Time series cross-validation

BUS 323 Forecasting and Risk Analysis

Cross-validation

- Many training sets, many test sets.

- Can be used for one- or multi-step forecasts.

stretch_tsibble()

stretch_tsibble()can be used to create many training sets..initdefines length of initial training set..stepdefines by how much each successive training set increases in length.

Example: Google stock data

- Using our 2015 Google stock price data again:

Example: Google stock data

- Use

stretch_tsibble()with.init=3and.step=1. - Use

relocate()to put index variables up front:

google_2015_tr <- google_2015 |>

stretch_tsibble(.init = 3, .step = 1) |>

relocate(Date, Symbol, .id)

google_2015_tr# A tsibble: 31,875 x 10 [1]

# Key: Symbol, .id [250]

Date Symbol .id Open High Low Close Adj_Close Volume day

<date> <chr> <int> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <int>

1 2015-01-02 GOOG 1 526. 528. 521. 522. 522. 1447600 1

2 2015-01-05 GOOG 1 520. 521. 510. 511. 511. 2059800 2

3 2015-01-06 GOOG 1 512. 513. 498. 499. 499. 2899900 3

4 2015-01-02 GOOG 2 526. 528. 521. 522. 522. 1447600 1

5 2015-01-05 GOOG 2 520. 521. 510. 511. 511. 2059800 2

6 2015-01-06 GOOG 2 512. 513. 498. 499. 499. 2899900 3

7 2015-01-07 GOOG 2 504. 504. 497. 498. 498. 2065100 4

8 2015-01-02 GOOG 3 526. 528. 521. 522. 522. 1447600 1

9 2015-01-05 GOOG 3 520. 521. 510. 511. 511. 2059800 2

10 2015-01-06 GOOG 3 512. 513. 498. 499. 499. 2899900 3

# ℹ 31,865 more rowsExample: Google stock data

- Use

accuracy()to evaluate forecast accuracy across training sets:

# A tibble: 1 × 11

.model Symbol .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

<chr> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 RW(Close ~ drif… GOOG Test 0.726 11.3 7.26 0.112 1.19 1.02 1.01 0.0985Example: Google stock data

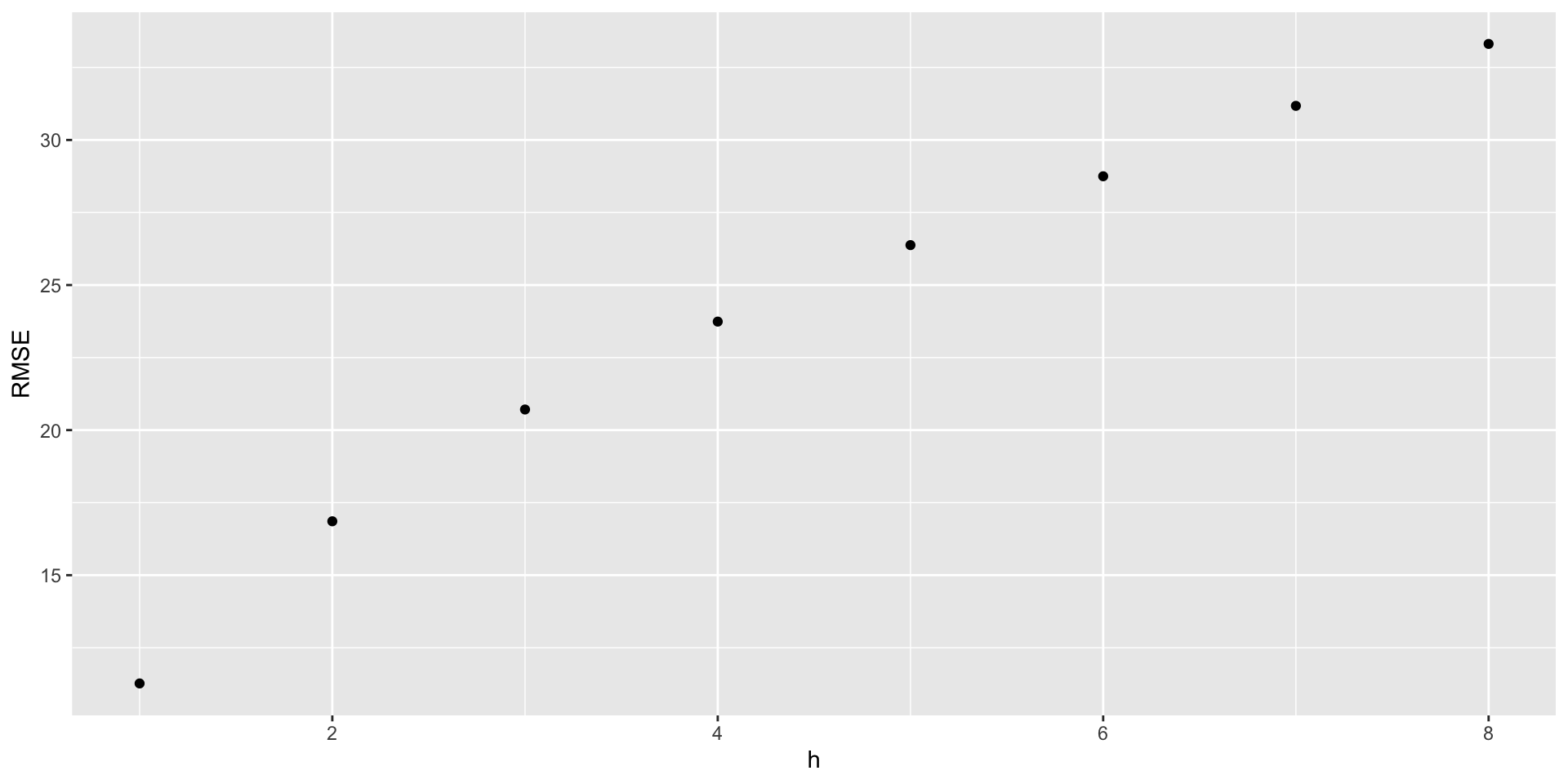

- We can evaluate the accuracy of multi-step forecasts:

Example: Google stock data

- We can evaluate the accuracy of multi-step forecasts:

Example: Google stock data

- We can evaluate the accuracy of multi-step forecasts:

Example: Google stock data

- We can evaluate the accuracy of multi-step forecasts:

# A tibble: 8 × 11

h .model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

<int> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1 RW(Close ~ drift… Test 0.726 11.3 7.26 0.112 1.19 1.02 1.01 0.0985

2 2 RW(Close ~ drift… Test 1.52 16.9 11.0 0.228 1.82 1.54 1.51 0.509

3 3 RW(Close ~ drift… Test 2.34 20.7 14.0 0.350 2.32 1.96 1.85 0.668

4 4 RW(Close ~ drift… Test 3.15 23.7 16.0 0.474 2.65 2.24 2.12 0.749

5 5 RW(Close ~ drift… Test 3.93 26.4 17.7 0.596 2.94 2.48 2.36 0.791

6 6 RW(Close ~ drift… Test 4.71 28.7 19.3 0.718 3.21 2.71 2.57 0.827

7 7 RW(Close ~ drift… Test 5.49 31.2 21.3 0.837 3.53 2.99 2.79 0.833

8 8 RW(Close ~ drift… Test 6.27 33.3 22.6 0.958 3.75 3.17 2.98 0.848 Example: Google stock data

- We can evaluate the accuracy of multi-step forecasts:

Example: Google stock data

- We can evaluate the accuracy of multi-step forecasts: