Exponential smoothing

Simple exponential smoothing

- Naive method:

\[ \widehat{y}_{T+h|T} = y_{T} \]

- All weight given to observation \(T\)

- Mean method:

\[ \widehat{y}_{T+h|T} = \frac{\sum_{t=1}^{T}y_{t}}{T} \]

- All observations equally weighted

Simple exponential smoothing

- We might want something in between.

- More weight to recent observations

- Less weight to those in the distant past

- Simple exponential smoothing

\[ \widehat{y}_{T+1|T} = \alpha y_{T} + \alpha(1-\alpha) y_{T-1} + \alpha(1-\alpha)^{2} y_{T-2} + ... \]

- \(0 \leq \alpha \leq 1\): smoothing parameter

Optimization

- Need to estimate \(\alpha\) and \(l_{0}\).

- As with regression, seek to minimize SSE (sum of squared errors):

\[ SSE = \sum_{t=1}^{T} (y_{t} - \widehat{y}_{t|t-1})^{2} = \sum_{t=1}^{t} e_{t}^{2} \]

- No OLS SSE-minimizing formulae here

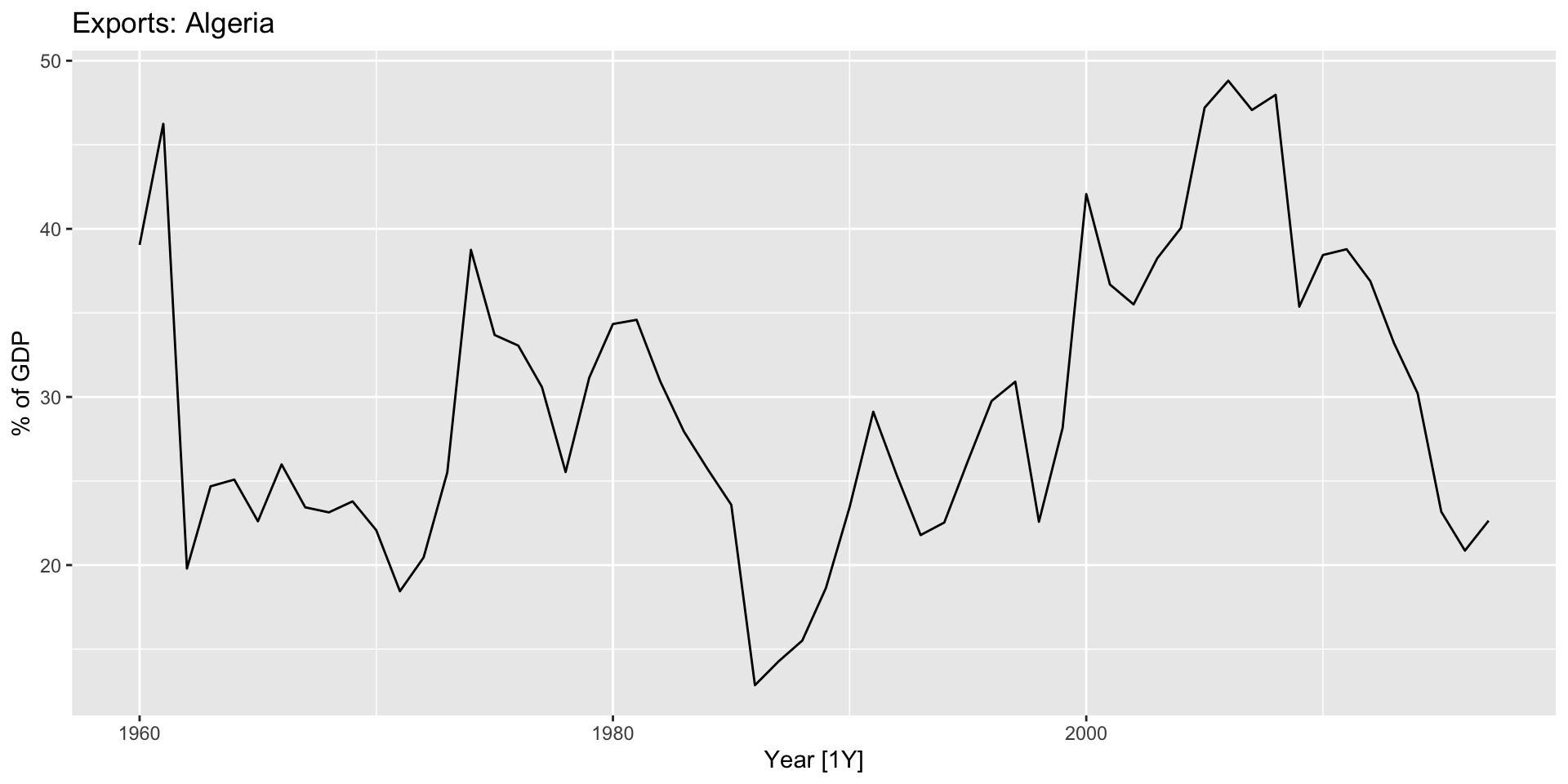

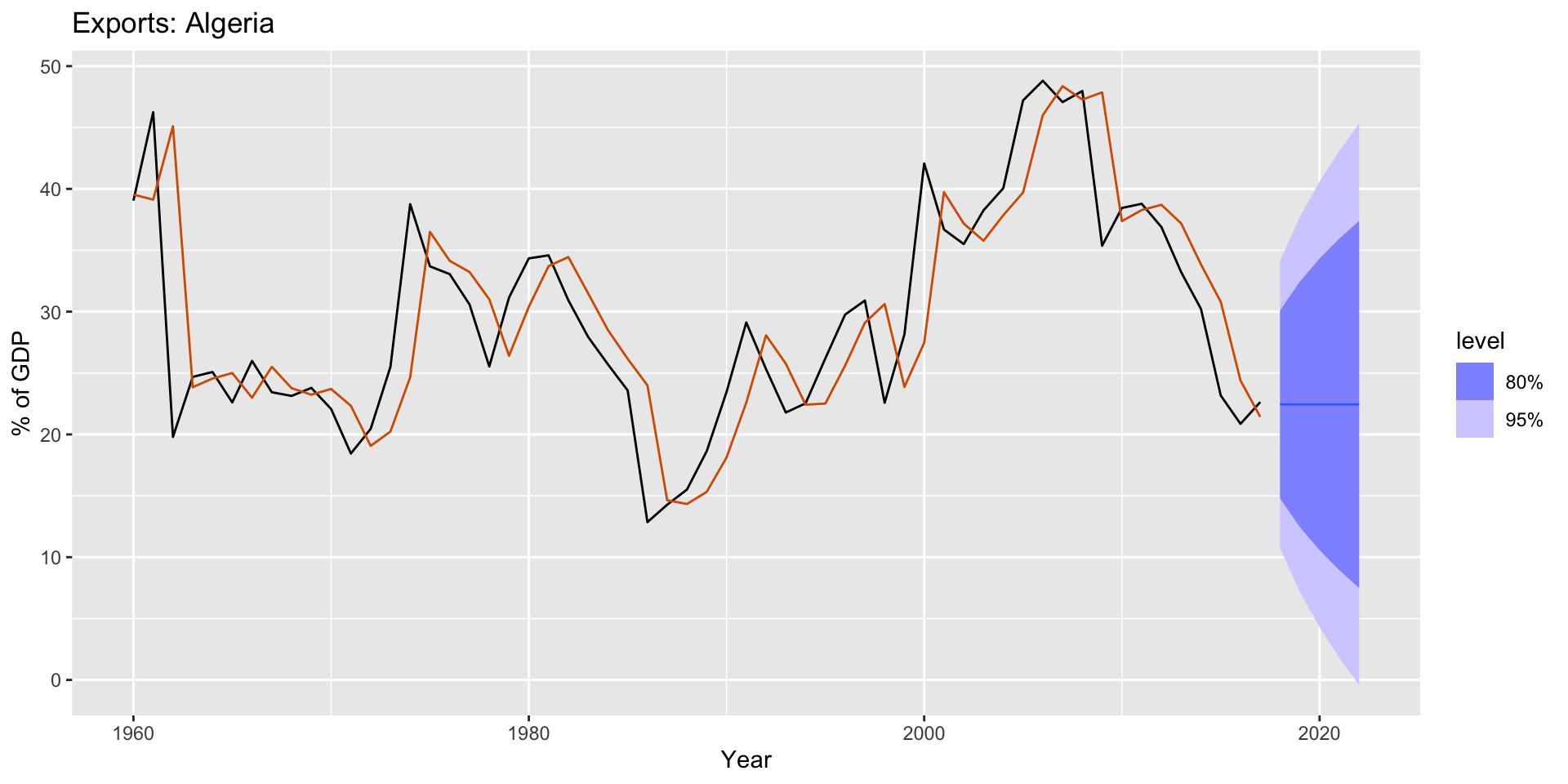

Example: Algerian exports

- Simple exponential smoothing works best with data with no trend or seasonality.

Example: Algerian exports

Example: Algerian exports

- To estimate an exponential smoothing model, use the

ETS()option inmodel():

Example: Algerian exports

- Produce a 5-step forecast:

Example: Algerian exports

- Plot forecast + historical data:

Example: Algerian exports

- Plot forecast + historical data:

Exponential smoothing with trend

- Holt’s linear trend method:

\[ \begin{align} \textrm{Forecast equation. } & \widehat{y}_{t+h|t} = l_{t} + hb_{t} \end{align} \]

\[ \begin{align} \textrm{Level equation. } & l_{t} = \alpha y_{t} + (1-\alpha)(l_{t-1} + b_{t-1}) \end{align} \]

\[ \begin{align} \textrm{Trend equation. } & b_{t} = \beta^{*} (l_{t} - l_{t-1}) + (1-\beta^{*})b_{t-1} \end{align} \]

- \(l_{t}\): level of \(y\) at \(t\)

- \(b_{t}\): trend of \(y\) at \(t\)

- \(\alpha\): smoothing parameter for level

- \(\beta^{*}\): smoothing parameter for trend

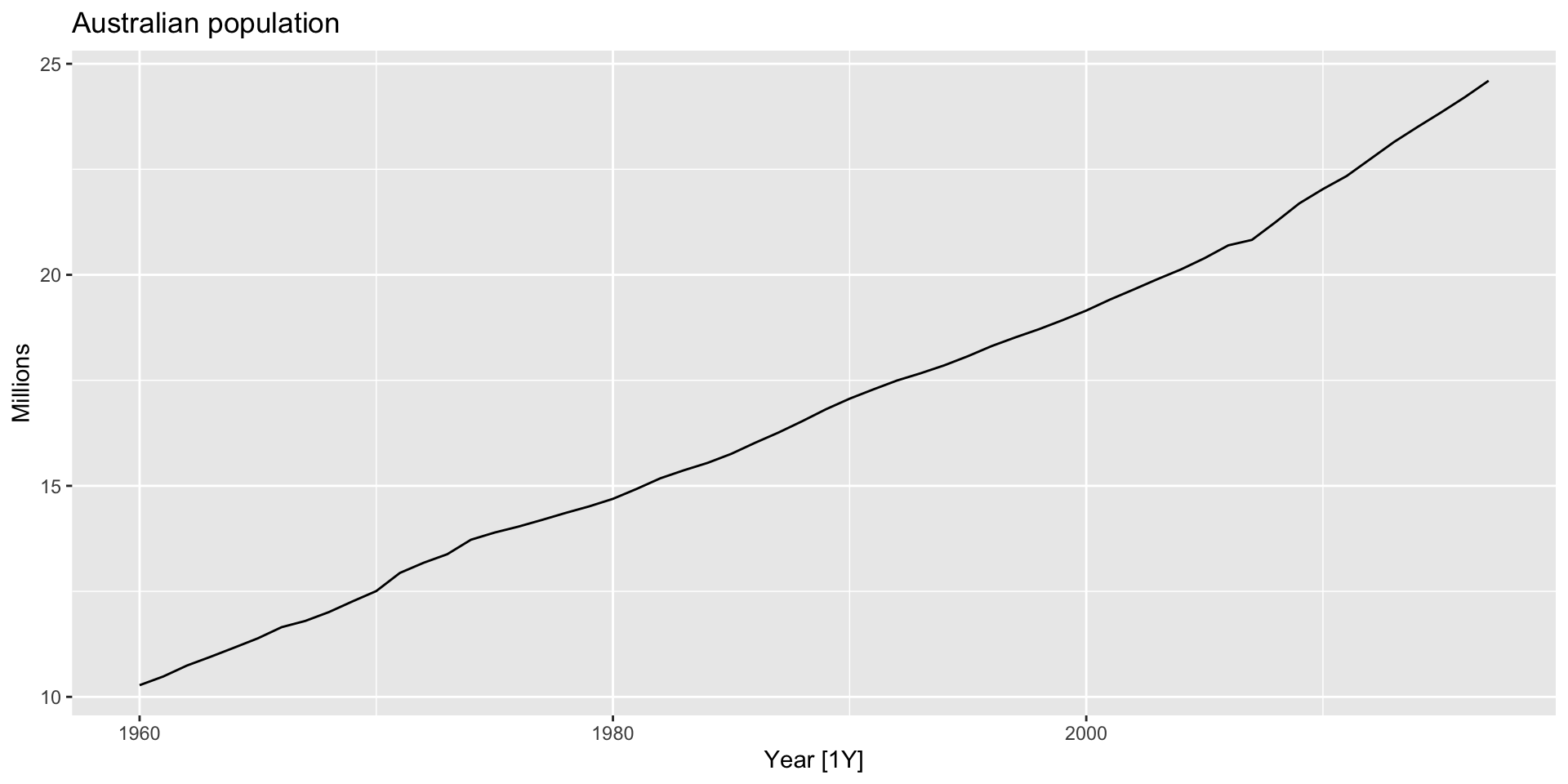

Example: Australian population

- Use a series with a trend:

Example: Australian population

- Use a series with a trend:

Example: Australian population

- Apply Holt’s method by using the

trend("A")option withinmodel(ETS()).- \(\alpha\), \(\beta^{*}\), \(l_{0}\), \(b_{0}\) estimated by minimizing SSE for one-step training errors.

Damped trend methods

- Gardner-McKenzie method:

\[ \widehat{y}_{t+h|t} = l_{t} + (\phi + \phi^{2} + ... + \phi^{h})b_{t} \]

- \(0 < \phi < 1\): damping parameter

\[ l_{t} = \alpha y_{t} + (1-\alpha)(l_{t-1} + \phi b_{t-1}) \]

\[ b_{t} = \beta^{*}(l_{t}-l_{t-1}) + (1-\beta^{*}) \phi b_{t-1} \]

- Forecasts converge to \(l_{T} + \frac{\phi b_{T}}{1-\phi}\) in the limit of \(h\)

- Long-run forecasts: constant

- Short-run forecasts: trended

- \(0 < \phi < 1\): damping parameter

- Usually \(0.8 \leq \phi \leq 0.98\).

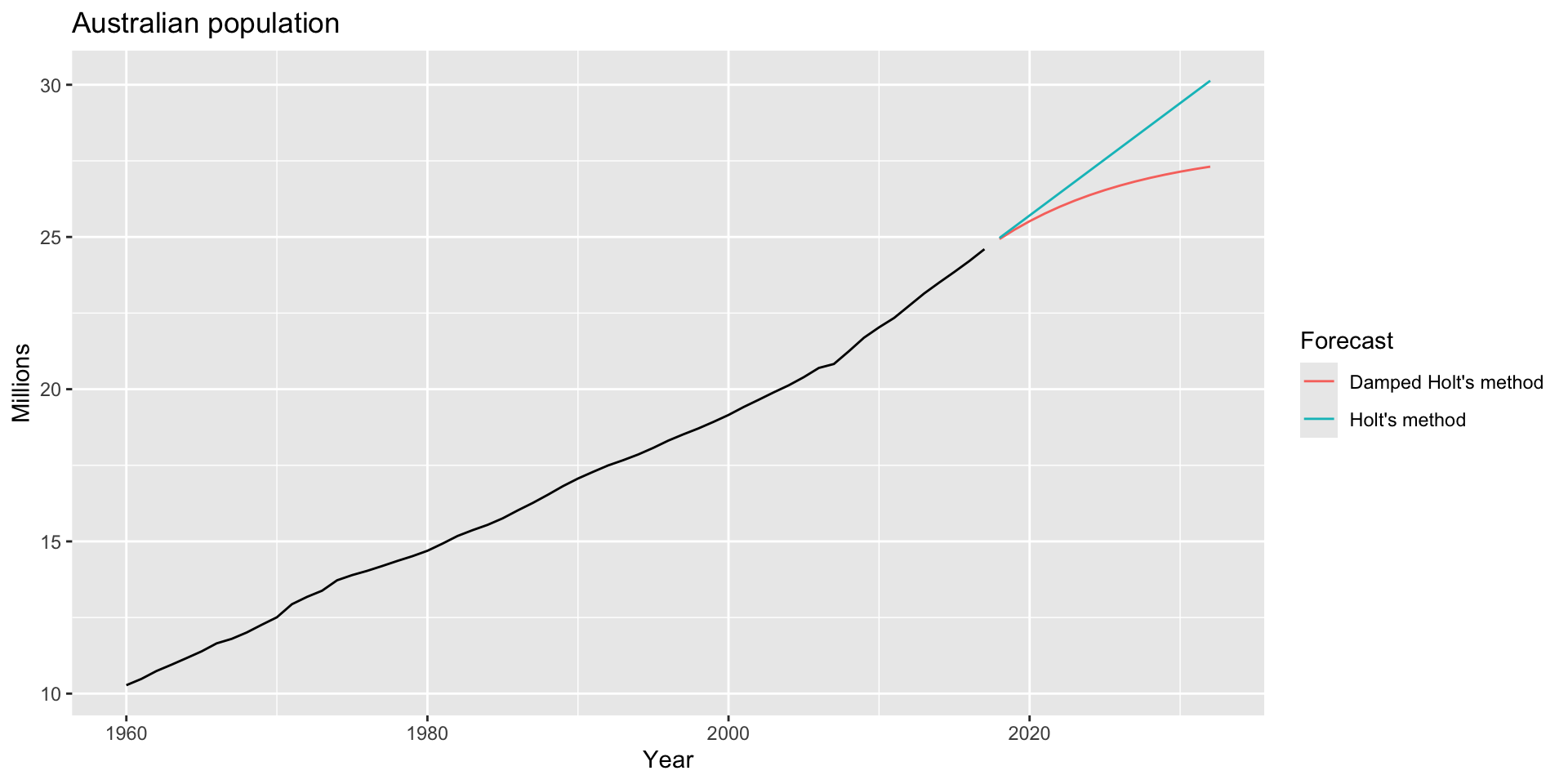

Example: Australian population

- Compare a trended model to a damped trended model (use \(\phi=0.9\)). Estimate 15-step forecasts:

aus_economy |>

model(

`Holt's method` = ETS(Pop ~ error("A") +

trend("A") + season("N")),

`Damped Holt's method` = ETS(Pop ~ error("A") +

trend("Ad", phi = 0.9) + season("N"))

) |>

forecast(h=15)# A fable: 30 x 5 [1Y]

# Key: Country, .model [2]

Country .model Year

<fct> <chr> <dbl>

1 Australia Holt's method 2018

2 Australia Holt's method 2019

3 Australia Holt's method 2020

4 Australia Holt's method 2021

5 Australia Holt's method 2022

6 Australia Holt's method 2023

7 Australia Holt's method 2024

8 Australia Holt's method 2025

9 Australia Holt's method 2026

10 Australia Holt's method 2027

# ℹ 20 more rows

# ℹ 2 more variables: Pop <dist>, .mean <dbl>Example: Australian population

- And plot:

aus_economy |>

model(

`Holt's method` = ETS(Pop ~ error("A") +

trend("A") + season("N")),

`Damped Holt's method` = ETS(Pop ~ error("A") +

trend("Ad", phi = 0.9) + season("N"))

) |>

forecast(h = 15) |>

autoplot(aus_economy, level = NULL) +

labs(title = "Australian population",

y = "Millions") +

guides(colour = guide_legend(title = "Forecast"))Example: Australian population

- And plot:

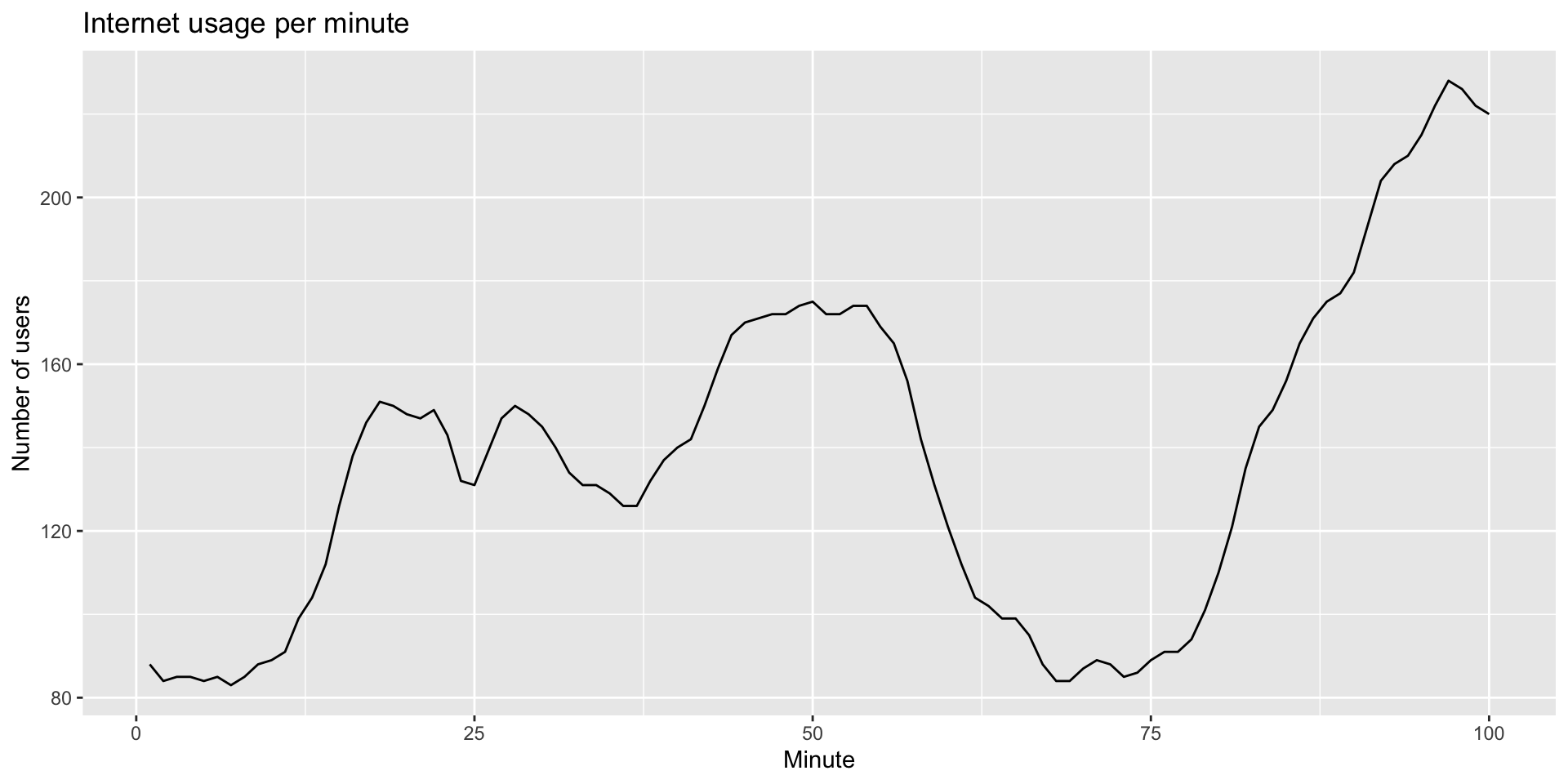

Example: internet usage

- Which method works best for these data?

Example: internet usage

- Which method works best for these data?

Example: internet usage

- Estimate a 1-step forecast for all three smoothing methods.

- Use cross-validation (use an initial sample of size 10) to evaluate accuracy.

www_usage |>

stretch_tsibble(.init = 10) |>

model(

SES = ETS(value ~ error("A") + trend("N") + season("N")),

Holt = ETS(value ~ error("A") + trend("A") + season("N")),

Damped = ETS(value ~ error("A") + trend("Ad") +

season("N"))

) |>

forecast(h = 1) |>

accuracy(www_usage)# A tibble: 3 × 10

.model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

<chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 Damped Test 0.288 3.69 3.00 0.347 2.26 0.663 0.636 0.336

2 Holt Test 0.0610 3.87 3.17 0.244 2.38 0.701 0.668 0.296

3 SES Test 1.46 6.05 4.81 0.904 3.55 1.06 1.04 0.803Example: internet usage

- Use the best-performing method to forecast 10 steps into the future. Estimate:

Example: internet usage

- Forecast: