Forecasting with transformations and decomposition

BUS 323 Forecasting and Risk Analysis

Forecasting with transformed data

- Tranform data to improve forecast stability \(w_{t} = f(y_{t}\))

- Forecast transformed variable \(w_{t}\)

- Back-transform to obtain forecasts for \(y_{t}\)

Prediction intervals with transformed data

- Prediction interval computed for \(\widehat{w}_{t}\)

- End-points back-transformed

- Prediction interval not necessarily symmetric

Bias adjustments

- Back-transformed point forecast not necessarily mean

- Typically median

- Problem?

- Larger variance \(\rightarrow\) more difference between median and mean

Example: Box-Cox transformation

- The back-transformation for a Box-Cox transformation is given by:

\[ \widehat{y}_{T+h|T} = \left\{\begin{array}{lr} exp(\widehat{w}_{T+h|T}) & \textrm{if} \lambda=0; \\ sin(\lambda \widehat{w}_{T+h|T} + 1)(\lambda \widehat{w}_{T+h|T} + 1)^{1/\lambda} & \textrm{otherwise}. \end{array}\right\} \]

- This returns the median of the prediction interval.

Example: Box-Cox transformation

- The back-tranformed mean is given by:

\[ \widehat{y}_{T+h|T} = \left\{\begin{array}{lr} exp(\widehat{w}_{T+h|T})[1 + \frac{\sigma_{h}^{2}}{2}] & \textrm{if} \lambda=0; \\ (\lambda \widehat{w}_{T+h|T} + 1)^{1/\lambda}[1 + \frac{\sigma_{h}^{2}(1-\lambda)}{2(\lambda \widehat{w}_{T+h|T} + 1)^{2}}] & \textrm{otherwise} \end{array}\right\} \] where \(\widehat{w}_{T+h|T}\) is the \(h\)-step forecast mean and \(\sigma_{h}^{2}\) is the \(h\)-step forecast variance on the transformed scale.

Bias adjustments

- bias: The difference between the back-transformed forecast and the mean forecast

- bias-adjusted: uses the mean forecast rather than the back-transformed forecast

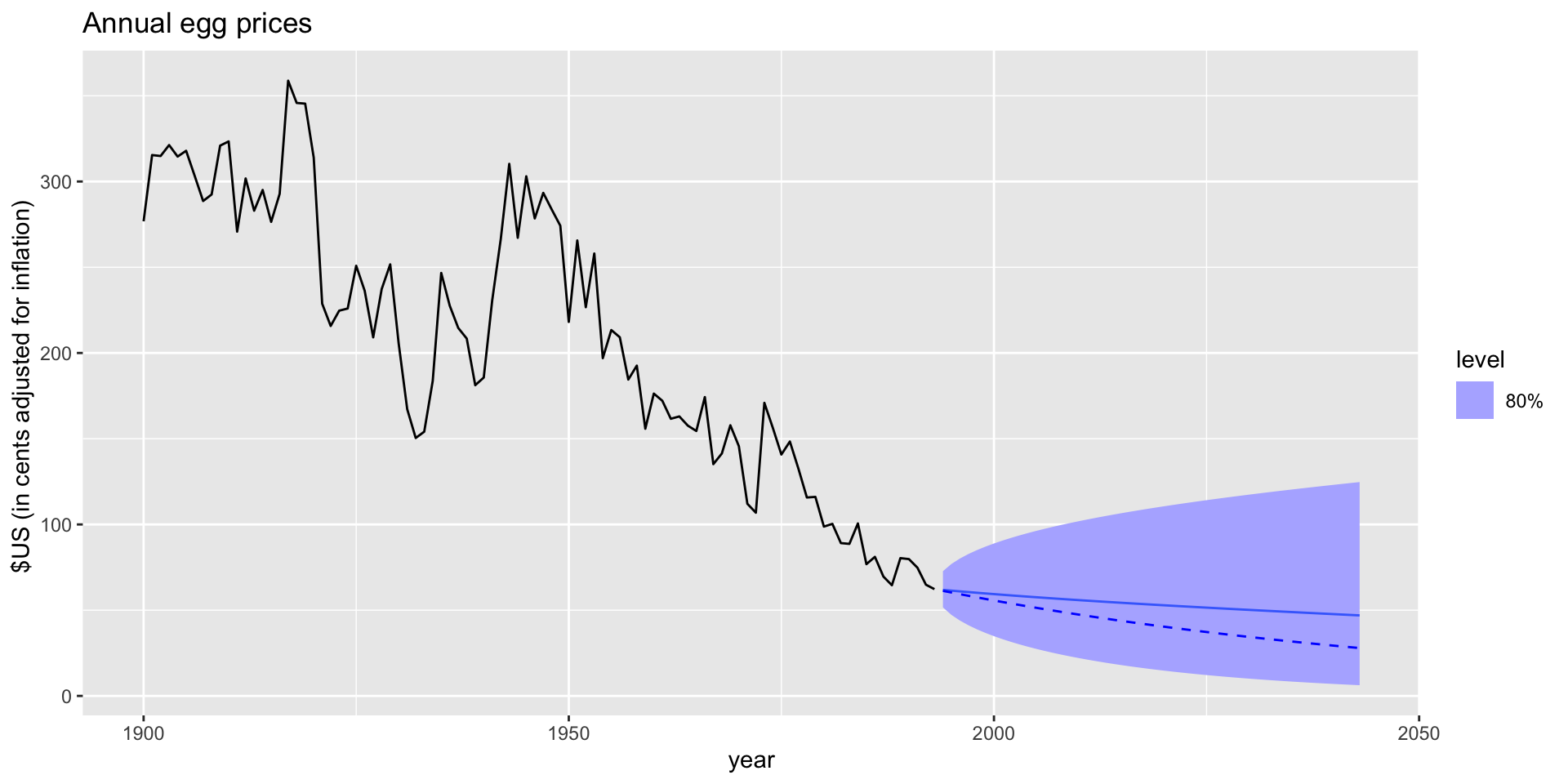

Bias adjustments: example

- Drift forecast of egg prices using a log transformation.

- Solid line: mean; dashed line: median

Bias adjustments: example

- Back-transformed means automatically calculated with

fable.- Median accessible using

median()on the distribution variable.

- Median accessible using

# A tsibble: 94 x 7 [1Y]

year eggs chicken copper nails oil wheat

<dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 1900 277. NA 6.81 54.1 23.1 399.

2 1901 315. NA 6.94 48.6 18.6 404.

3 1902 315. NA 4.74 41.6 14.9 425.

4 1903 321. NA 5.21 39.5 16.9 399.

5 1904 315. NA 4.98 36.3 15.5 416.

6 1905 318. NA 6.01 36.1 11.2 437.

7 1906 303. NA 7.45 37.3 13.1 410.

8 1907 289. NA 7.81 38.9 12.5 439.

9 1908 292. NA 5.18 40.0 13.0 469.

10 1909 321. NA 5.10 36.5 12.6 531.

# ℹ 84 more rowsBias adjustments: example

Bias adjustments: example

# A fable: 50 x 4 [1Y]

# Key: .model [1]

.model year eggs .mean

<chr> <dbl> <dist> <dbl>

1 RW(log(eggs) ~ drift()) 1994 t(N(4.1, 0.018)) 61.8

2 RW(log(eggs) ~ drift()) 1995 t(N(4.1, 0.036)) 61.4

3 RW(log(eggs) ~ drift()) 1996 t(N(4.1, 0.055)) 61.0

4 RW(log(eggs) ~ drift()) 1997 t(N(4.1, 0.074)) 60.6

5 RW(log(eggs) ~ drift()) 1998 t(N(4.1, 0.093)) 60.2

6 RW(log(eggs) ~ drift()) 1999 t(N(4, 0.11)) 59.8

7 RW(log(eggs) ~ drift()) 2000 t(N(4, 0.13)) 59.4

8 RW(log(eggs) ~ drift()) 2001 t(N(4, 0.15)) 59.0

9 RW(log(eggs) ~ drift()) 2002 t(N(4, 0.18)) 58.6

10 RW(log(eggs) ~ drift()) 2003 t(N(4, 0.2)) 58.3

# ℹ 40 more rowsBias adjustments: example

prices |>

filter(!is.na(eggs)) |>

model(RW(log(eggs) ~ drift())) |>

forecast(h = 50) |>

mutate(.median = median(eggs))# A fable: 50 x 5 [1Y]

# Key: .model [1]

.model year eggs .mean .median

<chr> <dbl> <dist> <dbl> <dbl>

1 RW(log(eggs) ~ drift()) 1994 t(N(4.1, 0.018)) 61.8 61.3

2 RW(log(eggs) ~ drift()) 1995 t(N(4.1, 0.036)) 61.4 60.3

3 RW(log(eggs) ~ drift()) 1996 t(N(4.1, 0.055)) 61.0 59.3

4 RW(log(eggs) ~ drift()) 1997 t(N(4.1, 0.074)) 60.6 58.4

5 RW(log(eggs) ~ drift()) 1998 t(N(4.1, 0.093)) 60.2 57.5

6 RW(log(eggs) ~ drift()) 1999 t(N(4, 0.11)) 59.8 56.6

7 RW(log(eggs) ~ drift()) 2000 t(N(4, 0.13)) 59.4 55.7

8 RW(log(eggs) ~ drift()) 2001 t(N(4, 0.15)) 59.0 54.8

9 RW(log(eggs) ~ drift()) 2002 t(N(4, 0.18)) 58.6 53.9

10 RW(log(eggs) ~ drift()) 2003 t(N(4, 0.2)) 58.3 53.0

# ℹ 40 more rowsRecall: decomposed vaiables

- Additive: \(y_{t} = \widehat{S}_{t} + \widehat{A}_{t}\)

- where \(\widehat{A}_{t} = \widehat{T}_{t} + \widehat{R}_{t}\) is the seasonally adjusted component.

- Multiplicative: \(y_{t} = \widehat{S}_{t}\widehat{A}_{t}\)

Forecasting with decomposed variables

- To forecast, forecast \(\widehat{S}_{t}\) and \(\widehat{A}_{t}\) separately.

- \(\widehat{S}_{t}\) typically assumed unchanging

- Thus a seasonal naive method used for \(\widehat{S}_{t}\)

- \(\widehat{A}_{t}\) can be forecasted with any appropriate method.

- \(\widehat{S}_{t}\) typically assumed unchanging

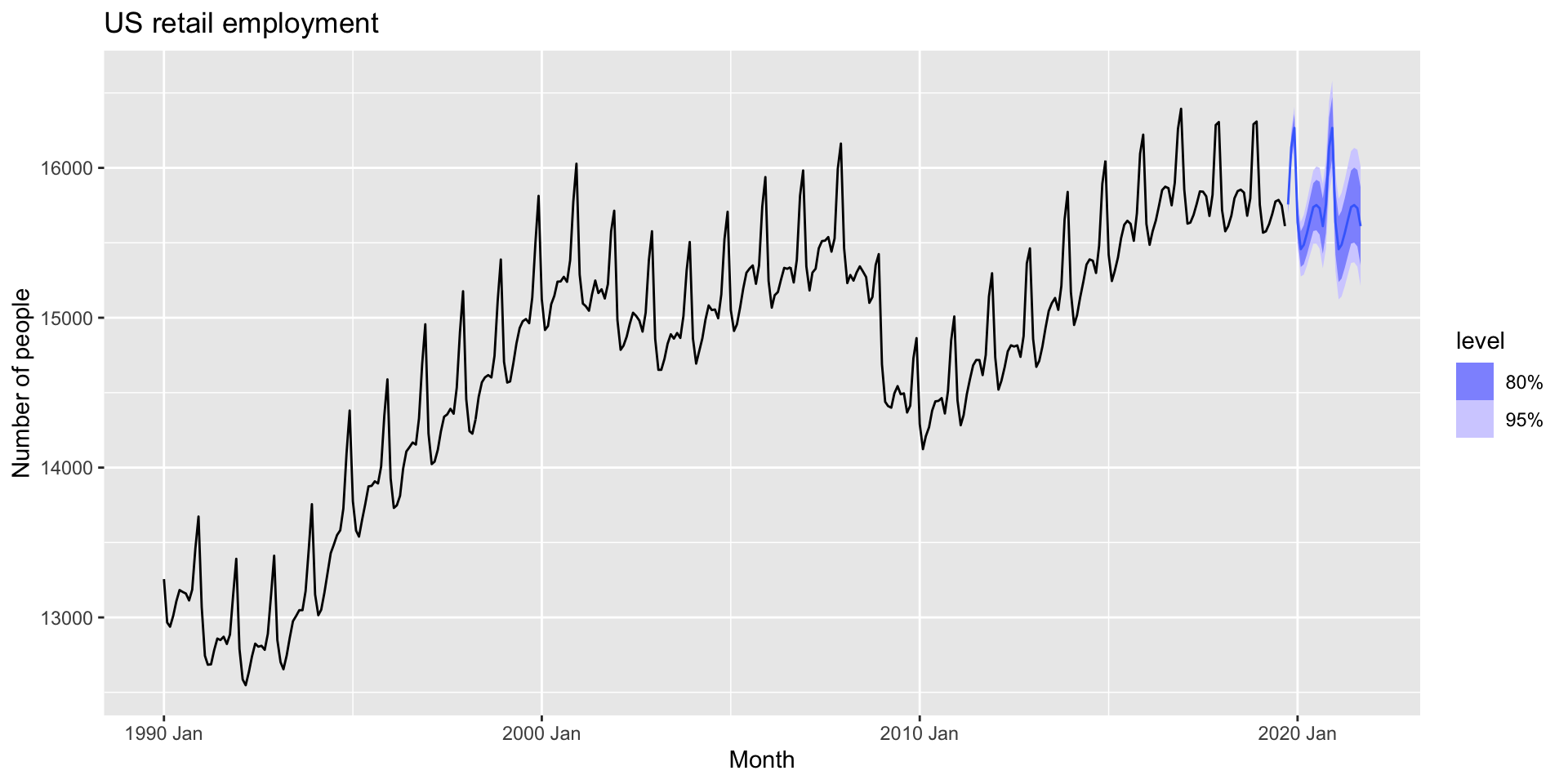

Example: US retail employment

- First, filter

us_retail_employmenttoyear>=1990andTitle=="Retail Trade"

Example: US retail employment

- Next, use an STL decompositionL

Example: US retail employment

- Let’s look at the components:

dcmp <- us_retail_employment |>

model(STL(Employed ~ trend(window = 7), robust = TRUE)) |>

components()

dcmp# A dable: 357 x 8 [1M]

# Key: Series_ID, .model [1]

# : Employed = trend + season_year + remainder

Series_ID .model Month Employed trend season_year remainder season_adjust

<chr> <chr> <mth> <dbl> <dbl> <dbl> <dbl> <dbl>

1 CEU42000… STL(E… 1990 Jan 13256. 13326. -72.6 2.85 13328.

2 CEU42000… STL(E… 1990 Feb 12966. 13297. -273. -58.1 13239.

3 CEU42000… STL(E… 1990 Mar 12938. 13270. -295. -36.3 13233.

4 CEU42000… STL(E… 1990 Apr 13012. 13230. -216. -1.59 13228.

5 CEU42000… STL(E… 1990 May 13108. 13223. -119. 4.72 13228.

6 CEU42000… STL(E… 1990 Jun 13183. 13212. -30.6 0.978 13213.

7 CEU42000… STL(E… 1990 Jul 13170. 13198. -32.8 5.23 13203.

8 CEU42000… STL(E… 1990 Aug 13160. 13178. -20.1 1.84 13180.

9 CEU42000… STL(E… 1990 Sep 13113. 13149. -45.5 9.76 13159.

10 CEU42000… STL(E… 1990 Oct 13185. 13113. 64.2 8.28 13121.

# ℹ 347 more rowsExample: US retail employment

- And remove the

.modelcolumn:

Example: US retail employment

- Next, make a naive forecast the seasonally adjusted component:

# A fable: 24 x 5 [1M]

# Key: Series_ID, .model [1]

Series_ID .model Month

<chr> <chr> <mth>

1 CEU4200000001 NAIVE(season_adjust) 2019 Oct

2 CEU4200000001 NAIVE(season_adjust) 2019 Nov

3 CEU4200000001 NAIVE(season_adjust) 2019 Dec

4 CEU4200000001 NAIVE(season_adjust) 2020 Jan

5 CEU4200000001 NAIVE(season_adjust) 2020 Feb

6 CEU4200000001 NAIVE(season_adjust) 2020 Mar

7 CEU4200000001 NAIVE(season_adjust) 2020 Apr

8 CEU4200000001 NAIVE(season_adjust) 2020 May

9 CEU4200000001 NAIVE(season_adjust) 2020 Jun

10 CEU4200000001 NAIVE(season_adjust) 2020 Jul

# ℹ 14 more rows

# ℹ 2 more variables: season_adjust <dist>, .mean <dbl>Example: US retail employment

- Finally, use

autoplot()to plot the forecast with the seasonal component added back in:

Example: US retail employment

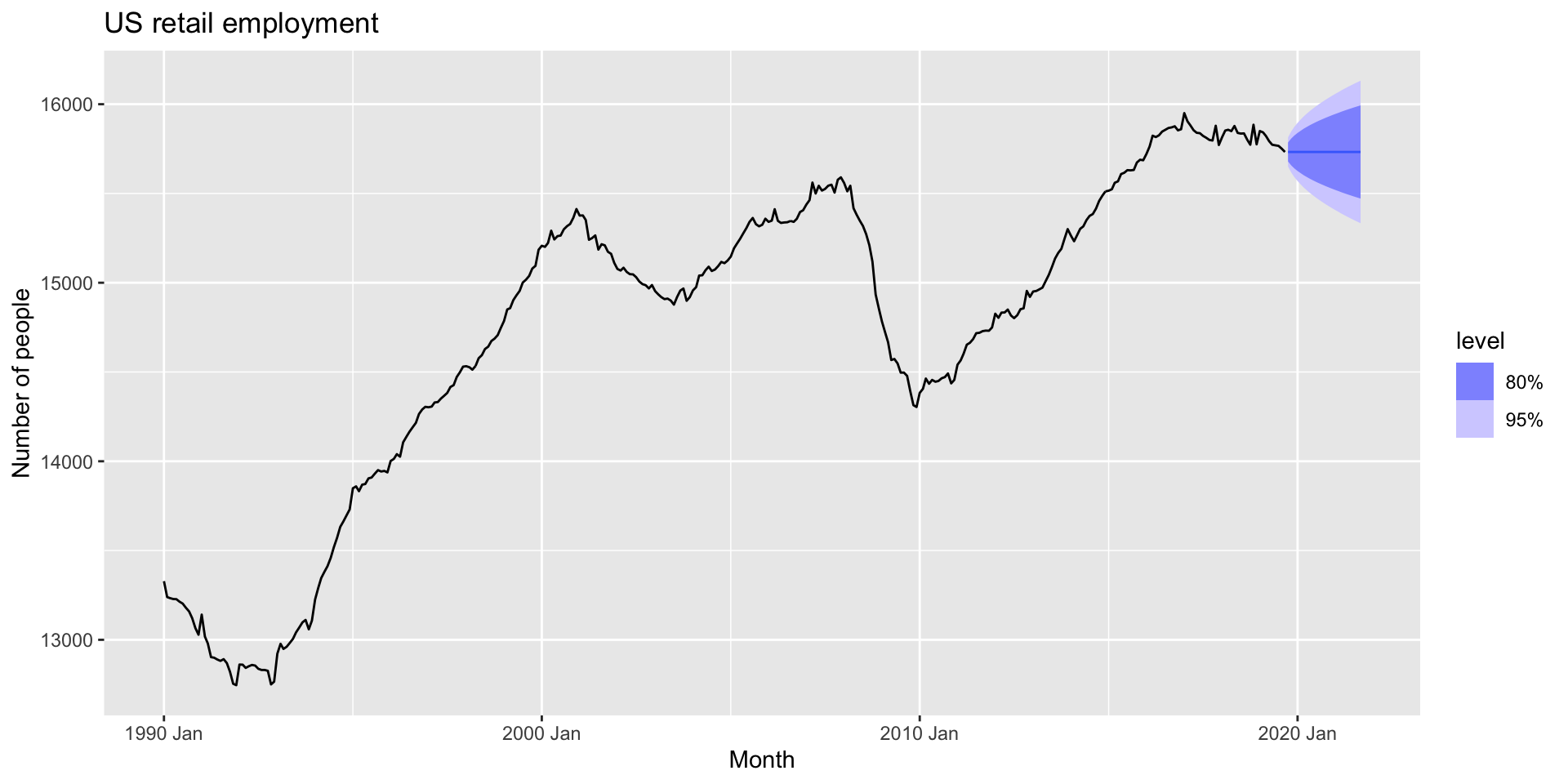

decomposition_model()

- The

decomposition_model()function makes this a bit simpler.- Seasonal naive forecasts are used for the seasonal component automatically.

- Also reseasonalizes the forecasts for you for observed data:

decomposition_model() forecasts

autoplot()will plot the forecasts for the original data as well as future forecasts:

decomposition_model() plot