146 0.146

10 TSLM(Consumption ~ Income + Prod… 1972 Q2 1.89 0.988 0.897 0.897

# ℹ 188 more rowsPlotting fitted values

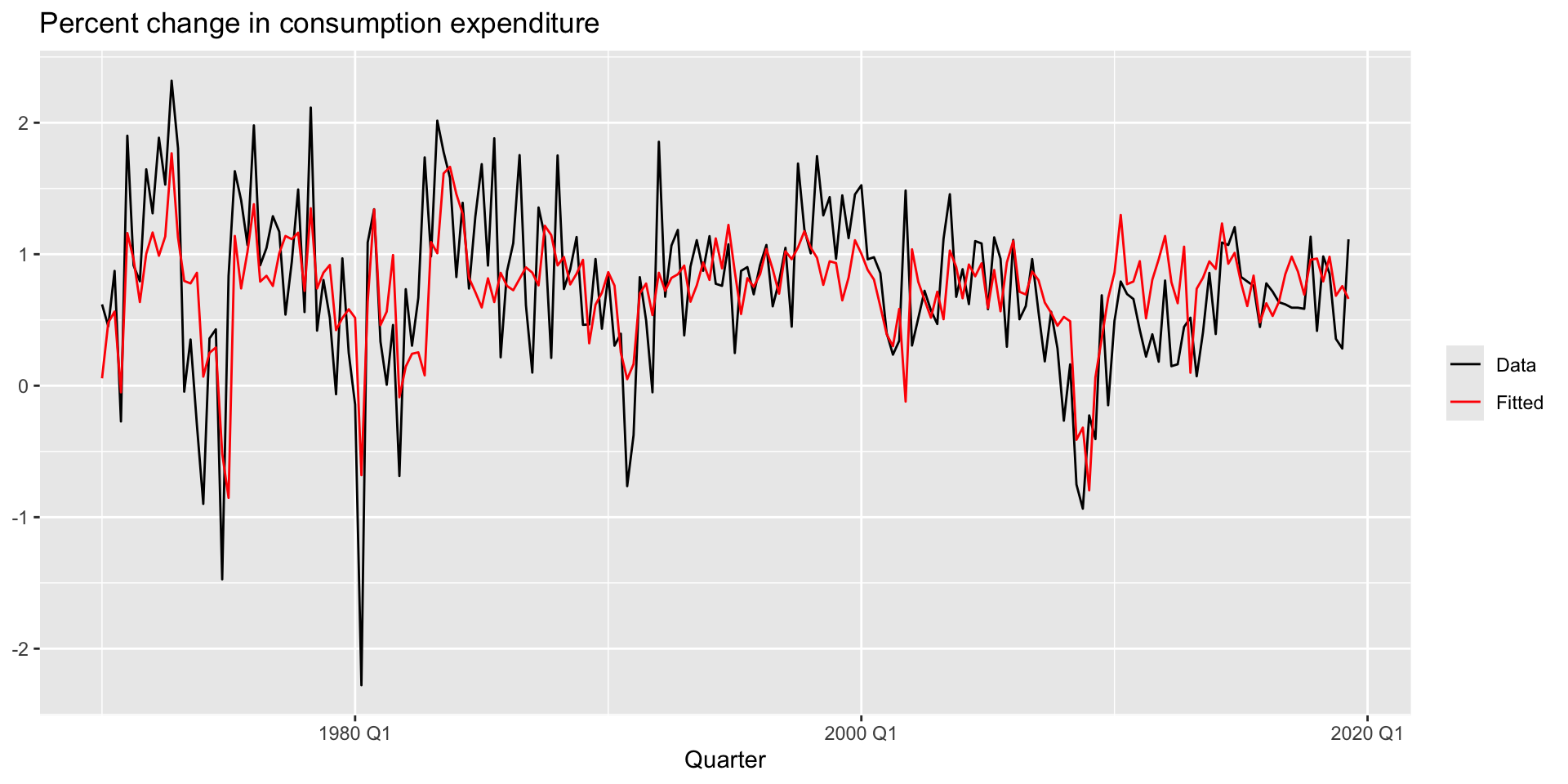

- Let’s see how well our predicted values line up with reality.

augment(mr_c) |>

ggplot(aes(x = Quarter)) +

geom_line(aes(y = Consumption, colour = "Data")) +

geom_line(aes(y = .fitted, colour = "Fitted")) +

labs(y = NULL,

title = "Percent change in consumption expenditure") +

scale_colour_manual(values=c(Data="black",Fitted="red")) +

guides(colour = guide_legend(title = NULL))Plotting fitted values

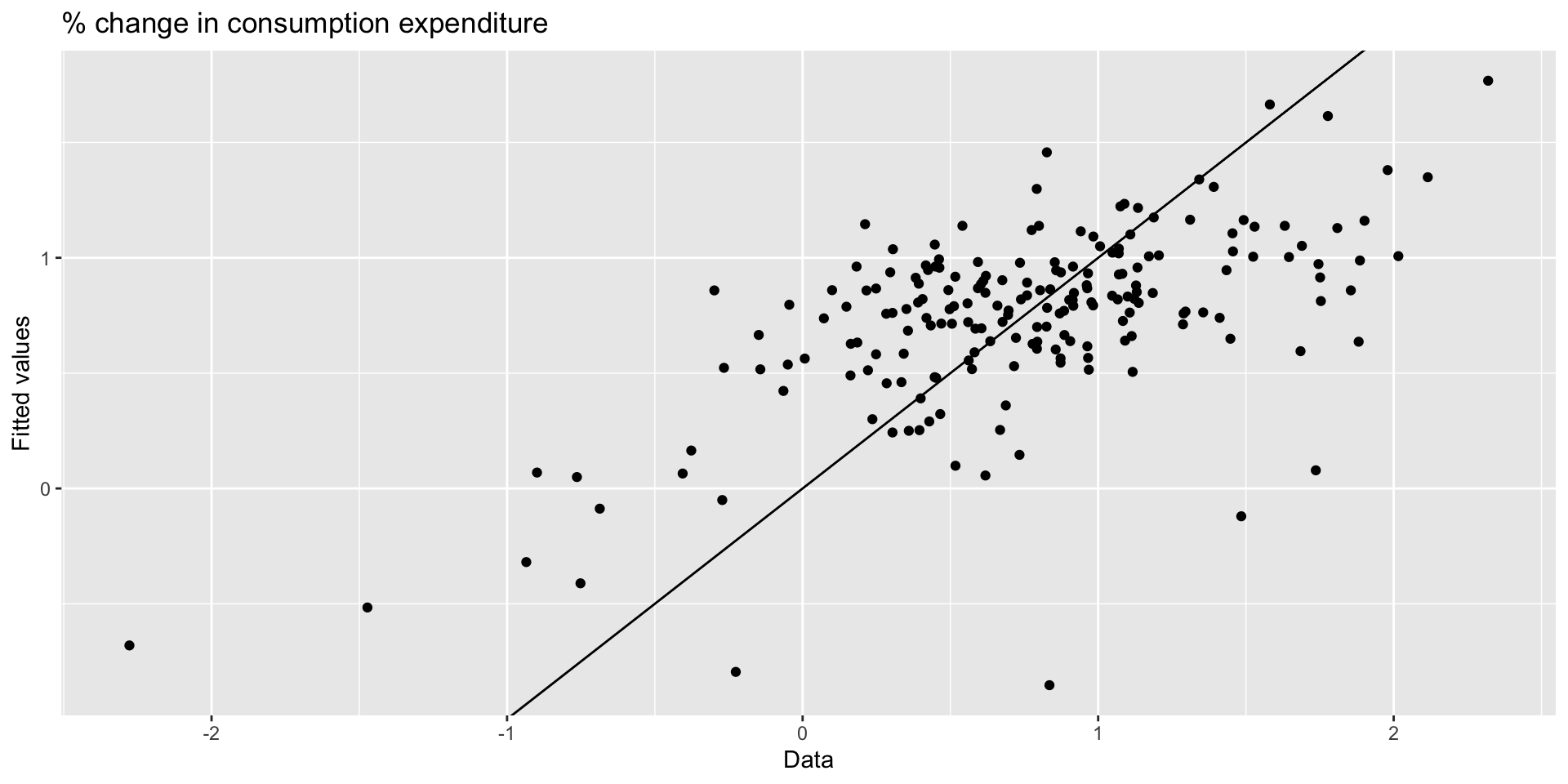

Plotting fitted values: scatter

- We could scatter \(y\) against \(\hat{y}\):

augment(mr_c) |>

ggplot(aes(x = Consumption, y = .fitted)) +

geom_point() +

labs(x = "Data",

y = "Fitted values",

title = "% change in consumption expenditure") +

geom_abline(intercept = 0, slope = 1)Plotting fitted values: scatter

Goodness-of-fit

- The coefficient of determination, \(R^{2}\) is a good summary measure of how well your model fits the data:

\(R^{2} = \frac{\sum(\hat{y}_{t} - \bar{y})^{2}}{\sum(y_{t} - \bar{y})^{2}}\)

- It gives the proportion of variation in \(y\) explained by \(\hat{y}\).

- Note \(R^{2}\) never decreases when adding predictors. Not necessarily a good metric for evaluating a forecast model.

- \(R^{2}\) of above model is 0.3755.