# A tibble: 1 × 4

adj_r_squared CV AIC AICc

<dbl> <dbl> <dbl> <dbl>

1 0.763 0.104 -457. -456.Time Series Regression: The Return

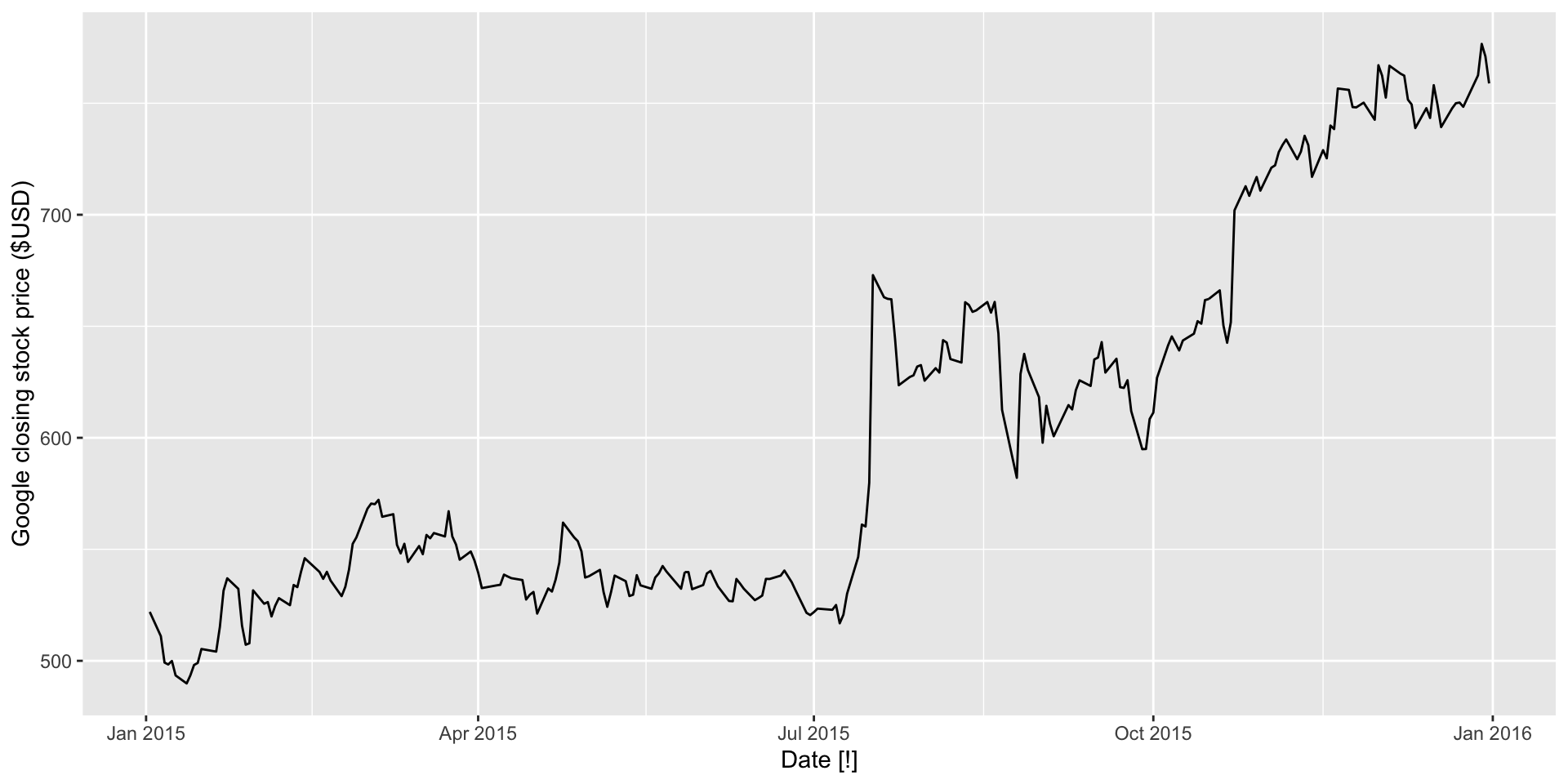

Example: plot

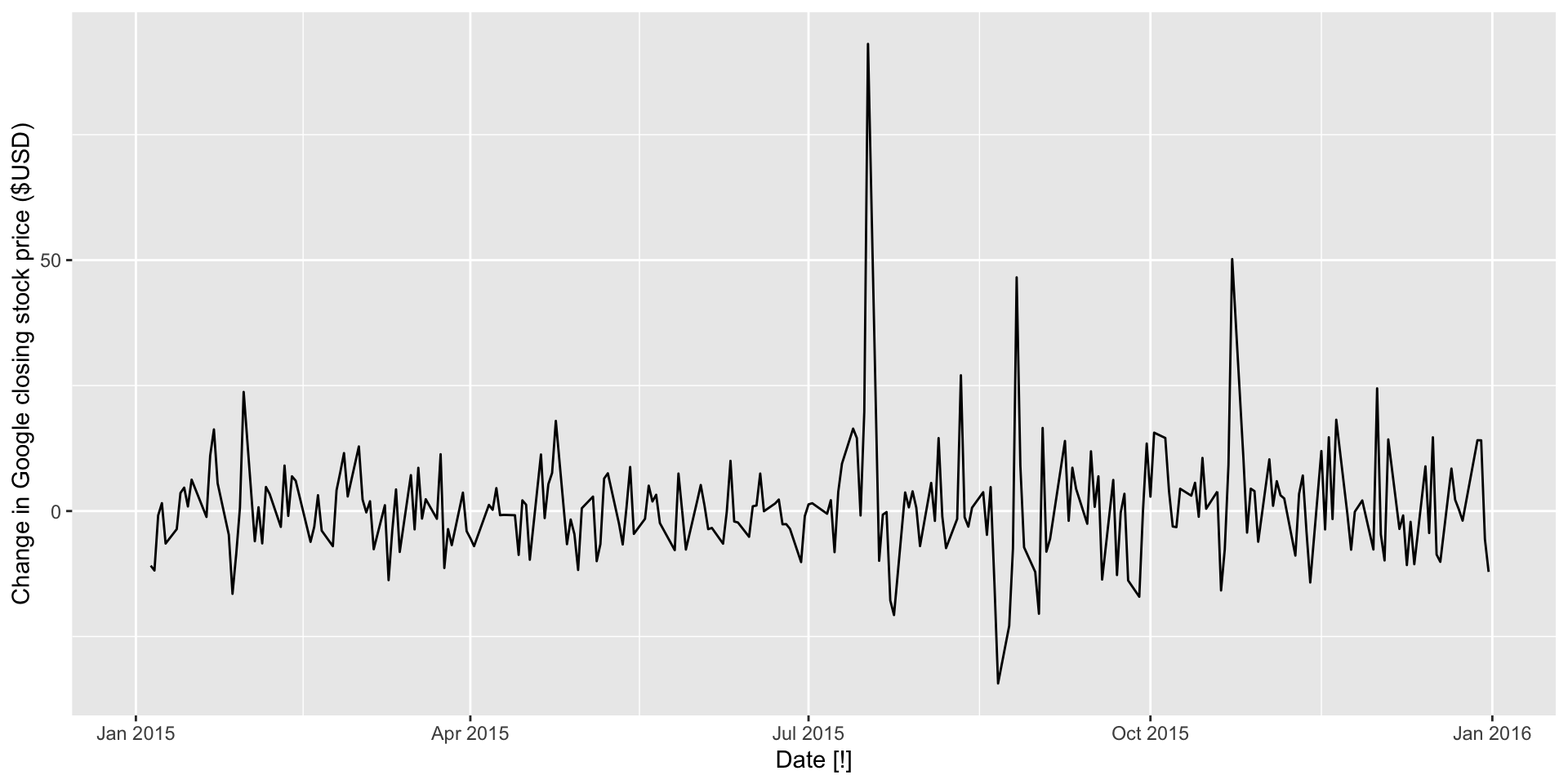

Example: first difference plot

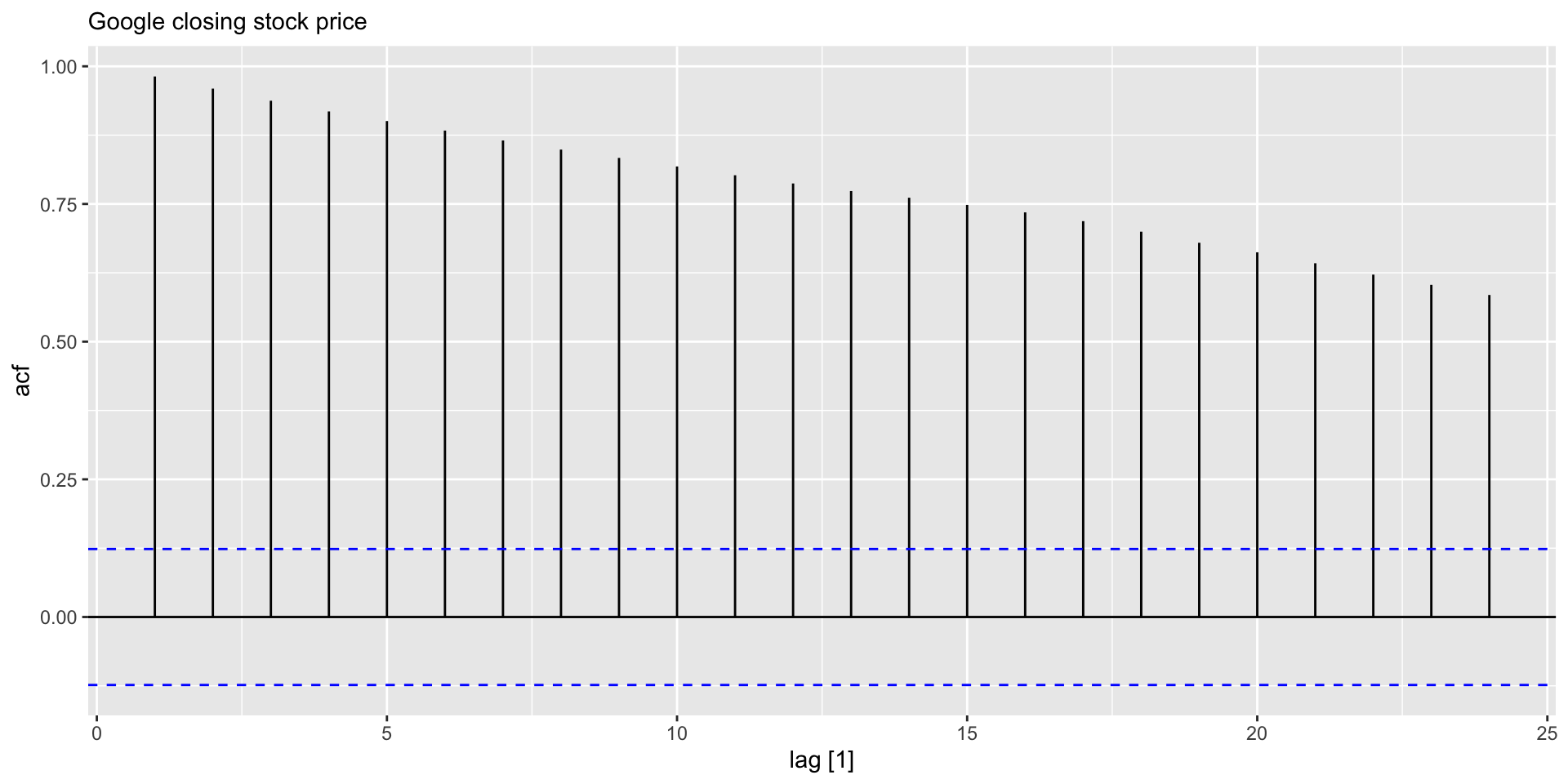

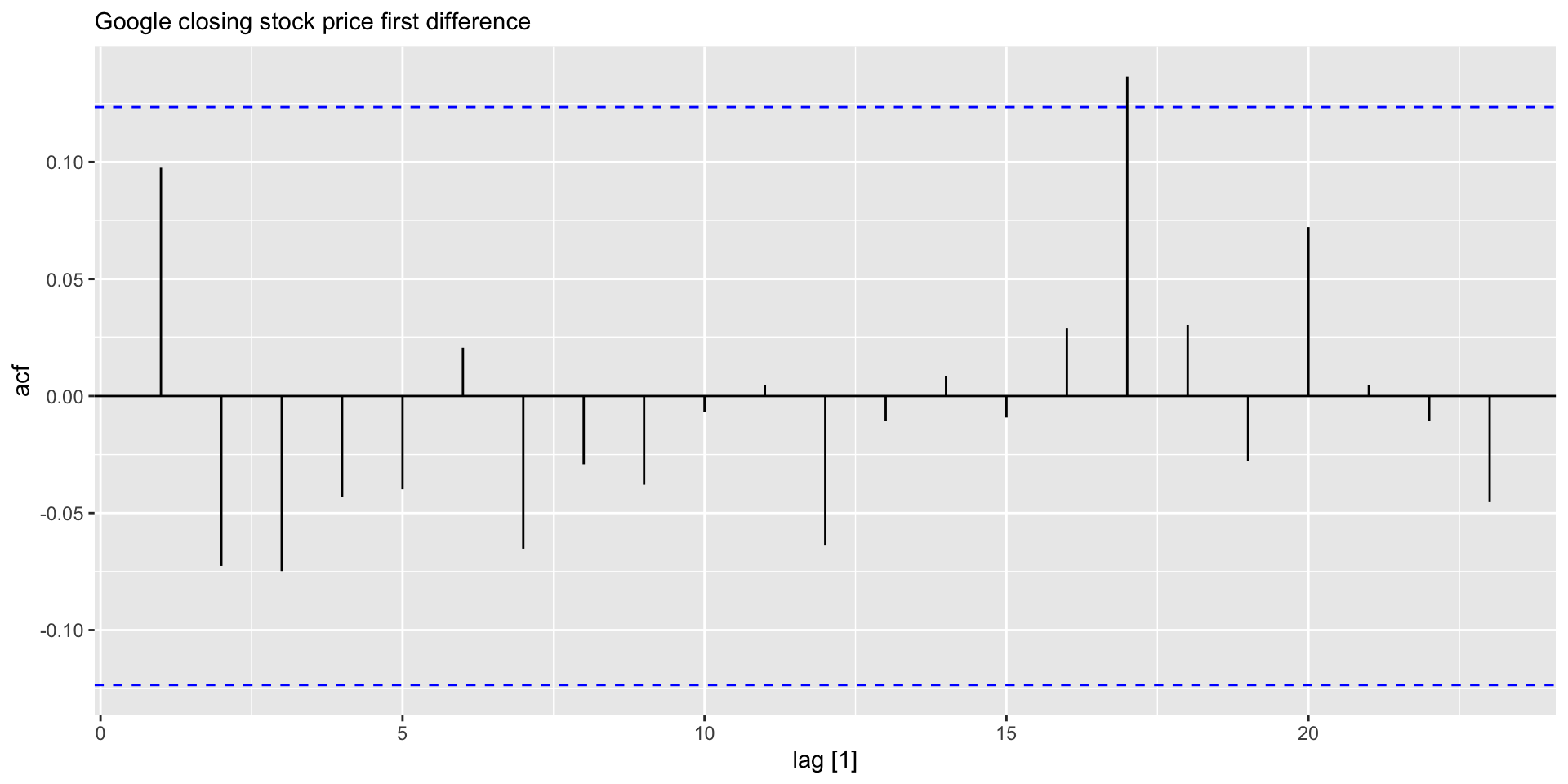

Example: ACF plots

- Check ACF for Google stock price and its first difference: