ARIMA II

Moving average models

- Uses past forecast errors:

\[ y_{t} = c + \epsilon_{t} + \theta_{1} \epsilon_{t-1} + \theta_{2} \epsilon_{t-2} + ... + \theta_{q} \epsilon_{t-q} \]

- Where \(\epsilon_{t}\) is white noise.

- The above is a MA(q) model.

Moving average models: simulation

- Suppose we have two models:

- MA(1): \(y_{t} = 20 + \epsilon_{t} + 0.8 \epsilon_{t-1}\).

- MA(2): \(y_{t} = \epsilon_{t} - \epsilon_{t-1} + 0.8 \epsilon_{t-2}\).

- Generate the MA process for each model based on the following observed values of \(\epsilon_{t}\):

| Period | \(\epsilon\) |

|---|---|

| 1 | 1.712. |

| 2. | -1.514. |

| 3. | 0.948. |

| 4. | -1.518. |

| 5. | -0.212. |

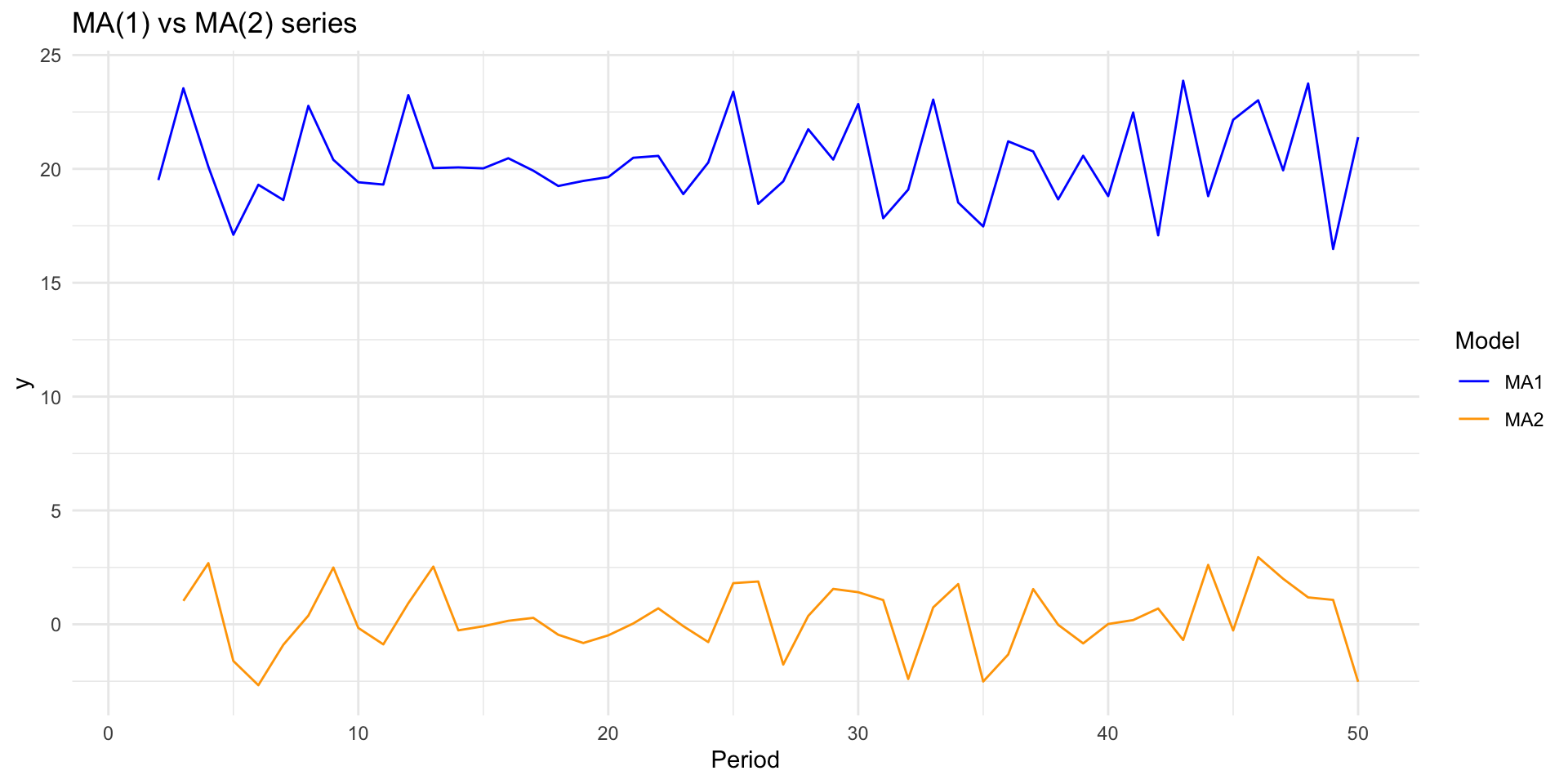

Moving average models: simulation II

- Suppose we have two models:

- MA(1): \(y_{t} = 20 + \epsilon_{t} + 0.8 \epsilon_{t-1}\).

- MA(2): \(y_{t} = \epsilon_{t} - \epsilon_{t-1} + 0.8 \epsilon_{t-2}\).

- Make a 50-observation vector containing white noise. Estimate both of the above MA models.

Moving average models: simulation II plot

- Plot the models:

Invertibility

- Any AR(p) model can be expressed as an MA(\(\infty\)) model.

- e.g. for an AR(1):

\[ \begin{align} y_{t} & = \phi_{1} y_{t-1} + \epsilon_{t} \\ & = \phi_{1}(\phi_{1} y_{t-2} + \epsilon_{t-1}) + \epsilon_{t-1} \\ & = \phi_{1}^{2} y_{t-2} + \phi_{1} \epsilon_{t-1}+ \epsilon_{t} \\ & = \phi_{1}^{2}(\phi_{1} y_{t-3} + \epsilon_{t-2}) + \phi_{1} \epsilon_{t-1} + \epsilon_{t} \\ & = \phi_{1}^{3} y_{t-3} + \phi_{1}^{2} \epsilon_{t-2} + \phi_{1} \epsilon_{t-1} + \epsilon_{t} \\ \textrm{etc.} \end{align} \]

- For \(-1 < \phi_{1} < 1\), \(\phi_{1}^{k}\) decreasing with \(k\).

- In the limit,

\[ y_{t} = \epsilon_{t} + \phi_{1} \epsilon_{t-1} + \phi_{1}^{2} \epsilon_{t-2} + \phi_{1}^{3} \epsilon_{t-3} + ... \]

- An MA(\(\infty\)) process.

- In the limit,

ARIMA models

- Combine differencing, autoregression, and moving average models:

\[ \begin{align} y_{t}' = & c + \phi y_{t-1}' + ... + \phi_{p} y_{t-p}' \\ & + \theta_{1} \epsilon_{t-1} + ... + \theta_{1} \epsilon_{t-q} + \epsilon_{t} \end{align} \]

- The above is an ARIMA(p,d,q) model

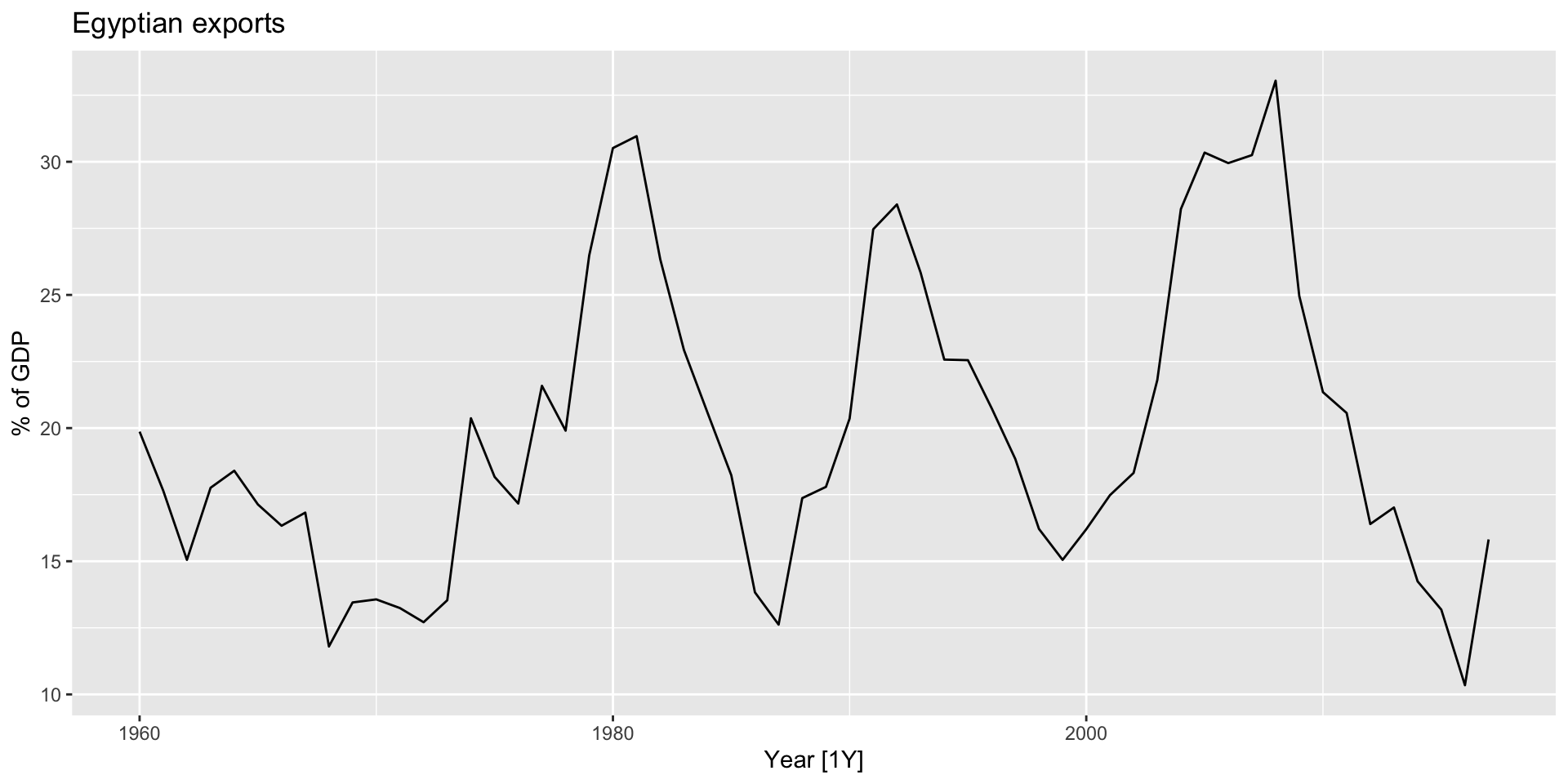

Example: Egyptian exports

- From

global_economy:

Example: Egyptian exports

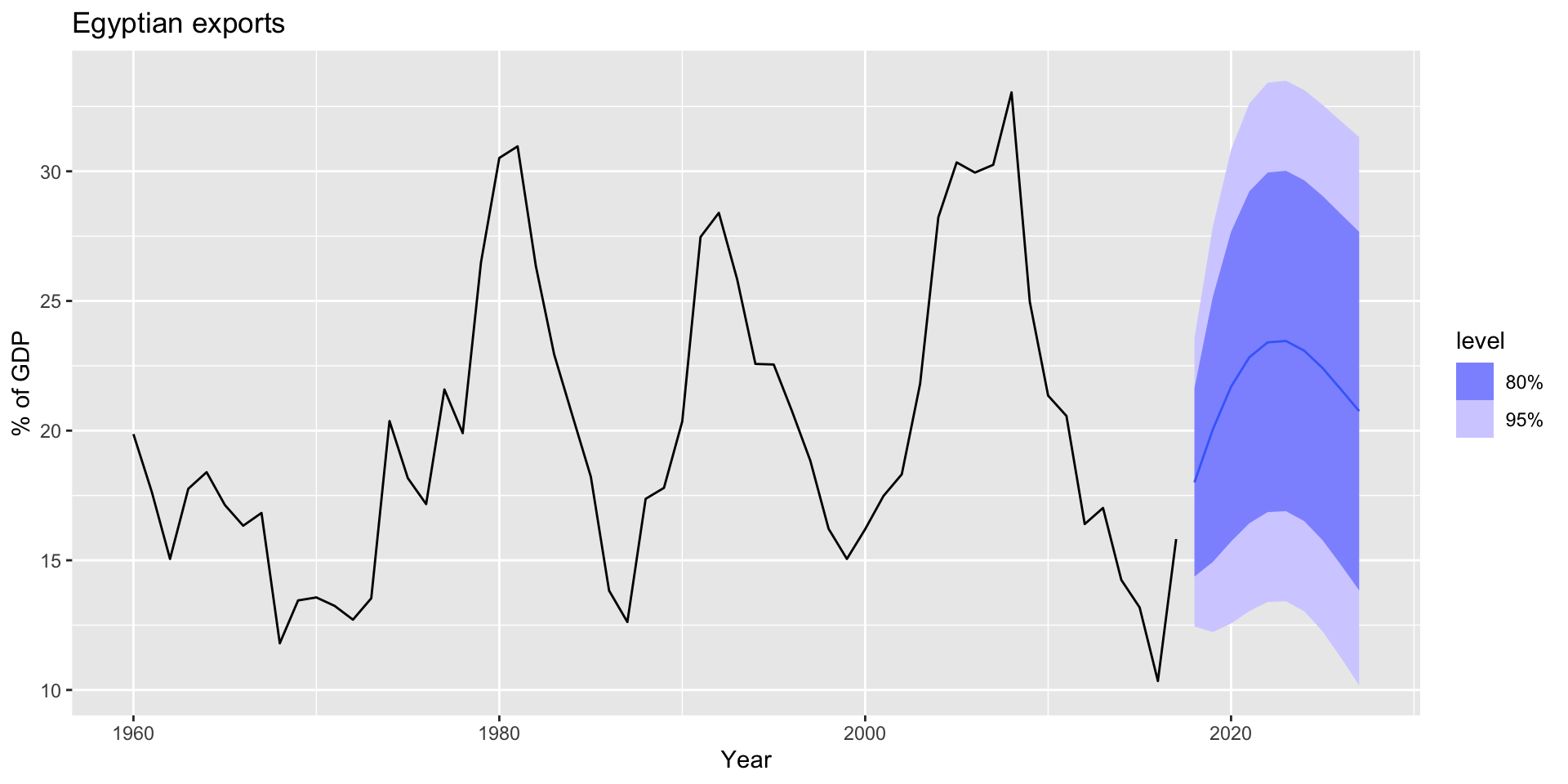

- Use

ARIMA()to automatically select appropriate values for \(p\), \(d\), and \(q\):

Series: Exports

Model: ARIMA(2,0,1) w/ mean

Coefficients:

ar1 ar2 ma1 constant

1.6764 -0.8034 -0.6896 2.5623

s.e. 0.1111 0.0928 0.1492 0.1161

sigma^2 estimated as 8.046: log likelihood=-141.57

AIC=293.13 AICc=294.29 BIC=303.43Example: Egyptian exports

- Forecast 10 years into the future:

Example: Egyptian exports

- Forecast 10 years into the future:

Notable parameter values

- If \(c=0\) and \(d=0\), forecasts \(\rightarrow\) 0.

- If \(c=0\) and \(d=1\), forecasts \(\rightarrow\) non-zero constant.

- If \(c=0\) and \(d=2\), forecasts \(\rightarrow\) straight line.

- If \(c \neq 0\) and \(d=0\), forecasts \(\rightarrow \bar{y}\).

- If \(c \neq 0\) and \(d=1\), forecasts \(\rightarrow\) straight line.

- If \(c \neq 0\) and \(d=2\), forecasts \(\rightarrow\) quadratic trend (this is bad)

- To obtain cyclic forecasts, \(p \geq 2\).