ARIMA I

BUS 323 Forecasting and Risk Analysis

Unit root tests

- Test whether a series has a unit root.

- A series has a unit root if it is integrated of order 1.

- That is, if it needs to be differenced to be stationary.

- Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test and Augmented Dickey-Fuller (ADF) test most common.

Implementation

- Use

unitroot_kpss():

Interpretation

unitroot_kpss()reports the p-value associated with the KPSS test.- \(H_{0}\) of the KPSS test is that the data are stationary.

- p-value of above was 0.01 or less

- \(\rightarrow\) reject \(H_{0}\)

- \(\rightarrow\) data are non-stationary.

- Difference the data and re-apply test.

Trying again…

- Apply unit root test to

Close':

How many differences?

- Use

unitroot_ndiffs()to find how mnay differences will be needed before the test detects a unit root.- Use

unitroot_nsdiffs()for seasonal data.

- Use

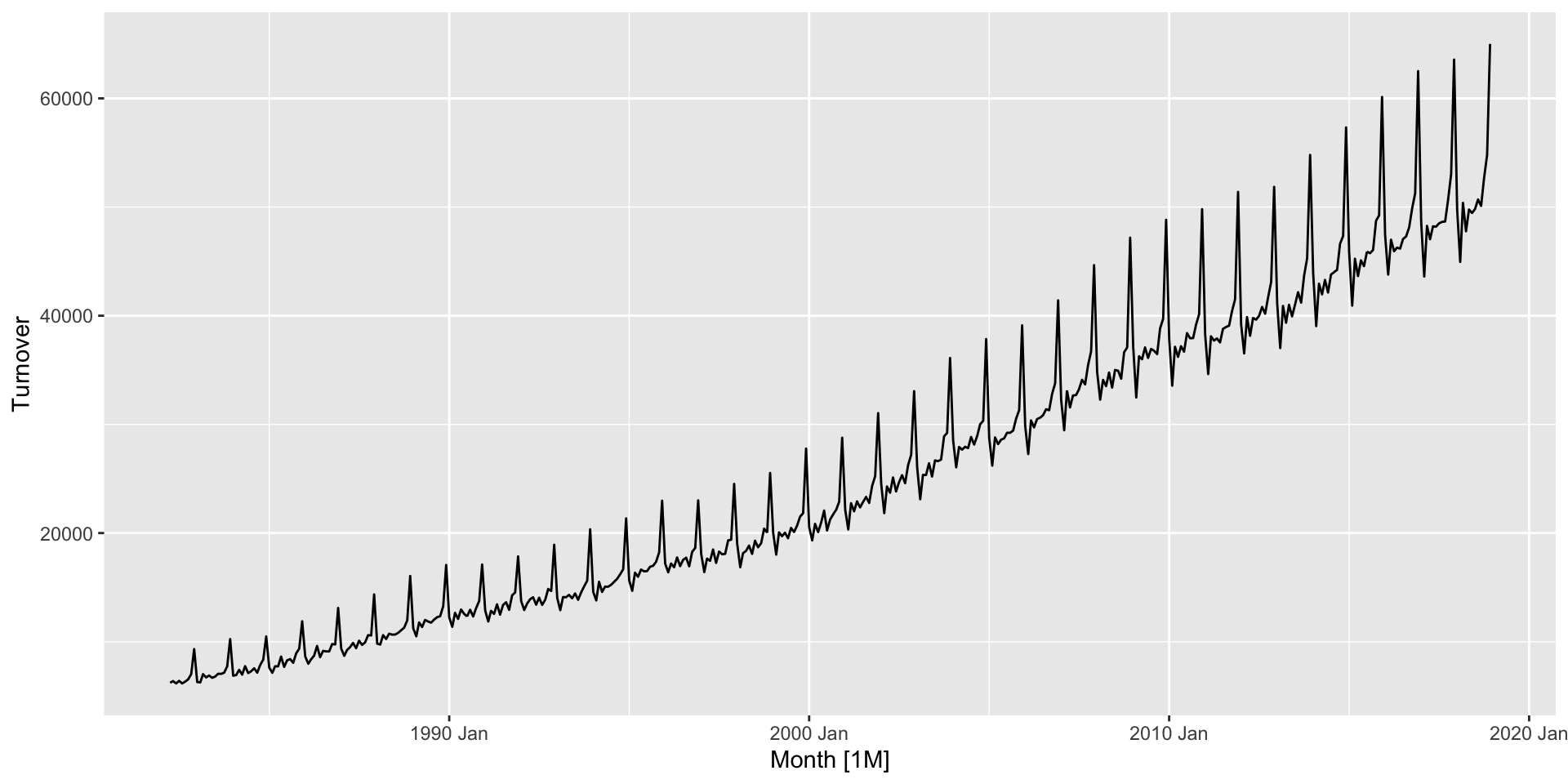

- Try it on monthly Australian retail turnover (from

aus_retail).

Example: Australian retail turnover

Example: Australian retail turnover

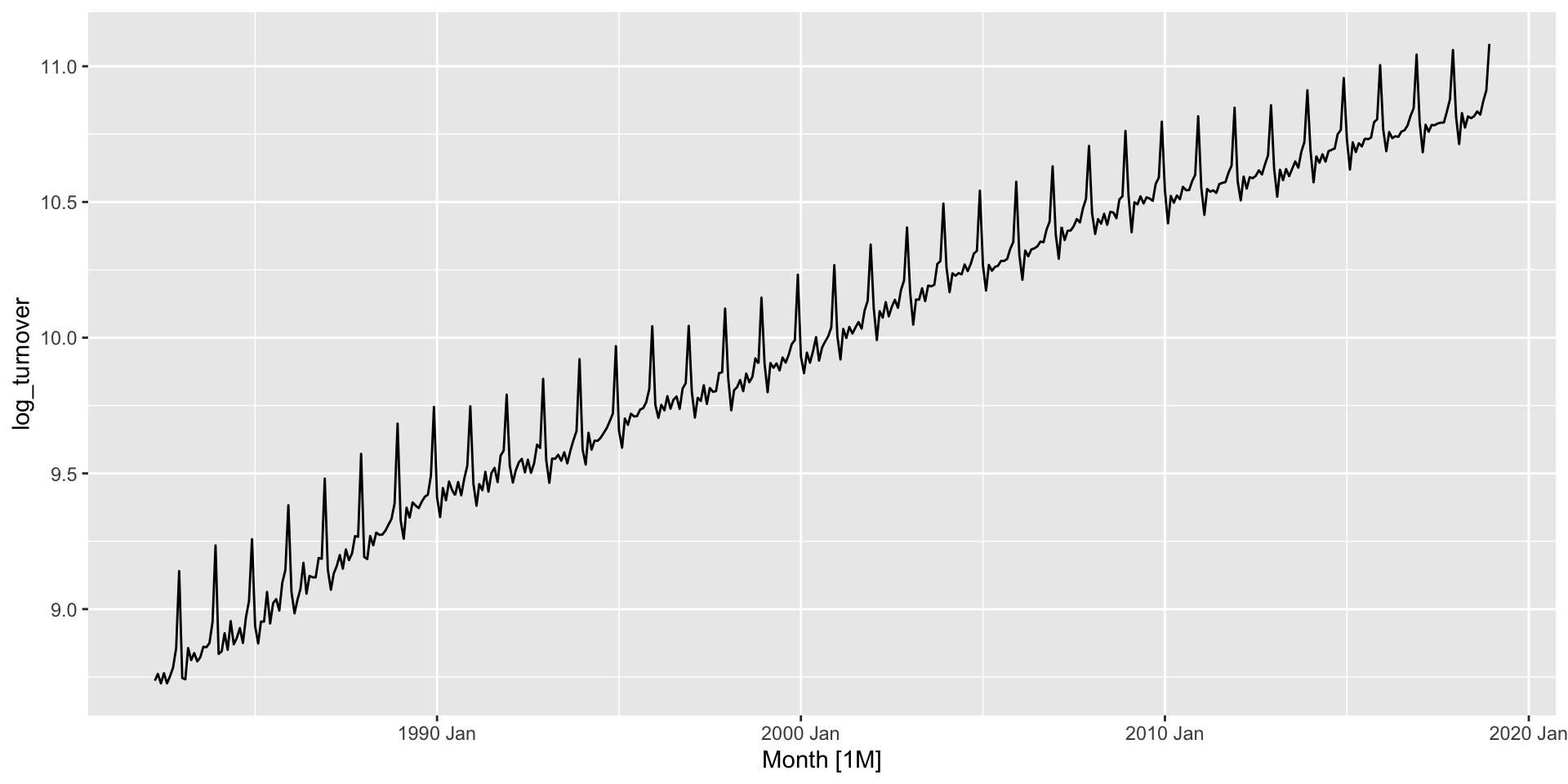

- Let’s try to log it:

Example: Australian retail turnover

- Try using

unitroot_nsdiffs():

Example: Australian retail turnover

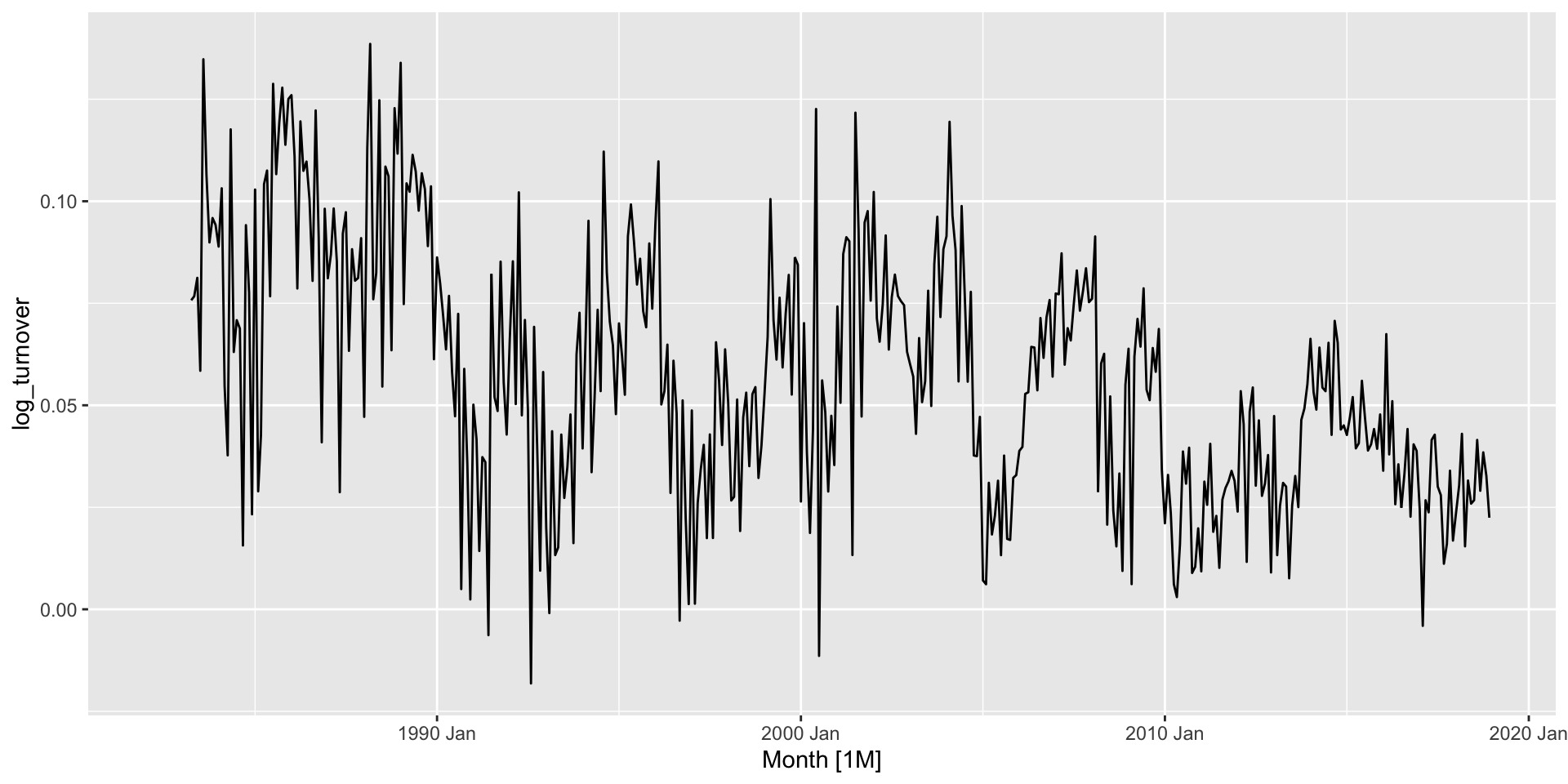

- Apply seasonal difference, then perform unit root test again:

Example: Australian retail turnover

- The test suggests one more difference is needed:

Example: Australian retail turnover

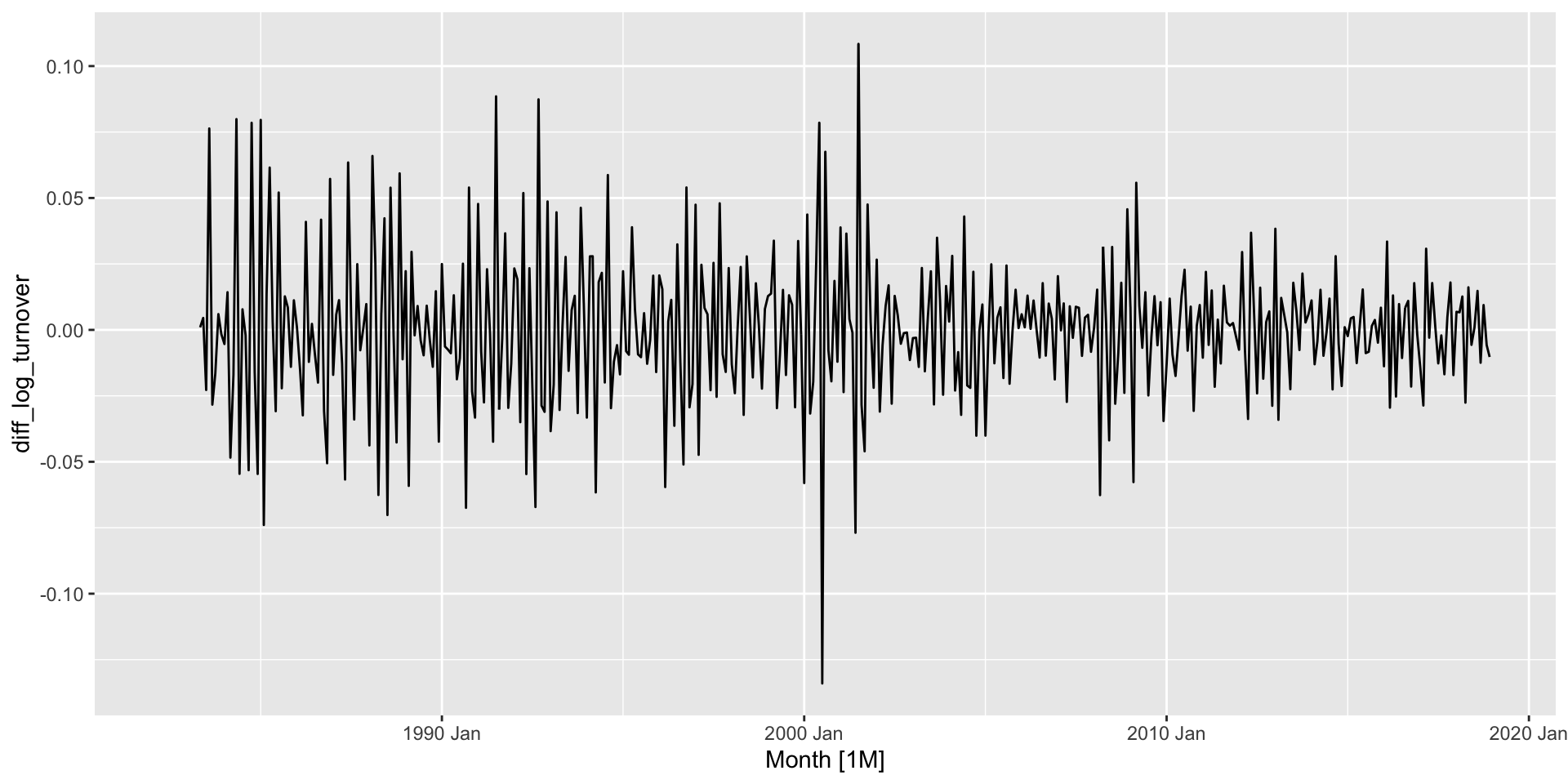

- Difference the seasonally differenced data, then test again:

Example: Australian retail turnover

Autoregressive models

- Forecast \(y_{t}\) based on past values of \(y\).

- AR(\(p\)):

\[ y_{t} = c + \phi_{1} y_{t-1} + \phi_{2} y_{t-2} + ... + \phi_{p} y_{t-p} + \epsilon_{t} \]

Autoregressive models

- For an AR(1) model:

- \(\phi_{1}=0\) and \(c=0\), \(y_{t}\) is white noise.

- \(\phi_{1} =1\) and \(c=0\), \(y_{t}\) is a random walk.

- \(\phi_{1}=1\) and \(c \neq 0\), \(y_{t}\) is a random walk with drift.

- \(\phi_{1} < 0\) results in \(y_{t}\) oscillating around its mean.

Autoregressive models

- AR models perform best on stationary data.

- Necessary constraints on parameters:

- For an AR(1): \(-1 < \phi_{1} < 1\).

- For an AR(2): \(-1 < \phi_{2} < 1\); \(\phi_{1} + \phi_{2} < 1\); \(\phi_{2} - \phi_{1} < 1\).

Implementation

- Use

ARIMA()(more later). Specify \(p\) in the first argument of the function. - e.g. let’s estimate an AR(2) based on the stationary series we found above:

ar_fit <- aus_total_retail |>

mutate(diff_log_turnover = difference(difference(log(Turnover),12),1)) |>

model(ar2 = ARIMA(diff_log_turnover ~ pdq(2,0,0)))

glance(ar_fit)# A tibble: 1 × 8

.model sigma2 log_lik AIC AICc BIC ar_roots ma_roots

<chr> <dbl> <dbl> <dbl> <dbl> <dbl> <list> <list>

1 ar2 0.000350 1089. -2168. -2168. -2148. <cpl [26]> <cpl [0]>Exercise

- Apply an AR(1) and AR(2) model to the stationary series derived last time. Which fits better? Try to plot the forecast and the data.