Evaluating forecast accuracy

BUS 323 Forecasting and Risk Analysis

Training and test sets

- Accuracy: more than error size

- Evaluate forecast performance on historical data

- Separate into training and test sets

- Test set: ~20% of the full sample

- Or at least as large as the forecast horizon

Training and test sets

- A couple things to note:

- Good fit with training data \(\neq\) good forecast

- More parameters \(\rightarrow\) perfect fit

- Over-fitting does not yield a good forecast.

- “Test set” aka “holdout set” or “out-of-sample data”.

Subsetting functions

filter()- e.g. To extract all data from 1995 onward:

# A tsibble: 62 x 7 [1Q]

Quarter Beer Tobacco Bricks Cement Electricity Gas

<qtr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1995 Q1 426 4714 430 1626 41768 131

2 1995 Q2 408 3939 457 1703 43686 167

3 1995 Q3 416 6137 417 1733 46022 181

4 1995 Q4 520 4739 370 1545 42800 145

5 1996 Q1 409 4275 310 1526 43661 133

6 1996 Q2 398 5239 358 1593 44707 162

7 1996 Q3 398 6293 379 1706 46326 184

8 1996 Q4 507 5575 369 1699 43346 146

9 1997 Q1 432 4802 330 1511 43938 135

10 1997 Q2 398 5523 390 1785 45828 171

# ℹ 52 more rowsSubsetting functions

filter()- Equivalently:

# A tsibble: 62 x 7 [1Q]

Quarter Beer Tobacco Bricks Cement Electricity Gas

<qtr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1995 Q1 426 4714 430 1626 41768 131

2 1995 Q2 408 3939 457 1703 43686 167

3 1995 Q3 416 6137 417 1733 46022 181

4 1995 Q4 520 4739 370 1545 42800 145

5 1996 Q1 409 4275 310 1526 43661 133

6 1996 Q2 398 5239 358 1593 44707 162

7 1996 Q3 398 6293 379 1706 46326 184

8 1996 Q4 507 5575 369 1699 43346 146

9 1997 Q1 432 4802 330 1511 43938 135

10 1997 Q2 398 5523 390 1785 45828 171

# ℹ 52 more rowsSubsetting functions

slice()- To extract the last 20 observations:

# A tsibble: 20 x 7 [1Q]

Quarter Beer Tobacco Bricks Cement Electricity Gas

<qtr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 2005 Q3 408 NA NA 2340 56043 221

2 2005 Q4 482 NA NA 2265 54992 180

3 2006 Q1 438 NA NA 2027 57112 171

4 2006 Q2 386 NA NA 2278 57157 224

5 2006 Q3 405 NA NA 2427 58400 233

6 2006 Q4 491 NA NA 2451 56249 192

7 2007 Q1 427 NA NA 2140 56244 187

8 2007 Q2 383 NA NA 2362 55036 234

9 2007 Q3 394 NA NA 2536 59806 245

10 2007 Q4 473 NA NA 2562 56411 205

11 2008 Q1 420 NA NA 2183 59118 194

12 2008 Q2 390 NA NA 2558 56660 229

13 2008 Q3 410 NA NA 2612 64067 249

14 2008 Q4 488 NA NA 2373 59045 203

15 2009 Q1 415 NA NA 1963 58368 196

16 2009 Q2 398 NA NA 2160 57471 238

17 2009 Q3 419 NA NA 2325 58394 252

18 2009 Q4 488 NA NA 2273 57336 210

19 2010 Q1 414 NA NA 1904 58309 205

20 2010 Q2 374 NA NA 2401 58041 236Subsetting functions

slice()- To subset the first year of data from each

StateandIndustry:

- To subset the first year of data from each

# A tsibble: 1,824 x 5 [1M]

# Key: State, Industry [152]

# Groups: State, Industry [152]

State Industry `Series ID` Month Turnover

<chr> <chr> <chr> <mth> <dbl>

1 Australian Capital Territory Cafes, restaurant… A3349849A 1982 Apr 4.4

2 Australian Capital Territory Cafes, restaurant… A3349849A 1982 May 3.4

3 Australian Capital Territory Cafes, restaurant… A3349849A 1982 Jun 3.6

4 Australian Capital Territory Cafes, restaurant… A3349849A 1982 Jul 4

5 Australian Capital Territory Cafes, restaurant… A3349849A 1982 Aug 3.6

6 Australian Capital Territory Cafes, restaurant… A3349849A 1982 Sep 4.2

7 Australian Capital Territory Cafes, restaurant… A3349849A 1982 Oct 4.8

8 Australian Capital Territory Cafes, restaurant… A3349849A 1982 Nov 5.4

9 Australian Capital Territory Cafes, restaurant… A3349849A 1982 Dec 6.9

10 Australian Capital Territory Cafes, restaurant… A3349849A 1983 Jan 3.8

# ℹ 1,814 more rowsForecast errors

- Forecast residuals based on training set.

- Forecast errors based on test set.

\[ e_{T+h} = y_{T+h} - \widehat{y}_{T+h|T} \]

- We’ll use these to evaluate forecast accuracy.

Scale-dependent errors

- Forecast errors are on the same scale as the time series being forecasted.

- Any measure of accuracy based on errors will be similarly scaled.

- Two common measures:

\[ \textrm{Mean absolute error: } MAE = \bar{|e_{t}|} \]

\[ \textrm{Root mean squared error: } RMSE = \sqrt{\bar{e_{t}}^{2}} \]

- RMSE commonly used as an objective function for forecast methods.

Percentage errors

- Used to compare performance across time series

- Most common measure:

\[ \textrm{Mean absolute percentage error: } MAPE = \bar{|p_{t}|} \]

- Where \(p_{t} = 100 \frac{e_{t}}{y_{t}}\).

- Percentage errors cause problems when \(y_{t}\) is small.

Example: defining train/test

- Use

aus_production. Filter such thatyearis \(\geq\) 1992. Then define the period 1992-2007 as the training set:

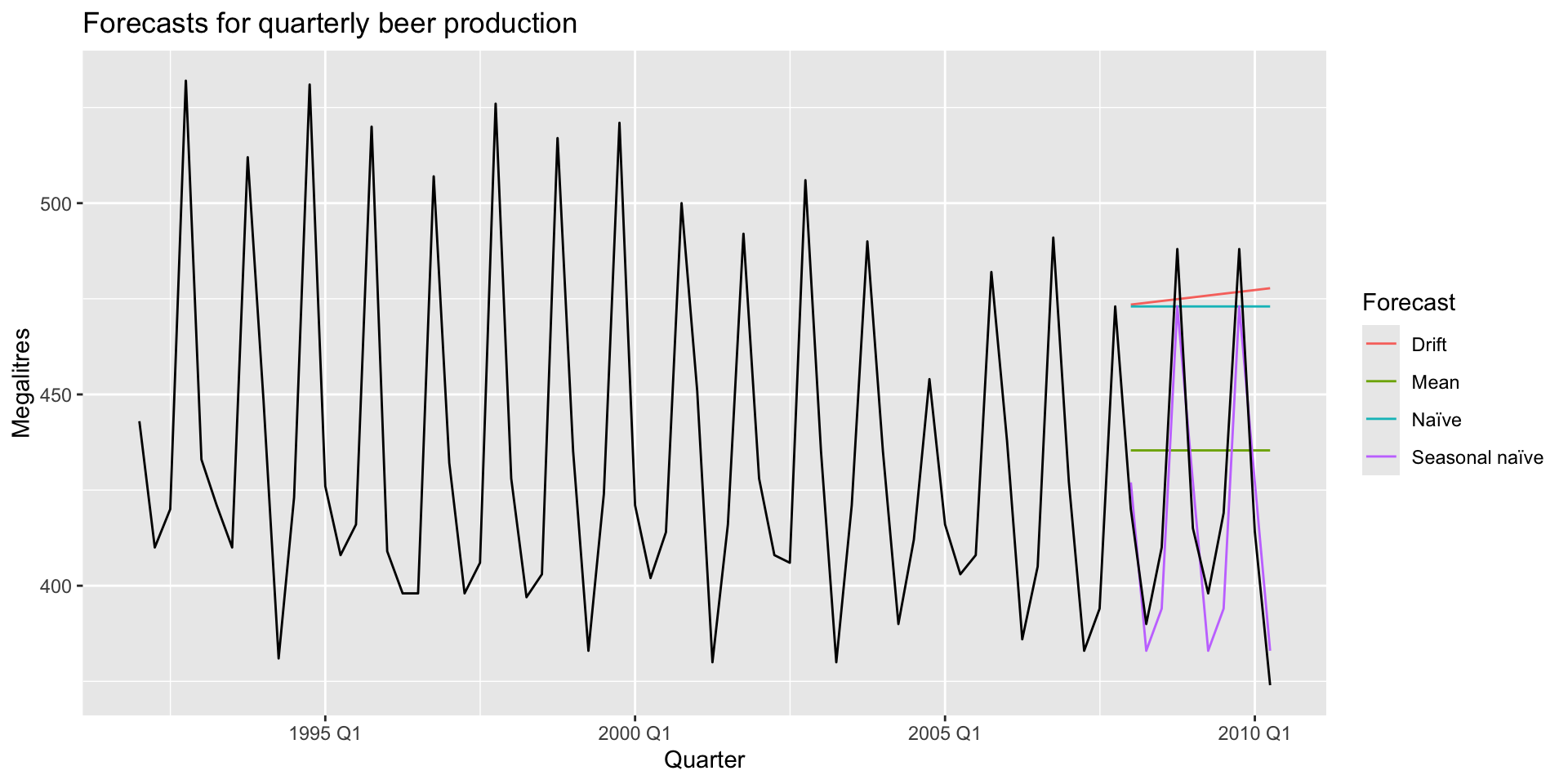

Example: forecasting

- 10 observations exist in the test set. Produce a mean, naive, seasonal naive, and drift forecast for those observations.

Example: plotting

- Plot all forecasts with

autoplot()and add in observed data:

Example: plotting

Example: forecast accuracy

- Use the

accuracy()function. Supply the forecast object (beer_fc) and the observed data (`recent_production)

# A tibble: 4 × 10

.model .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

<chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 Drift Test -54.0 64.9 58.9 -13.6 14.6 4.12 3.87 -0.0741

2 Mean Test -13.8 38.4 34.8 -3.97 8.28 2.44 2.29 -0.0691

3 Naïve Test -51.4 62.7 57.4 -13.0 14.2 4.01 3.74 -0.0691

4 Seasonal naïve Test 5.2 14.3 13.4 1.15 3.17 0.937 0.853 0.132 Example: Google stock price

- Use the 2015 Google stock price data previously constructed. We’ll produce forecasts for January 2016.

# Re-index based on trading days

google_stock <- gafa_stock |>

filter(Symbol == "GOOG", year(Date) >= 2015) |>

mutate(day = row_number()) |>

update_tsibble(index = day, regular = TRUE)

# Filter for training set

google_2015 <- google_stock |> filter(year(Date) == 2015)

# Filter for test set

google_jan_2016 <- google_stock |>

filter(yearmonth(Date) == yearmonth("2016 Jan"))Example: Google stock price

- Produce a mean, naive, and drift forecast for January 2016. Plot the historical data and the forecasts.

Example: Google stock price

- Evaluate each forecast’s accuracy.

# A tibble: 3 × 11

.model Symbol .type ME RMSE MAE MPE MAPE MASE RMSSE ACF1

<chr> <chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 Drift GOOG Test -49.8 53.1 49.8 -6.99 6.99 6.99 4.74 0.604

2 Mean GOOG Test 117. 118. 117. 16.2 16.2 16.4 10.5 0.496

3 Naïve GOOG Test -40.4 43.4 40.4 -5.67 5.67 5.67 3.88 0.496