More time series graphics

BUS 323 Forecasting and Risk Analysis

Seasonal plots

- Seasonal plots disaggregate a time series into “seasons”.

- I’m going to work with the antidiabetic drug sales object we made last time to start:

library(fpp3)

a10 <- PBS |>

filter(ATC2 == "A10") |>

select(Month, Concession, Type, Cost) |>

summarise(TotalC = sum(Cost)) |>

mutate(Cost = TotalC/1e6)

Seasonal plots

- To make a seasonal plot, use

gg_season()

- e.g.

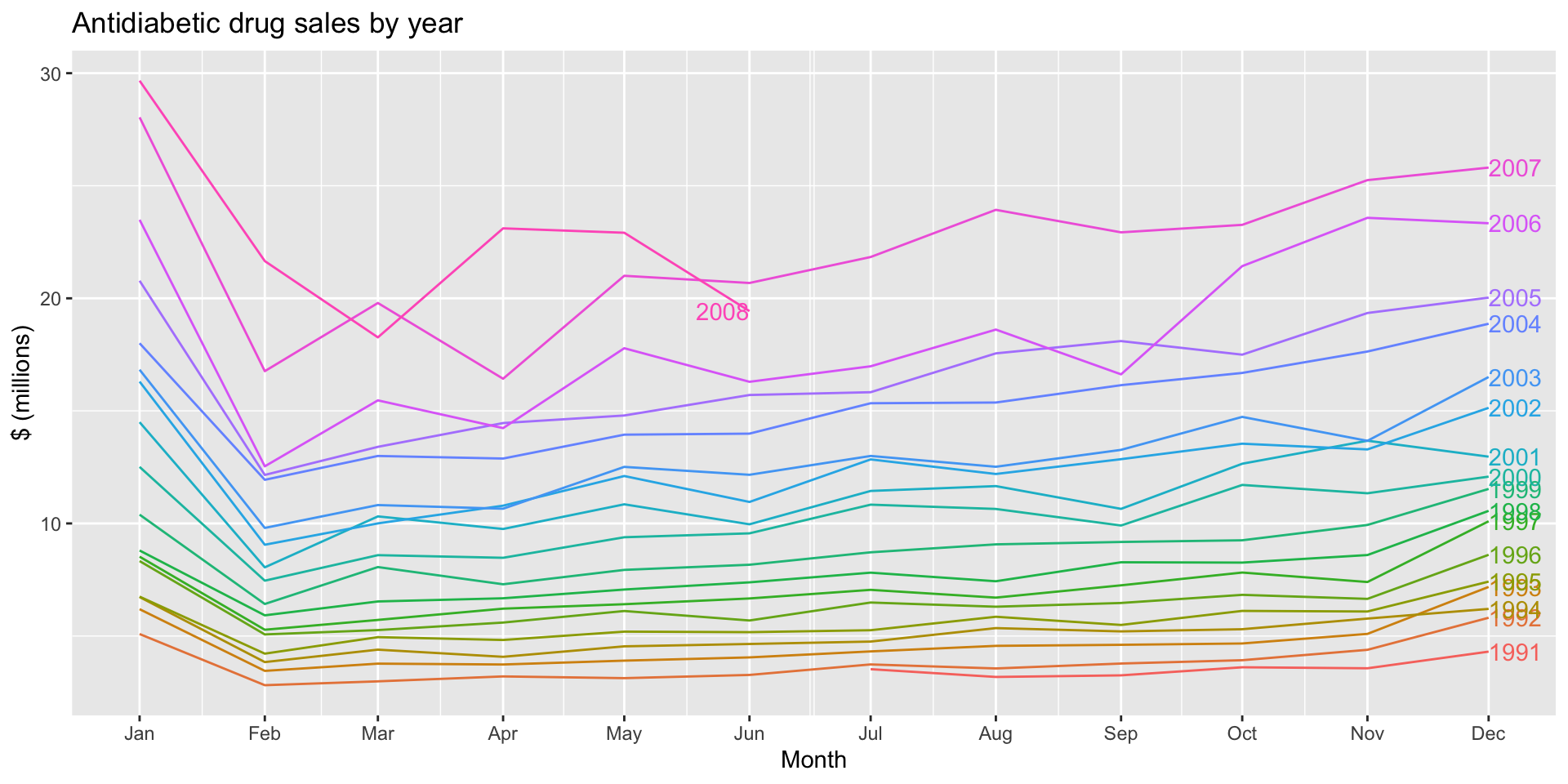

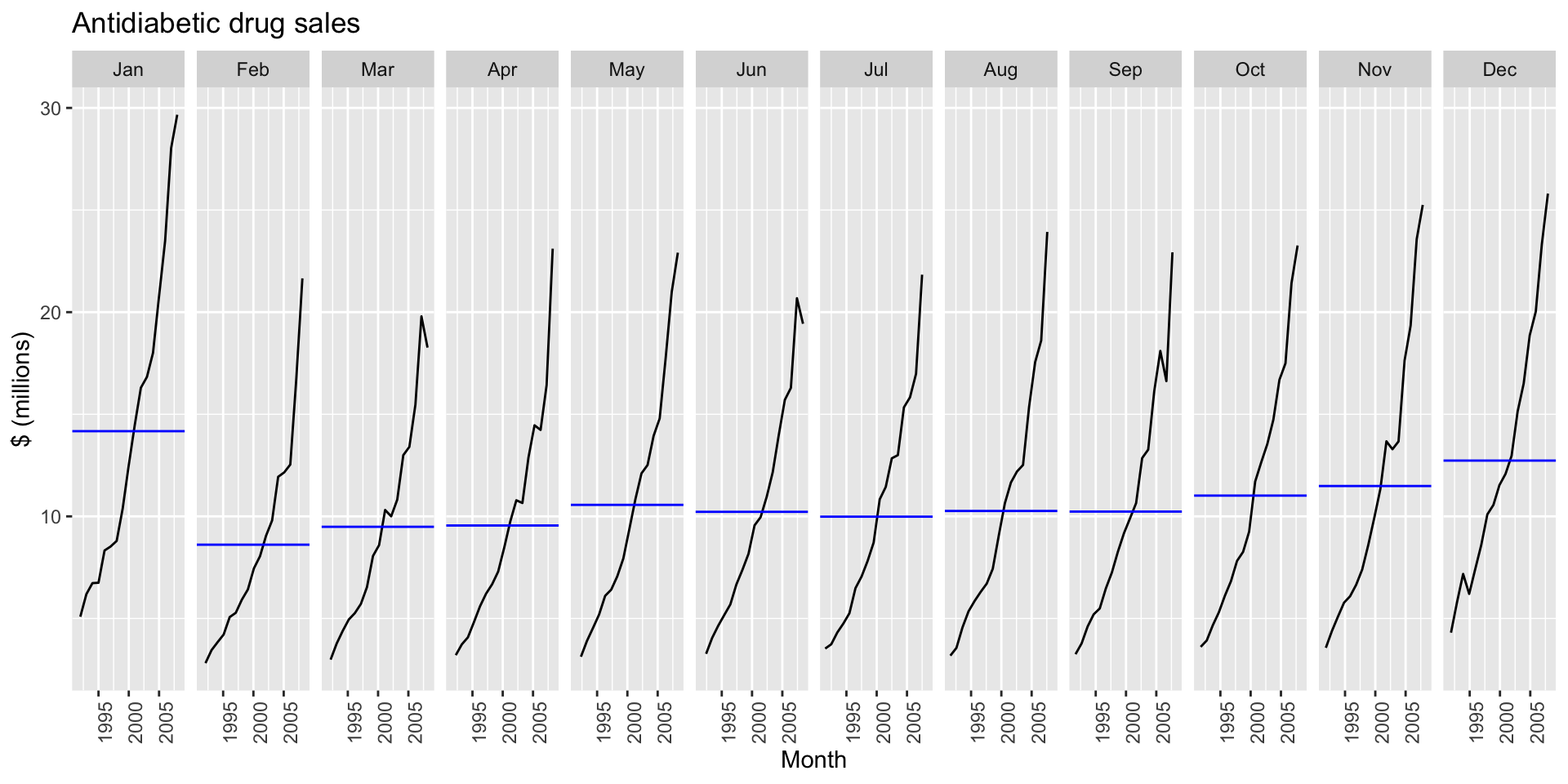

a10 |>

gg_season(Cost, labels="right") +

labs(y = "$ (millions)",

title = "Antidiabetic drug sales by year")

![]()

Seasonal plots

?gg_season()gg_season will assume you want to disaggregate by the largest frequency in the tsibble by default.

Seasonal plots

- If your time series has multiple periods, you can specify which seasonal plot you want using the

period argument.

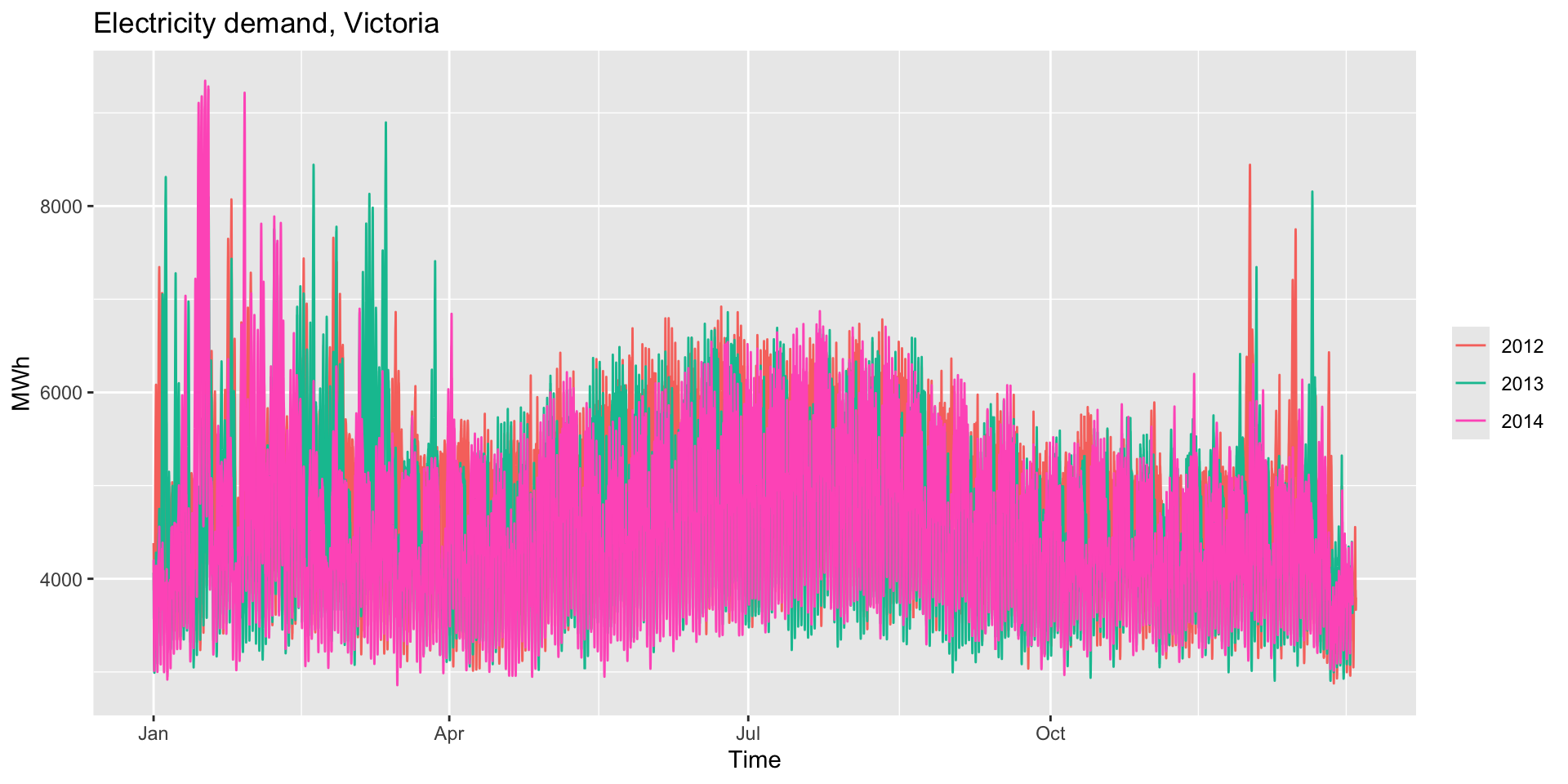

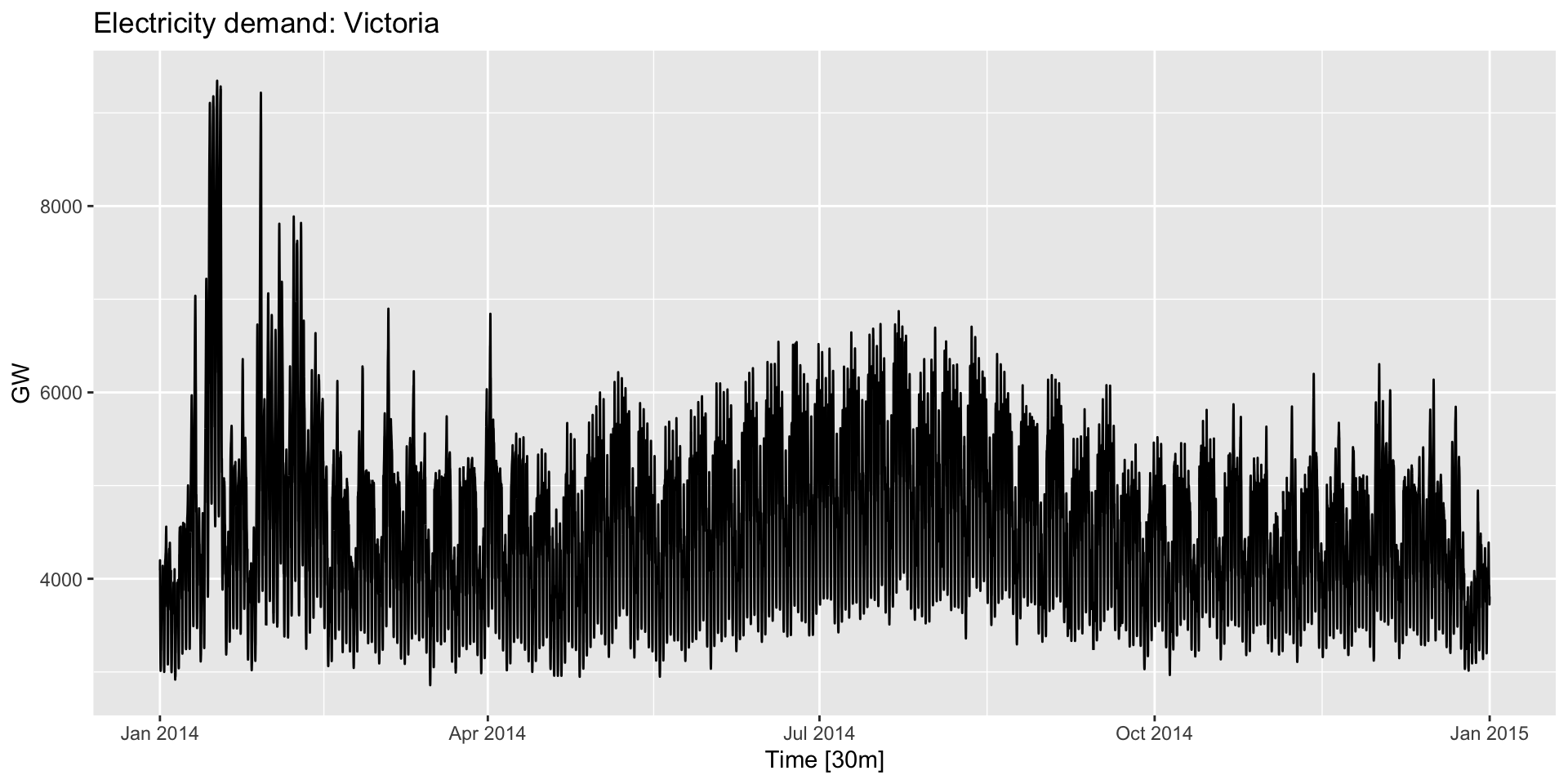

vic_elec has half-hourly observations of electricity demand in Victoria. What does gg_season plot by default?

vic_elec |>

gg_season(Demand) +

labs(y="MWh", title="Electricity demand, Victoria")

![]()

Seasonal plots

- Try

head(vic_elec) to get a sense of the format of the time variable.

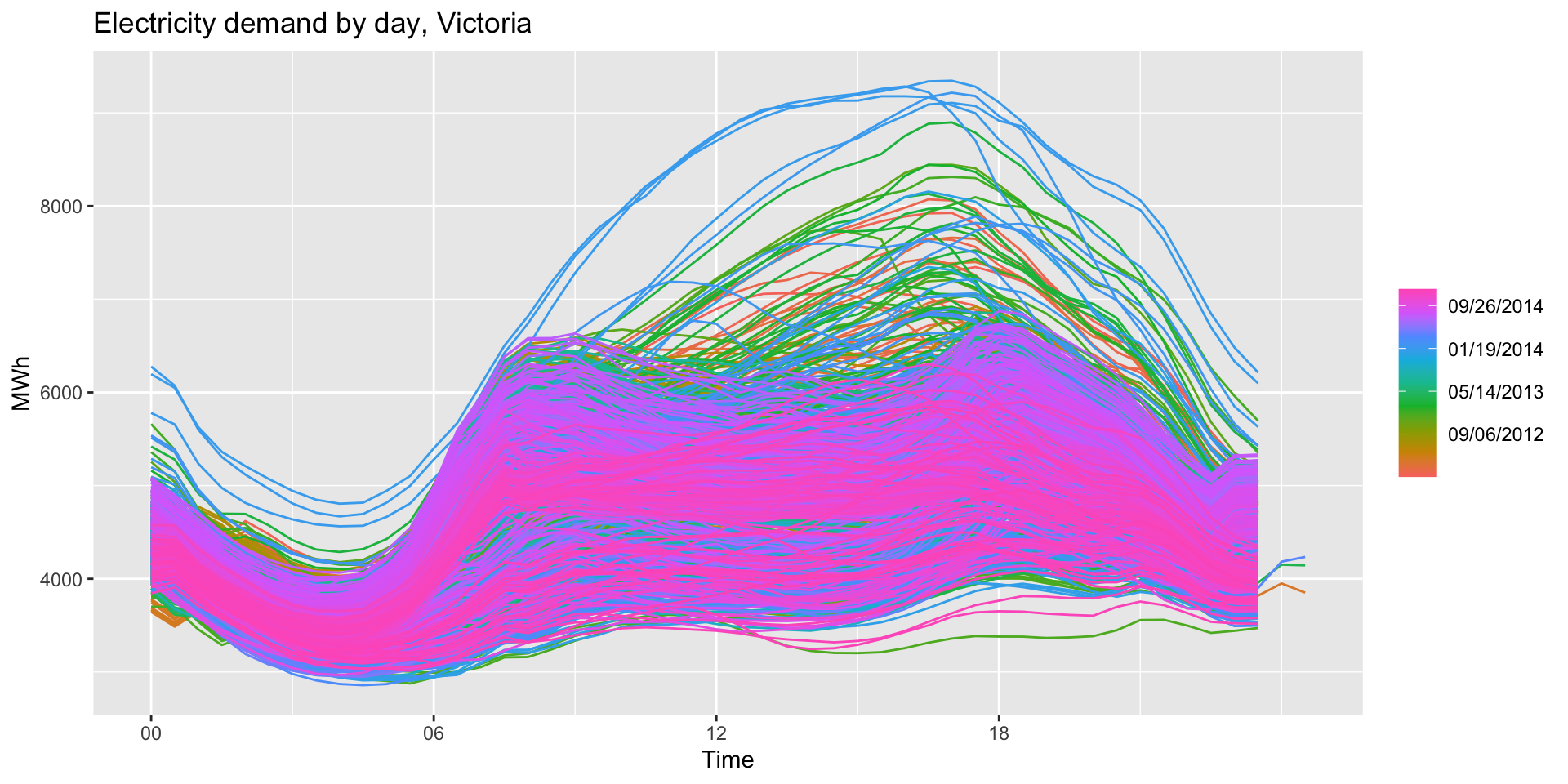

- Use the

period argument to produce a daily seasonal time plot:

vic_elec |>

gg_season(Demand, period="day") +

labs(y="MWh", title="Electricity demand by day, Victoria")

![]()

Seasonal plots

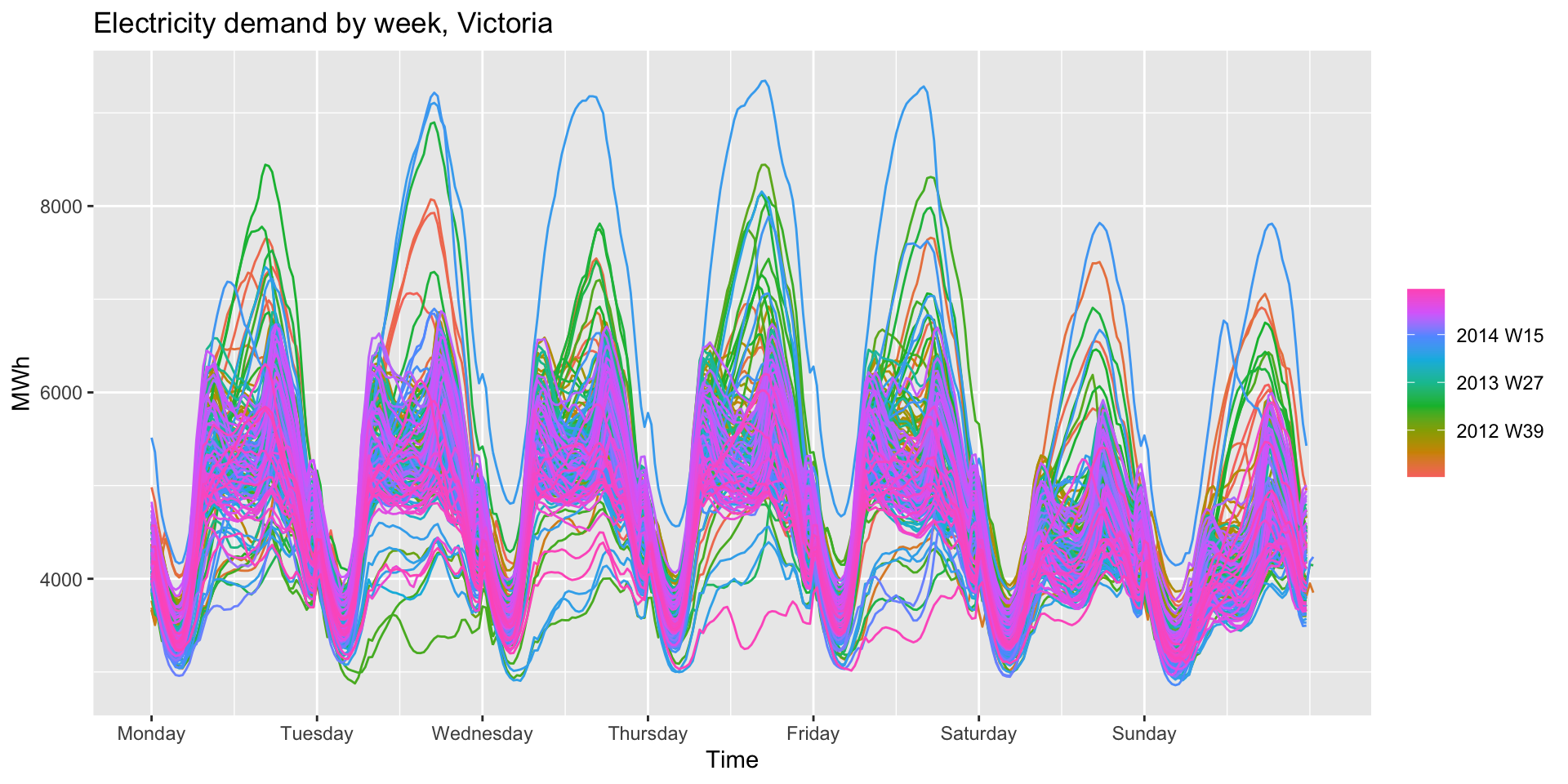

vic_elec |>

gg_season(Demand, period="week") +

labs(y="MWh", title="Electricity demand by week, Victoria")

![]()

Seasonal subseries plots

gg_subseries()- Plots a time series by each season within a seasonal period.

- e.g., using the antidiabetic drug sales dataset:

a10 |>

gg_subseries(Cost) +

labs(

y = "$ (millions)",

title = "Antidiabetic drug sales"

)

Seasonal subseries plots

![]()

Exercise: holiday tourism

holidays <- tourism |>

filter(Purpose == "Holiday") |>

group_by(State) |>

summarise(Trips = sum(Trips))

# A tsibble: 640 x 3 [1Q]

# Key: State [8]

State Quarter Trips

<chr> <qtr> <dbl>

1 ACT 1998 Q1 196.

2 ACT 1998 Q2 127.

3 ACT 1998 Q3 111.

4 ACT 1998 Q4 170.

5 ACT 1999 Q1 108.

6 ACT 1999 Q2 125.

7 ACT 1999 Q3 178.

8 ACT 1999 Q4 218.

9 ACT 2000 Q1 158.

10 ACT 2000 Q2 155.

# ℹ 630 more rows

Exercise: holiday tourism autoplot

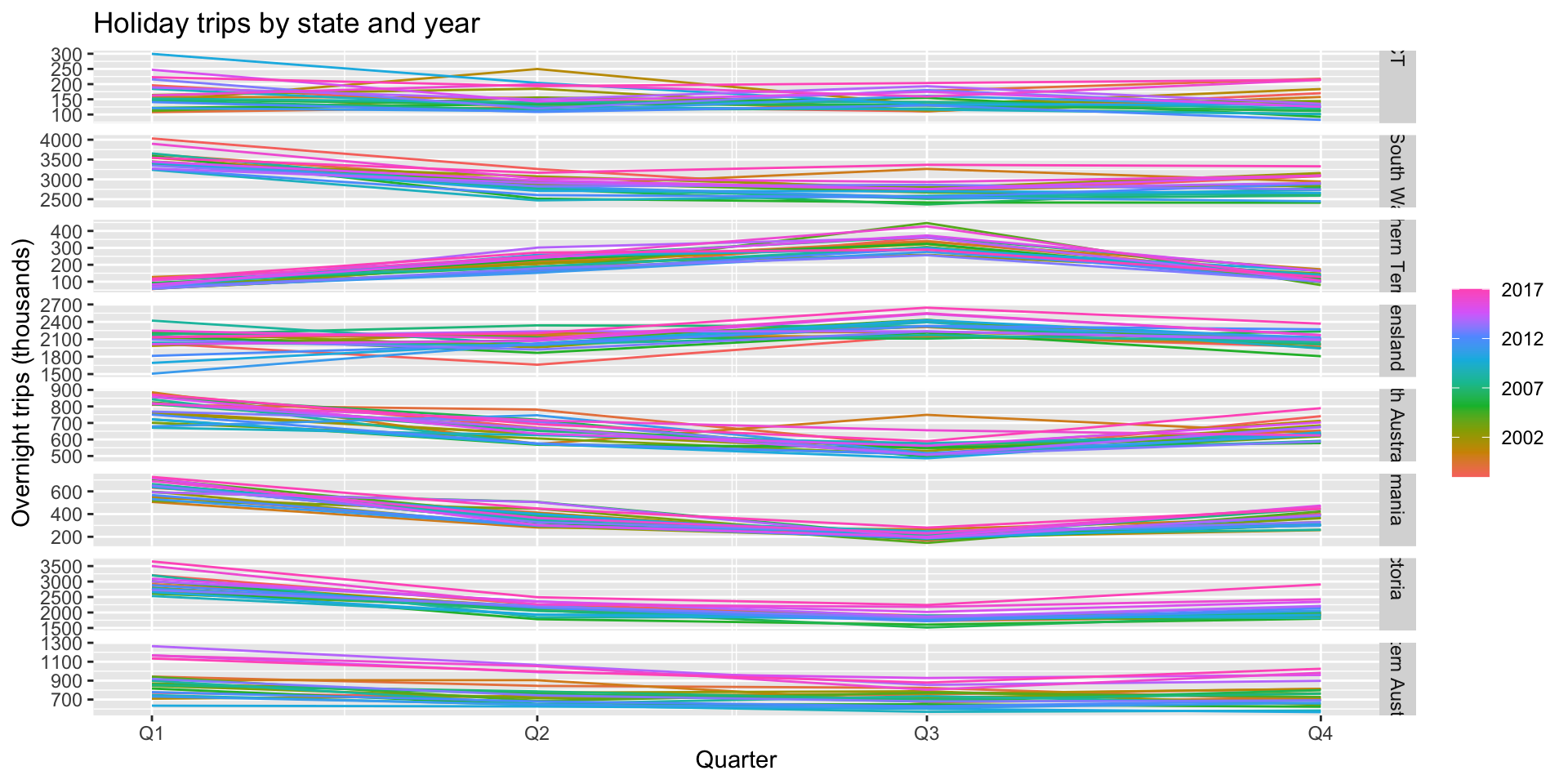

autoplot(holidays, Trips) +

labs(y = "Overnight trips (thousands)",

title = "Holiday trips by state")

![]()

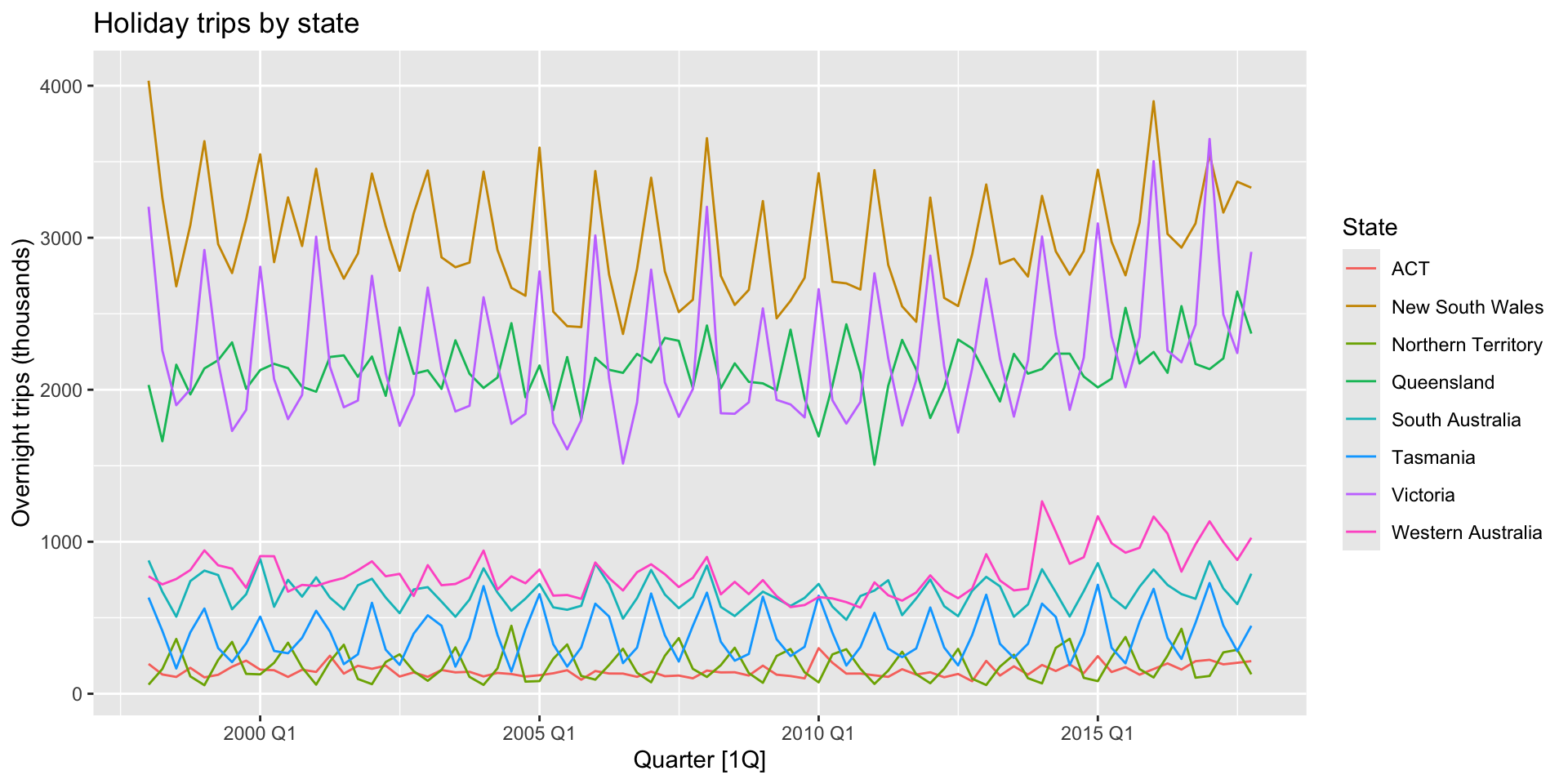

Exercise: holiday tourism seasonal plot

gg_season(holidays, Trips) +

labs(y = "Overnight trips (thousands)",

title = "Holiday trips by state and year")

![]()

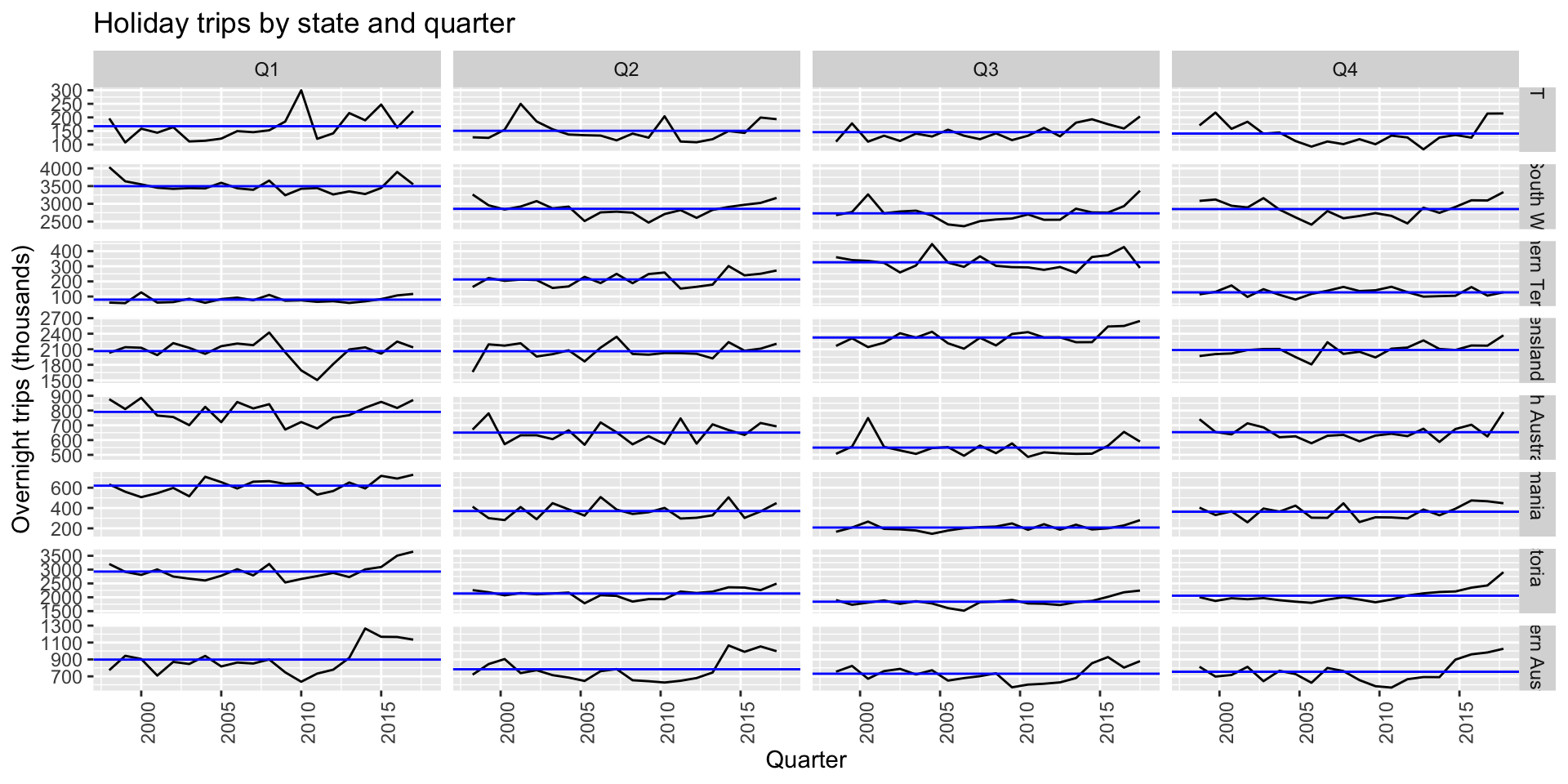

Exercise: holiday tourism subseries plots

gg_subseries(holidays, Trips) +

labs(y = "Overnight trips (thousands)",

title = "Holiday trips by state and quarter")

![]()

Scatterplots

- Useful for visualizing relationships between variables.

Scatterplots

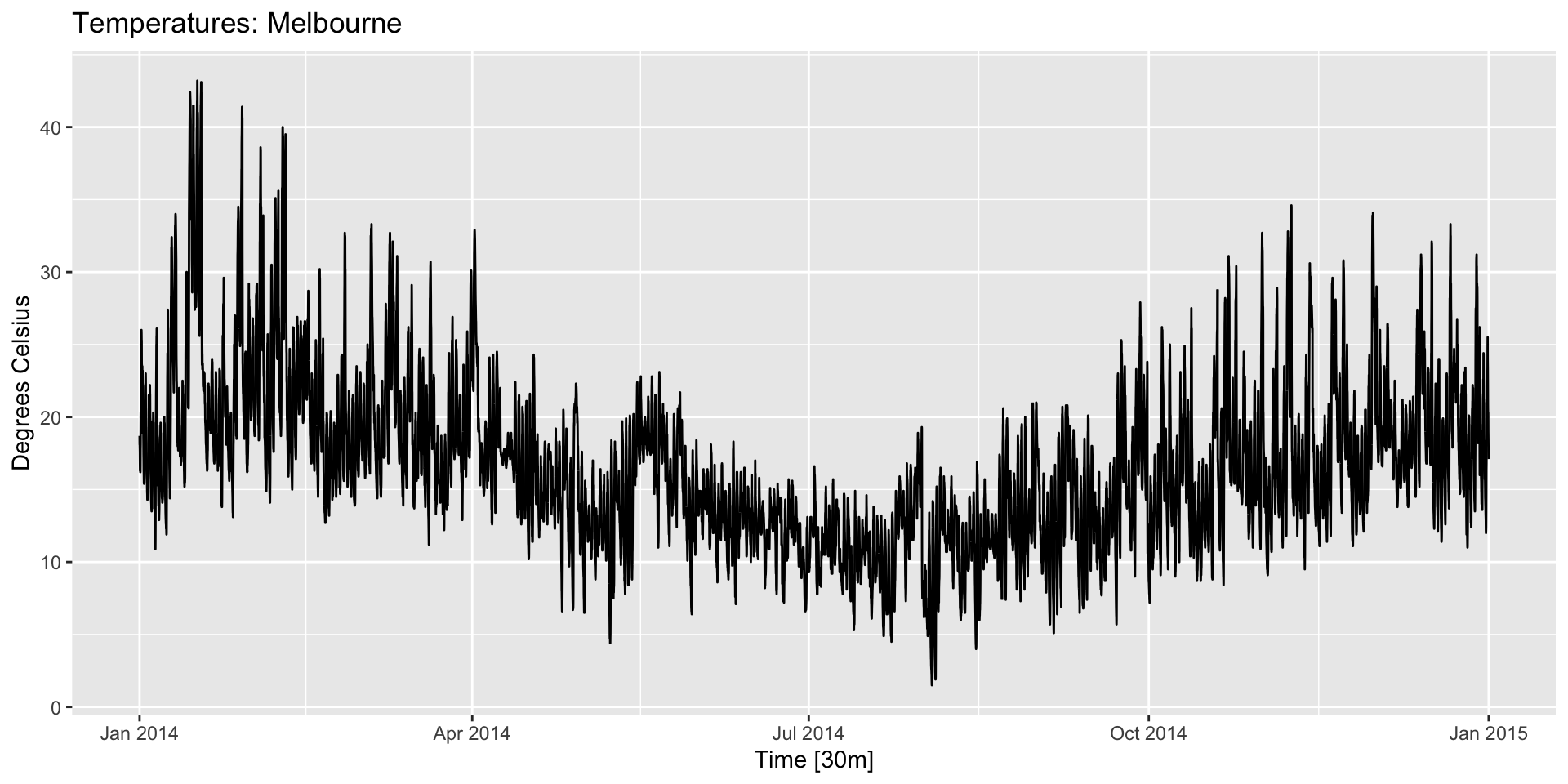

- Suppose we think electricity demand and temperature are related. Here’s demand:

![]()

Scatterplots

![]()

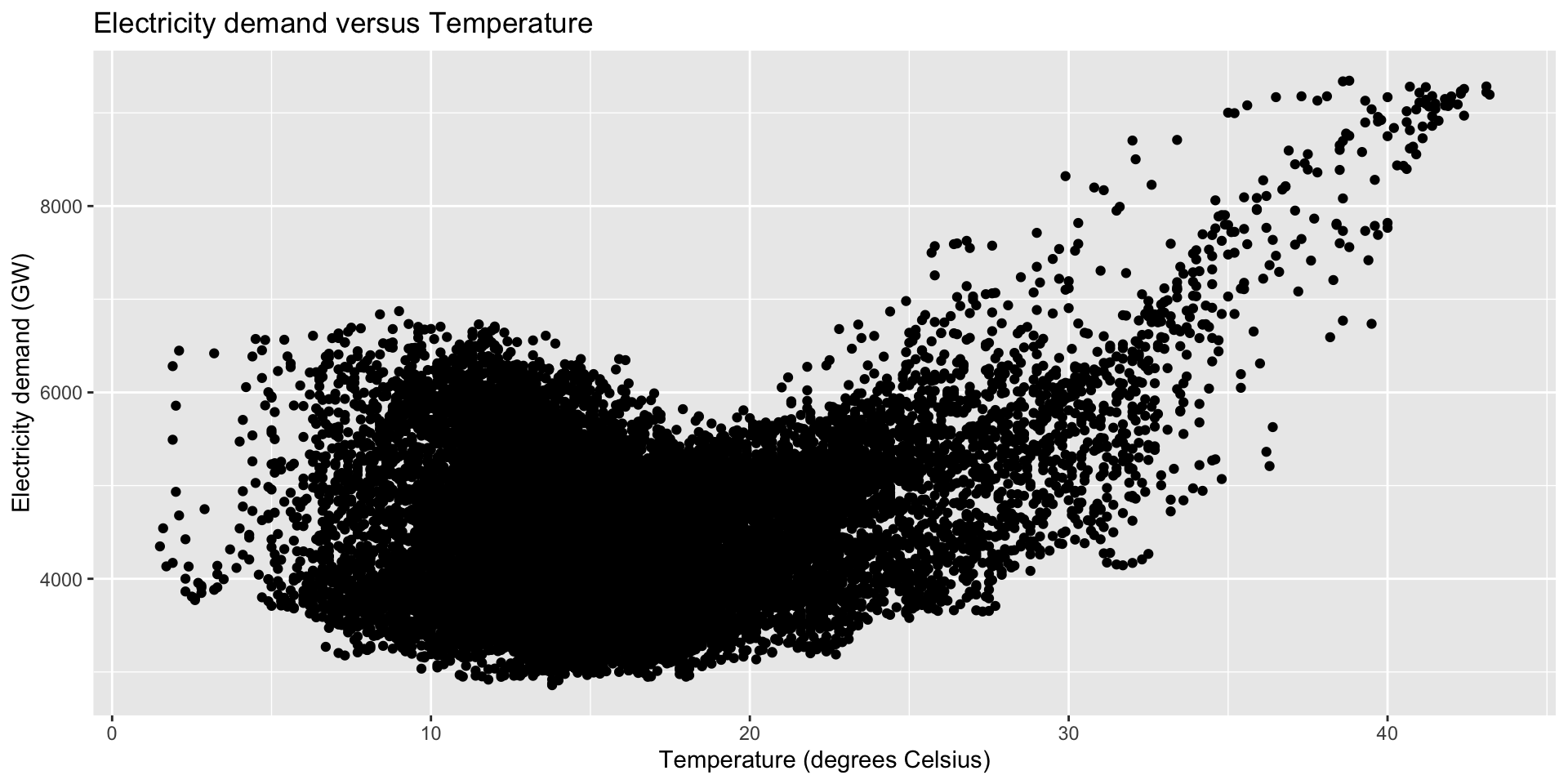

Scaterplots

vic_elec |>

filter(year(Time) == 2014) |>

ggplot(aes(x = Temperature, y = Demand)) +

geom_point() +

labs(title="Electricity demand and temperature",

x = "Temperature (Celsius)",

y = "Electricity demand (GW)")

![]()

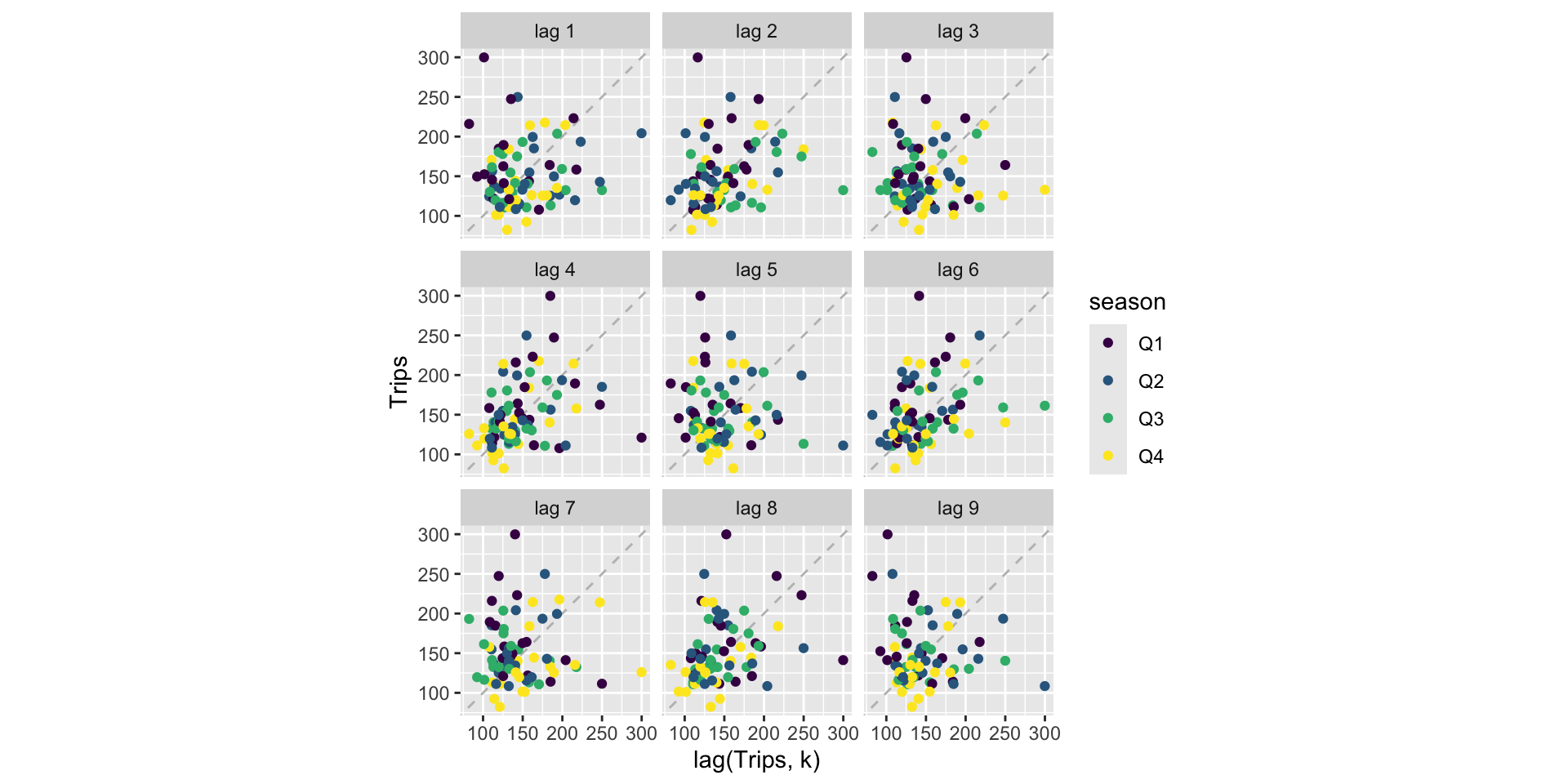

Lag plots

- Lagged values (\(y_{t-k}\)) are often useful predictors in forecasting.

- We can use

gg_lag() to get a quick sense of which might be important.

holidays |>

filter(State == "ACT") |>

gg_lag(Trips, geom = "point") +

labs(x = "lag(Trips, k)")

Lag plots

![]()

Lag plots

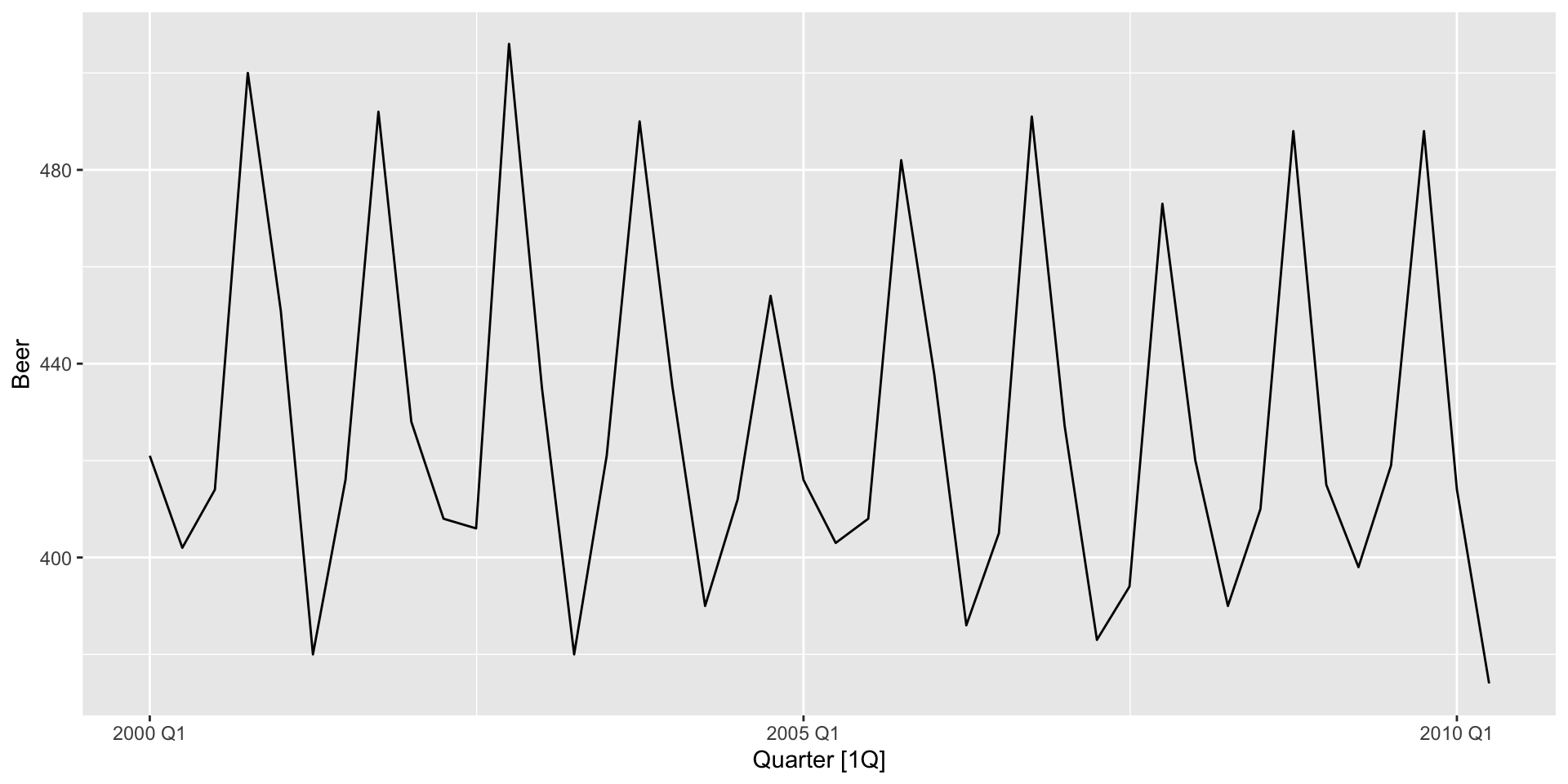

- Not much there. Let’s try another series:

recent_production <- aus_production |>

filter(year(Quarter) >= 2000)

autoplot(recent_production, Beer)

![]()

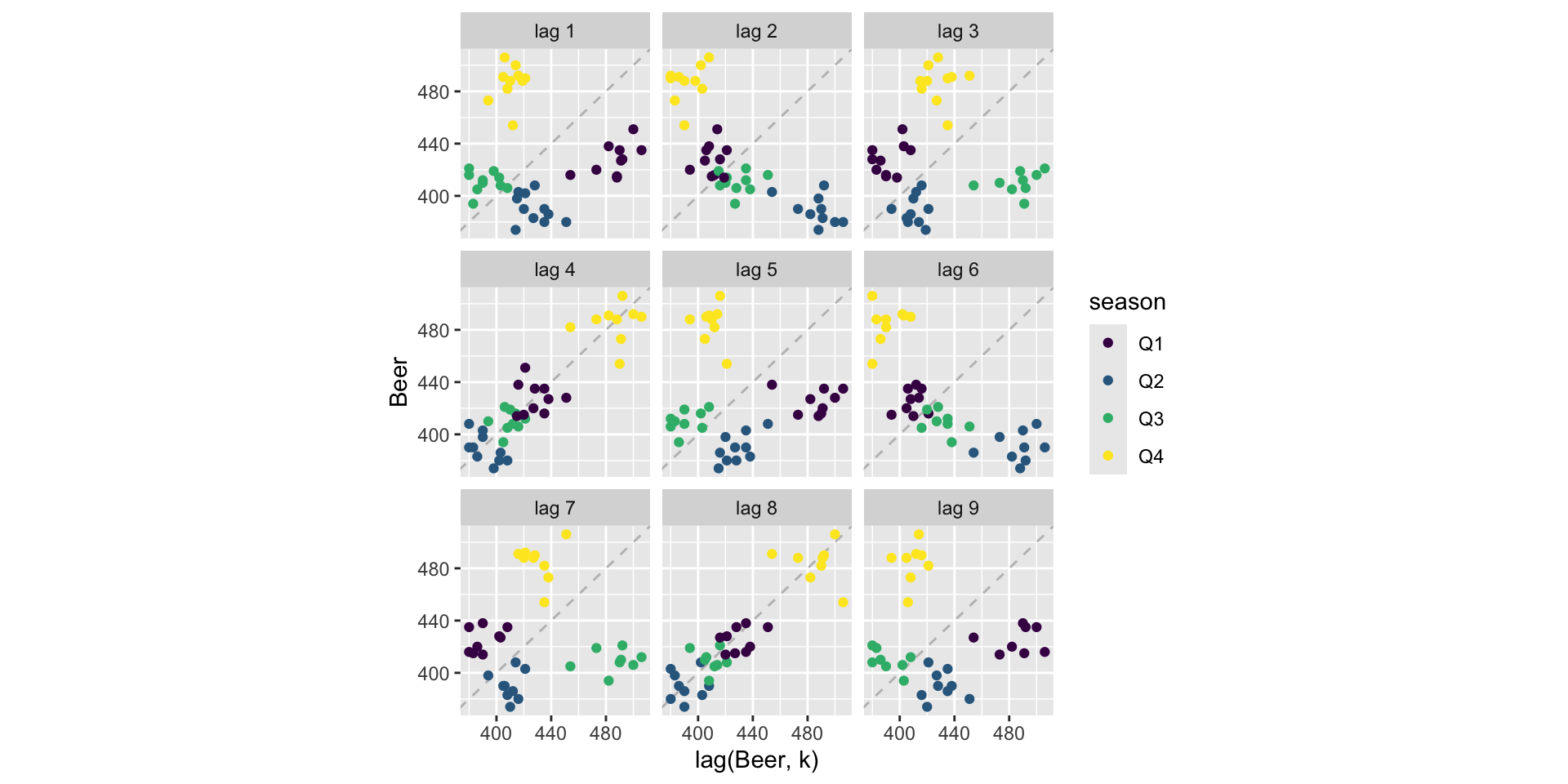

Lag plots

- There’s clear seasonality across years here. Let’s see what the lag plots say:

recent_production |>

gg_lag(Beer, geom = "point") +

labs(x = "lag(Beer, k)")

Lag plots

![]()

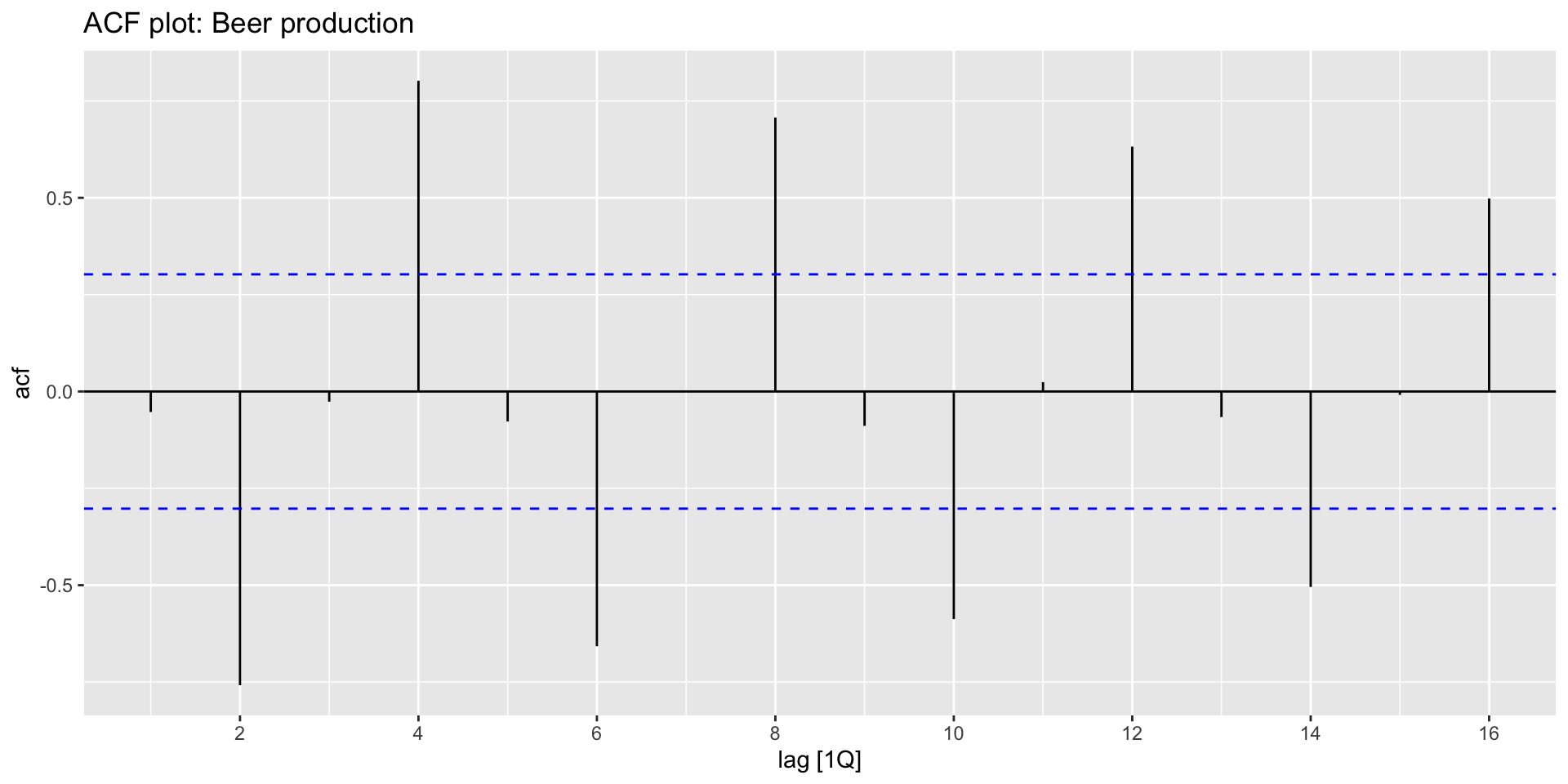

Autocorrelation and the ACF

ACF() calculates \(r_{k}\) for all \(k\) as specified by the lag_max option:

recent_production |>

ACF(Beer, lag_max = 9)

# A tsibble: 9 x 2 [1Q]

lag acf

<cf_lag> <dbl>

1 1Q -0.0530

2 2Q -0.758

3 3Q -0.0262

4 4Q 0.802

5 5Q -0.0775

6 6Q -0.657

7 7Q 0.00119

8 8Q 0.707

9 9Q -0.0888

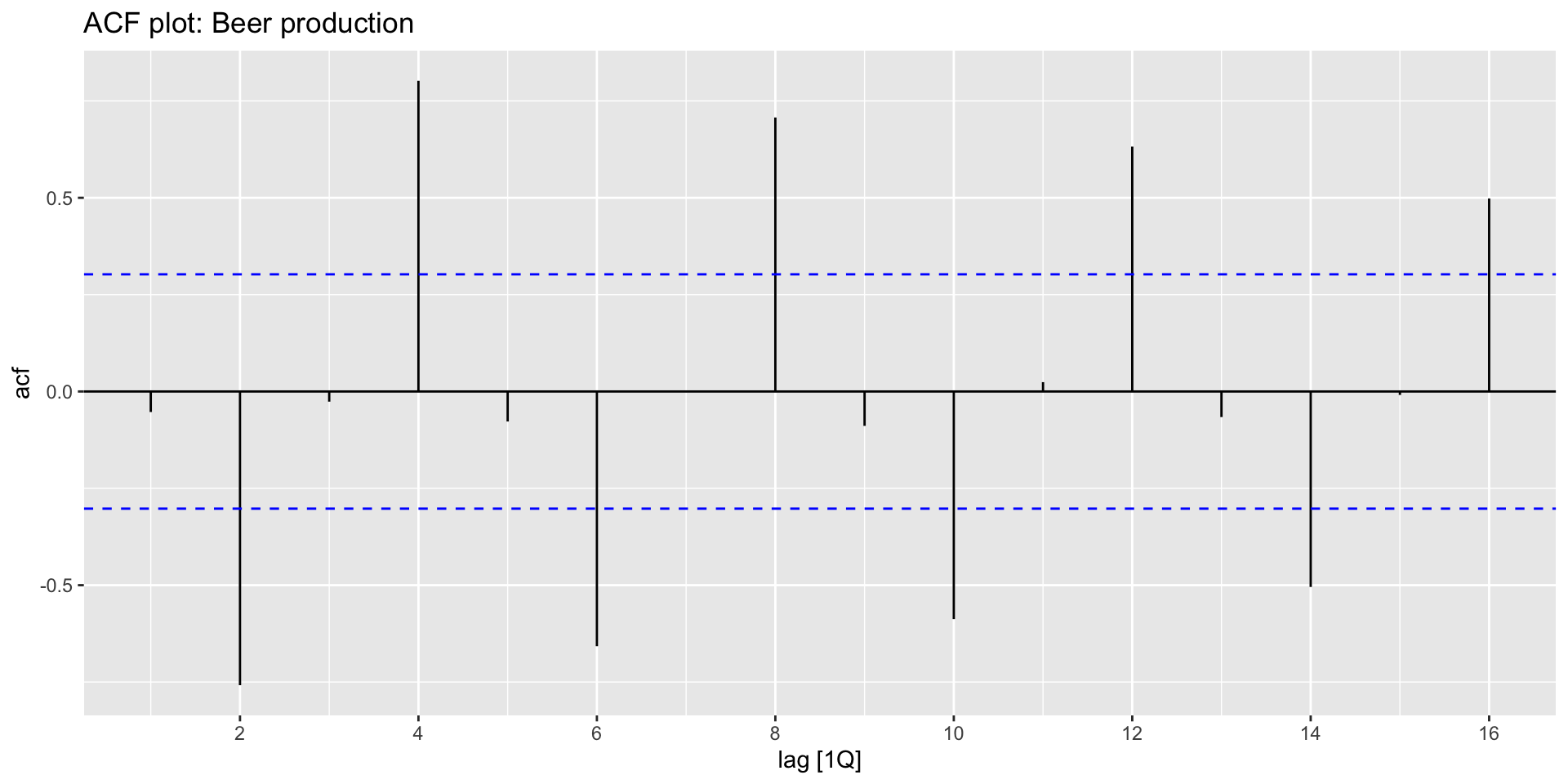

ACF plots

- We can plot the autocorrelation coefficients easily with

autoplot():

recent_production |>

ACF(Beer) |>

autoplot() +

labs(title = "ACF plot: Beer production")

![]()

ACF plots in the presence of trend

- When there is a trend, small lags tend to have high \(r_{k}\) and large lags tend to have small \(r_{k}\):

![]()

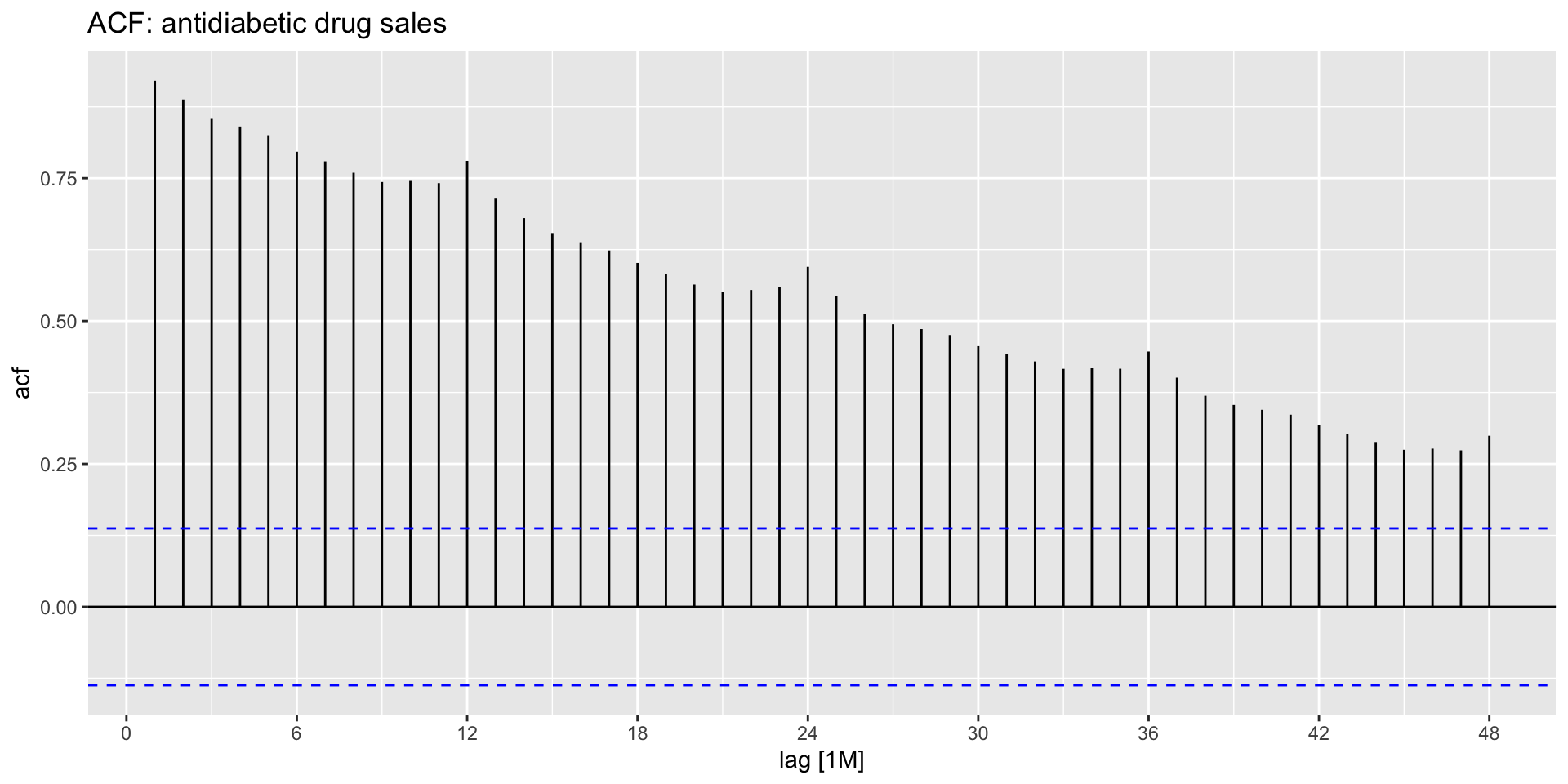

ACF plots in the presence of seasonality

- When there is seasonality, \(r_{k}\) tend to be relatively large for the seasonal lags:

![]()

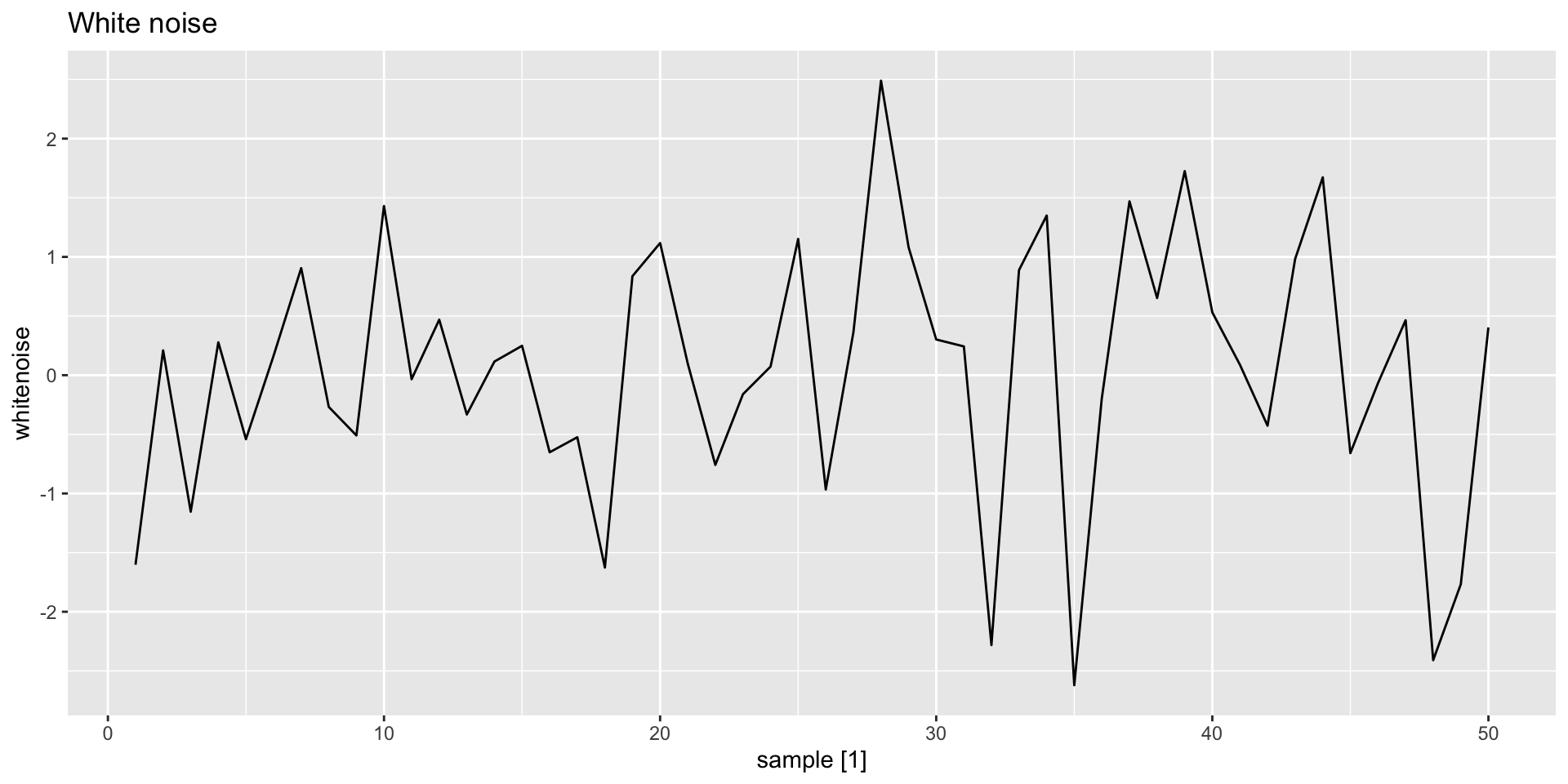

White noise

- Time series with no or little autocorrelation are called white noise:

y <- tsibble(sample = 1:50, whitenoise = rnorm(50), index = sample)

y |>

autoplot(whitenoise) +

labs(title = "White noise")

![]()

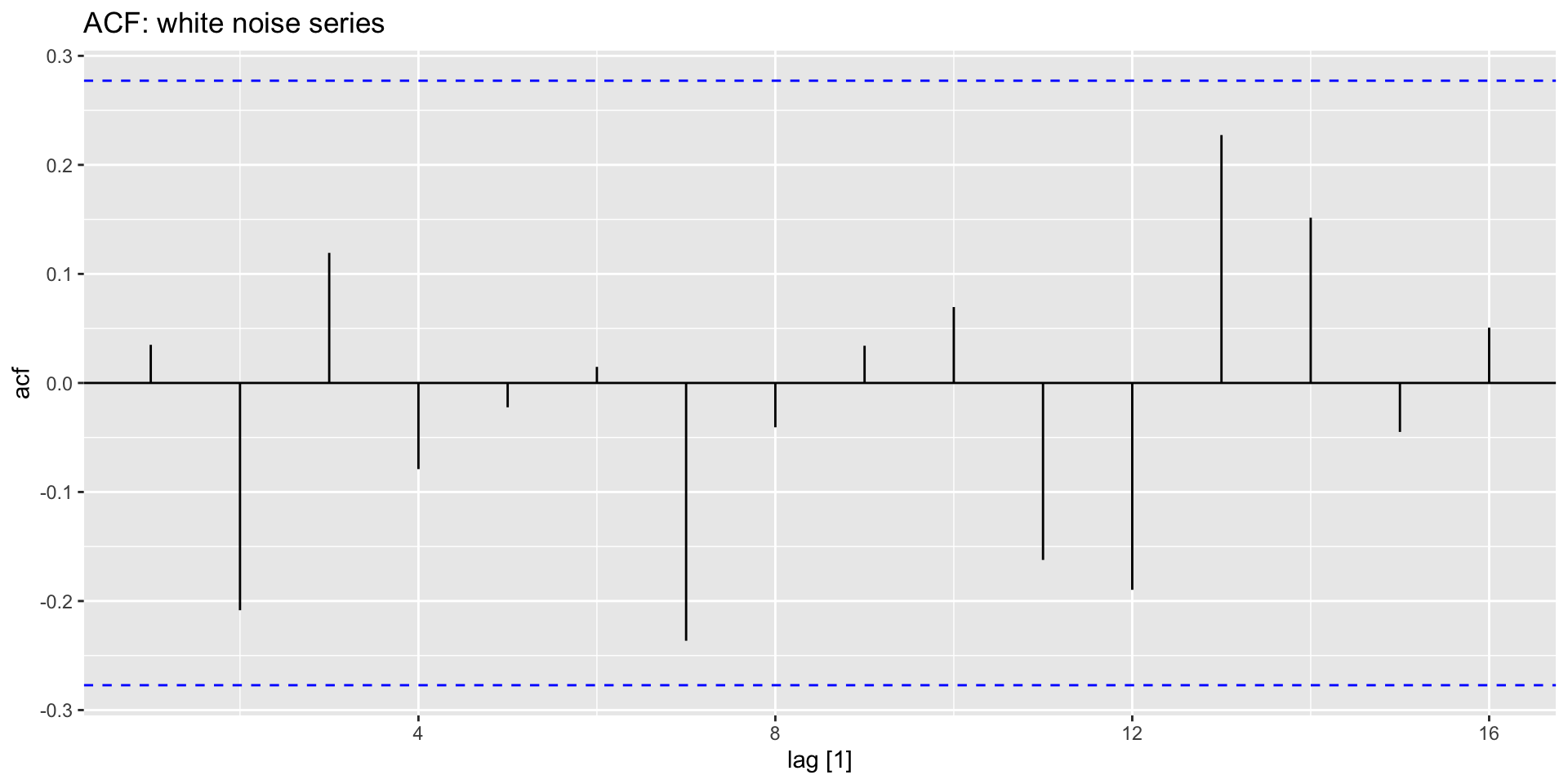

White noise ACF

- The ACF plot for a white noise series should show \(r_{k}\) of zero on average:

y |>

ACF(whitenoise) |>

autoplot() +

labs(title = "ACF: white noise series")

![]()

White noise ACF

- 95% of \(r_{k}\) should lie within \(\pm \frac{1.96}{\sqrt{T}}\).

- These bounds are shown in blue below.

- Here \(T=50\), so the bounds are at \(\pm \frac{1.96}{\sqrt{50}} = \pm 0.28\). If more then 5% of the “spikes” extend beyond these bounds, it’s not a white noise series.

![]()